TL;DR:

- B2B fintech provides automation, real-time visibility, and compliance improvements tailored for organizational financial operations.

- Its effective implementation depends on understanding cross-border challenges, integration complexities, and the importance of automation maturity.

Business payments should be straightforward. In practice, many finance teams at SMEs and digital-first companies deal with unpredictable costs, unclear routing paths, and reconciliation headaches that eat hours each week. The promise of B2B fintech (financial technology built specifically for business-to-business operations) is to replace that chaos with automation, real-time visibility, and compliance frameworks that actually work at scale. This article breaks down exactly what B2B fintech is, where it delivers measurable value, and what the typical implementation guides fail to mention.

Table of Contents

- Understanding B2B fintech: Core concepts and why it matters

- Cross-border payments: Challenges and fintech solutions

- Automation and operational efficiency: AP and payment benchmarks

- Hidden challenges and edge cases in B2B fintech

- What most guides miss about B2B fintech adoption

- Explore B2B fintech solutions with Demivolt

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| B2B fintech definition | B2B fintech delivers automated, integrated financial tools for businesses instead of individual consumers. |

| Cross-border payment challenges | Traditional business payments suffer from unpredictable fees and delays that fintech solutions can address. |

| Operational efficiency benefits | Fintech automation reduces invoice processing time by up to 90% compared to manual workflows. |

| Beware hidden pitfalls | Edge cases like routing and compliance mismatches can still disrupt fintech-powered operations. |

| Fit matters most | Workflow alignment and transparency drive more ROI than feature lists when choosing a B2B fintech platform. |

Understanding B2B fintech: Core concepts and why it matters

Most finance leaders have heard the term “fintech” used loosely to describe everything from mobile wallets to blockchain experiments. B2B fintech is a much more specific category. As defined by industry analysts, B2B fintech describes financial technology products and services built for organizations rather than individual consumers, typically delivered through workflows, platforms, and integrations (often via APIs) that automate and standardize financial operations.

That distinction matters. Consumer fintech is optimized for simplicity and user experience at the individual level. B2B fintech is optimized for accuracy, auditability, compliance, and throughput at the organizational level. The requirements are fundamentally different. A mobile payment app needs to be intuitive for a single person. A B2B payment platform needs to handle multi-entity structures, approval chains, regulatory reporting, and reconciliation across dozens or hundreds of transactions simultaneously.

“B2B payments are generally transactions made between businesses for goods and services, and they can be recurring or one-off depending on contract terms. This B2B context increases operational sensitivity around exact received amounts and reconciliation.” Tipalti B2B Payment Solutions Guide

The core capabilities most B2B fintech platforms share include:

- Payment tooling: SEPA, SWIFT, ACH, and local payment rails for domestic and international transfers

- Invoicing and accounts payable (AP) automation: Digital invoice capture, matching, and approval workflows

- Cash flow analytics: Real-time dashboards showing inflows, outflows, and projected balances

- Compliance automation: KYC (Know Your Customer), AML (Anti-Money Laundering), and sanctions screening built into payment flows

- API connectivity: Integrations with ERP systems, accounting tools, and banking partners

Understanding how fintech platforms and payment infrastructure interact is essential before selecting any solution. The role of APIs in fintech is especially critical here: APIs allow B2B platforms to connect directly to banking networks, enabling business payment automation that eliminates manual data entry and reduces the risk of human error at every touchpoint.

Why does this matter specifically for SMEs and digital-first companies? Large enterprises often have in-house treasury teams and relationships with major banks that absorb the friction. Smaller, faster-growing companies typically lack both. B2B fintech levels that playing field by delivering enterprise-grade financial infrastructure through accessible, scalable platforms.

Cross-border payments: Challenges and fintech solutions

Cross-border B2B payments are where operational risk concentrates most visibly. When your company pays a supplier in Singapore, collects revenue from a client in Germany, or moves working capital between subsidiaries in two different countries, the complexity multiplies fast.

The core mechanics of cross-border payments involve routing through payment networks and intermediaries (correspondent banks) when direct connections aren’t available. Each intermediary adds potential for fees, delays, and reduced visibility into total cost and timing. A payment that looks simple on the surface, say, a wire transfer from the US to Poland, might pass through three or four correspondent banks before landing in the recipient’s account. Each hop represents a point where the transaction can be delayed, inspected, or charged an additional fee.

Here’s how traditional bank processes compare to fintech-enabled approaches:

| Factor | Traditional banking | B2B fintech platform |

|---|---|---|

| Settlement time | 2 to 5 business days | Often same-day or next-day |

| Fee transparency | Fees revealed after transaction | Fees disclosed upfront |

| FX rate visibility | Rate applied at execution | Real-time rate preview |

| Reconciliation | Manual, spreadsheet-based | Automated, reference-matched |

| Compliance checks | Manual review, variable timing | Automated, built into workflow |

| Payment tracking | Limited or no tracking | End-to-end status visibility |

The contrast is significant. For a company processing dozens of international invoices monthly, the cumulative time and cost savings from switching to a fintech-enabled approach can be substantial.

Here’s a practical framework for reducing friction in cross-border B2B payments:

- Standardize payment data fields: Ensure every outgoing payment includes complete beneficiary name, IBAN or account number, bank SWIFT/BIC code, and reference details. Incomplete data is the single most common cause of payment delays.

- Consolidate currency exposure: Rather than converting currency reactively on each transaction, use a platform that lets you hold balances in multiple currencies and convert when rates are favorable.

- Automate recurring payments: Supplier payments that happen on a fixed schedule should be automated entirely, removing manual initiation and reducing the risk of missed payment terms.

- Map your correspondent bank paths: Know in advance which corridors your platform uses for specific country pairs. Some corridors are faster and cheaper than others.

- Implement payment pre-validation: Many modern platforms will validate IBAN and BIC details before a payment is submitted, catching errors before they cause delays.

Pro Tip: Before onboarding a new cross-border supplier or client, run a small test transaction to verify that the full payment path works as expected. This exposes routing or compliance issues before they affect time-sensitive payments.

The resources on cross-border payment facilitation and SME international payments go deeper into specific corridor strategies and compliance considerations that affect fast-growing businesses.

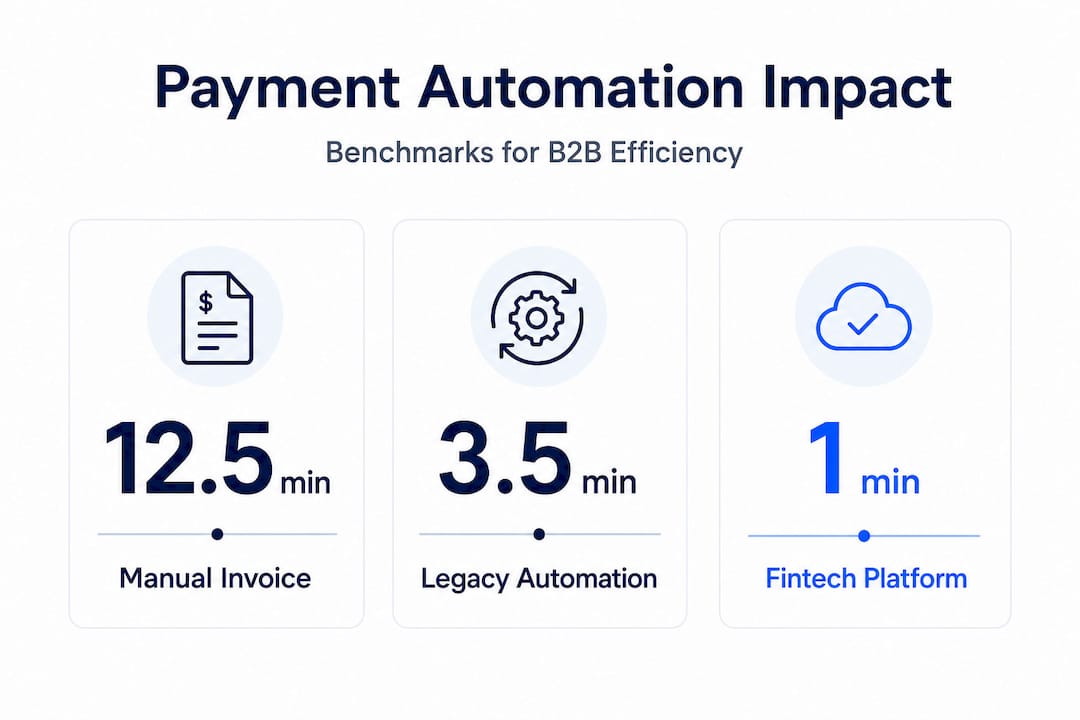

Automation and operational efficiency: AP and payment benchmarks

Once a B2B fintech platform is in place, the next question is how much operational value it actually delivers. The answer depends heavily on where your organization sits on the automation maturity curve.

Published benchmarks from AP automation research illustrate the gap clearly. Manual invoice processing averages 12.5 minutes per invoice. Legacy automation, which typically means OCR (optical character recognition) plus basic rules-based matching, reduces that to 4.8 minutes. AI-native automation, which handles exception resolution and learns from historical data, drops it to 1.2 minutes. That is roughly a 90% reduction in processing time per invoice compared to manual handling.

Run those numbers against your actual invoice volume. If your team processes 500 invoices per month manually, that is approximately 104 hours per month spent on invoice handling alone. Legacy automation gets you to about 40 hours. AI-native automation gets you to under 10 hours. The freed-up capacity can be redirected to exception handling, vendor relationship management, or financial planning tasks that actually require human judgment.

Here is a useful benchmark table to contextualize your current position:

| Automation level | Processing time per invoice | Monthly cost (500 invoices) | Error rate |

|---|---|---|---|

| Manual | 12.5 minutes | High (labor-intensive) | 3 to 5% |

| Legacy (OCR + rules) | 4.8 minutes | Moderate | 1 to 2% |

| AI-native | 1.2 minutes | Low (scalable) | Below 0.5% |

Beyond speed, automation delivers benefits that are harder to quantify but equally important:

- Reduced duplicate payment risk: Automated matching flags duplicate invoices before they are paid

- Consistent compliance documentation: Every transaction generates an audit trail without manual effort

- Real-time cash visibility: Finance leaders can see actual cash position rather than relying on end-of-day reconciliation

- Approval workflow enforcement: Payment limits, dual authorization, and role-based controls become automatic, not dependent on individual discipline

Learning how to automate business payments and stay compliant is not just about efficiency. It is about building a financial infrastructure that scales without adding proportional headcount. Companies that have pursued fintech partnership examples in their payment stack consistently report that compliance confidence is one of the top operational gains alongside cost reduction.

Hidden challenges and edge cases in B2B fintech

Most articles on B2B fintech focus on the upside. The adoption reality is messier. There are well-documented edge cases and implementation hurdles that can significantly affect whether your fintech investment delivers its expected value.

Cross-border payment edge cases that meaningfully affect operational outcomes include: correspondent-bank routing when direct links don’t exist, redundant or conflicting compliance checks across jurisdictions, and payer/payee data quality problems that cause blockages or exception handling. These are not rare events. They affect a predictable percentage of cross-border transactions, and the way your platform handles them determines whether your operations stay smooth or grind into manual escalation.

Common hidden challenges B2B fintech adopters encounter include:

- Jurisdiction-specific compliance gaps: A platform that is fully compliant in the EU may not handle regulatory requirements for payments into certain Asian or African markets without additional configuration or local banking partners

- Data format mismatches: ERP systems and banking platforms often use different reference formats for invoices and payments, causing reconciliation failures even when the payment itself succeeds

- Approval chain rigidity: Some platforms have limited flexibility in approval routing, which creates bottlenecks when team structures are matrix-based or change frequently

- FX spread opacity: Even platforms that advertise transparent pricing may embed margins in FX spreads that are not clearly surfaced in the transaction view

- Integration testing gaps: A clean API integration in a test environment sometimes behaves differently under real production loads, especially with high-volume payment batches

Automation maturity level is also a key factor that most benchmark comparisons underweight. Reported efficiency gains are highly dependent on whether a platform is doing basic digitization (OCR plus rules) versus genuine AI-native exception resolution. Vendors often market the AI-native numbers while delivering legacy-level automation in practice. Ask for specific details about how exception cases are handled before signing a contract.

Pro Tip: Request a live walkthrough of how the platform handles a payment that fails compliance screening on the first attempt. The way a platform manages exceptions reveals far more about its operational quality than its standard transaction flow.

Issues like these can be anticipated and mitigated. Understanding cross-border payment bottlenecks specifically helps finance teams identify where failure points are most likely to emerge and how to structure their workflows to reduce exposure.

What most guides miss about B2B fintech adoption

The standard narrative around B2B fintech adoption goes like this: choose a modern platform, connect your APIs, automate your payments, and watch the operational savings roll in. That narrative is not wrong. It is just incomplete in ways that cost finance leaders time and money when they discover the gaps after go-live.

The reality is that the operational value of B2B fintech scales with automation maturity, not just adoption. A company that moves from manual payments to a basic digital platform will see real improvements. A company that builds toward AI-native automation with clean data, tight integrations, and exception-resolved workflows will see transformational improvements. The difference between those two outcomes is not the platform feature list. It is the quality of implementation, the discipline around data standards, and the willingness to redesign workflows rather than just digitize the existing ones.

The edge cases covered in the previous section are not footnotes. They are the operational reality for any company processing significant cross-border volume. The businesses that get the most from B2B fintech are the ones that go into implementation knowing where the hard parts are, rather than discovering them under pressure.

We have seen B2B fintech transform payments for SMEs precisely because those organizations approached the implementation with realistic expectations about what needed to change internally, not just what the platform would deliver automatically.

Our perspective: don’t evaluate B2B fintech platforms based on features alone. Evaluate them based on how they handle your specific payment corridors, how they manage exceptions, how transparent they are about FX costs, and how their compliance framework aligns with your actual operating jurisdictions. The platform that fits your workflows beats the platform with the longest feature list every time.

Explore B2B fintech solutions with Demivolt

If this article has clarified what B2B fintech can and should deliver for your business, the next step is finding a platform that matches your operational reality, not just your aspirations.

Demivolt is a regulated European fintech platform built specifically for SMEs and digital-first companies that need compliant, efficient payment infrastructure. From dedicated IBAN accounts and SEPA/SWIFT payment management to virtual and physical business cards, multi-account structures, and role-based access controls, Demivolt is designed to eliminate the friction that slows finance teams down. If you are ready to move past unpredictable costs and manual workflows, explore how the automation advantages built into Demivolt’s platform can bring measurable efficiency to your payment operations from day one.

Frequently asked questions

What distinguishes B2B fintech from consumer fintech?

B2B fintech is built for organizational financial operations rather than personal finance, focusing on workflows, API integrations, compliance automation, and multi-user business structures that consumer apps simply are not designed to handle.

How do B2B fintech platforms handle currency conversion in cross-border payments?

Currency conversion happens at some point along the payment chain, and without a transparent platform, fees and rates are often hidden. Modern B2B fintech solutions surface FX rates upfront and reduce the number of correspondent bank intermediaries involved, improving both cost visibility and settlement speed.

What operational benchmarks demonstrate the value of B2B fintech automation?

According to published AP automation research, manual invoice processing averages 12.5 minutes per invoice, legacy automation cuts that to 4.8 minutes, and AI-native automation reduces it to just 1.2 minutes, representing roughly a 90% time savings at full maturity.

What are common edge cases that disrupt B2B fintech payment flows?

Routing through correspondent banks when direct connections are unavailable, conflicting compliance checks across jurisdictions, and payer/payee data quality problems are the most frequent causes of payment blockages and exception escalations in cross-border B2B flows.

How do SMEs maximize value from B2B fintech platforms?

SMEs get the most value by prioritizing workflow fit, maintaining clean and complete payment data, and advancing their automation maturity level rather than simply adopting new tools without redesigning the underlying processes.

Recommended

- Demivolt | Blog – Why automate business payments? Reduce costs, risks and delays

- Demivolt | Blog – How Fintech Transforms Cross-Border Payments for SMEs

- Demivolt | Blog – Business Payment Solutions Explained for European SMEs

- Demivolt | Blog – Fintech partnerships: Real-world examples for better cross-border payments