TL;DR:

- Business account verification confirms a company’s legitimacy and control for compliance purposes.

- Proper, ongoing verification prevents payment delays, account blocks, and regulatory fines for SMEs.

- Automated verification processes significantly reduce onboarding time and improve compliance accuracy.

Even well-established SMEs discover too late that a single gap in their verification records can freeze payments, block payroll, or delay a critical supplier transaction. Business account verification is one of those processes that feels invisible when it works and catastrophic when it doesn’t. Yet most SME owners treat it as a one-time paperwork task rather than the ongoing compliance foundation it actually is. This guide breaks down exactly what verification involves, why European regulators take it seriously, and how your finance team can master it without drowning in manual processes.

Table of Contents

- What is business account verification?

- Why business account verification matters for SMEs

- How business account verification works: steps and frameworks

- Navigating edge cases: Complex accounts and risk scenarios

- Best practices for SMEs: Making account verification seamless

- What most SMEs get wrong about verification—and how to fix it

- Streamline your business account verification with Demivolt

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Verification is essential | Business account verification protects SMEs from regulatory and operational risks. |

| Automation speeds onboarding | New digital tools reduce verification from days to minutes for most SMEs. |

| Complex cases need care | Multi-jurisdictional or complex ownership requires advanced review and ongoing monitoring. |

| Proactive practices win | Maintaining updated records and using modern banking partners ensures smoother verification. |

What is business account verification?

Business account verification is the process by which financial institutions confirm that a business is legitimate, properly registered, and controlled by the people who claim to own it. Before any account is opened or significant transaction is approved, the bank or fintech provider needs to understand who is behind the business and whether that entity poses any financial or legal risk.

Two core frameworks drive this process:

- Know Your Business (KYB): Confirms the legal existence, registration, ownership structure, and ultimate beneficial owners (UBOs) of a company.

- Know Your Customer (KYC): Verifies the identity of individual directors, shareholders, and authorized users connected to the business.

- Anti-Money Laundering (AML) screening: Cross-references entities and individuals against global sanctions lists and watchlists.

- Ongoing monitoring: Ensures that changes in ownership, jurisdiction, or risk profile are caught and reviewed after the account is live.

Regulators across the EU require these checks to protect market integrity, prevent fraud, and stop illicit funds from moving through the financial system. For SMEs, incomplete or inaccurate verification leads to real consequences: rejected onboarding, payment delays, or compliance fines that can be disproportionately damaging for smaller businesses.

Multi-jurisdictional entities and incomplete registry data are addressed using techniques such as enhanced due diligence (EDD) and tiered risk assessment, which means the complexity of your business structure directly affects how thorough the verification process will be.

Getting setting up business finances right from the start makes verification smoother, because clean financial records and accurate registration documents reduce the back-and-forth that delays account approval. Choosing providers with efficient onboarding solutions also makes a measurable difference in how quickly your business gets operational.

Why business account verification matters for SMEs

With the basics clear, it’s crucial to explore why verification matters so deeply for SMEs seeking efficiency and security.

European AML regulations, the EU’s Anti-Money Laundering Directives, and cross-border payment rules all place legal obligations on financial institutions to verify the businesses they serve. Banks and fintechs that fail to comply face heavy regulatory penalties, so they pass the verification burden directly onto their business clients. That means your SME needs to meet their standards, not just once, but continuously.

“Manual KYB onboarding can require 3-5 full-time employees for a mid-sized firm and lead to rejection rates of 15-25%.”

That statistic is striking, and it reveals why SMEs are disproportionately affected. A large corporation has a dedicated compliance department to manage these requirements. A 10-person SME does not. When verification stalls, the consequences hit fast:

- Blocked payments: A supplier waiting on funds doesn’t care about your compliance backlog.

- Delayed payroll: Employees expect to be paid on time, regardless of what’s happening with your bank’s verification queue.

- Suspended accounts: If a bank flags your account mid-operation, you may lose access to funds during a critical business period.

- Supplier friction: New vendors often require verified account details before engaging, slowing down procurement.

- Reputational risk: Repeated payment failures signal instability to partners and clients.

Understanding the importance of dedicated business accounts is part of the picture here. A dedicated business account keeps your finances clean and verifiable, which makes the entire KYB process faster and less prone to errors. Beyond compliance, the 2026 business account benefits for SMEs include better cash flow visibility and stronger credibility with financial partners.

Automation changes the equation significantly. Modern fintech platforms have replaced multi-day manual reviews with digital workflows that complete verification in minutes. For a lean finance team, that shift from days to minutes is not a minor convenience. It’s the difference between launching a new supplier relationship this week or next month. Consistently improving compliance accuracy through better processes also reduces the risk of errors that trigger re-verification.

How business account verification works: steps and frameworks

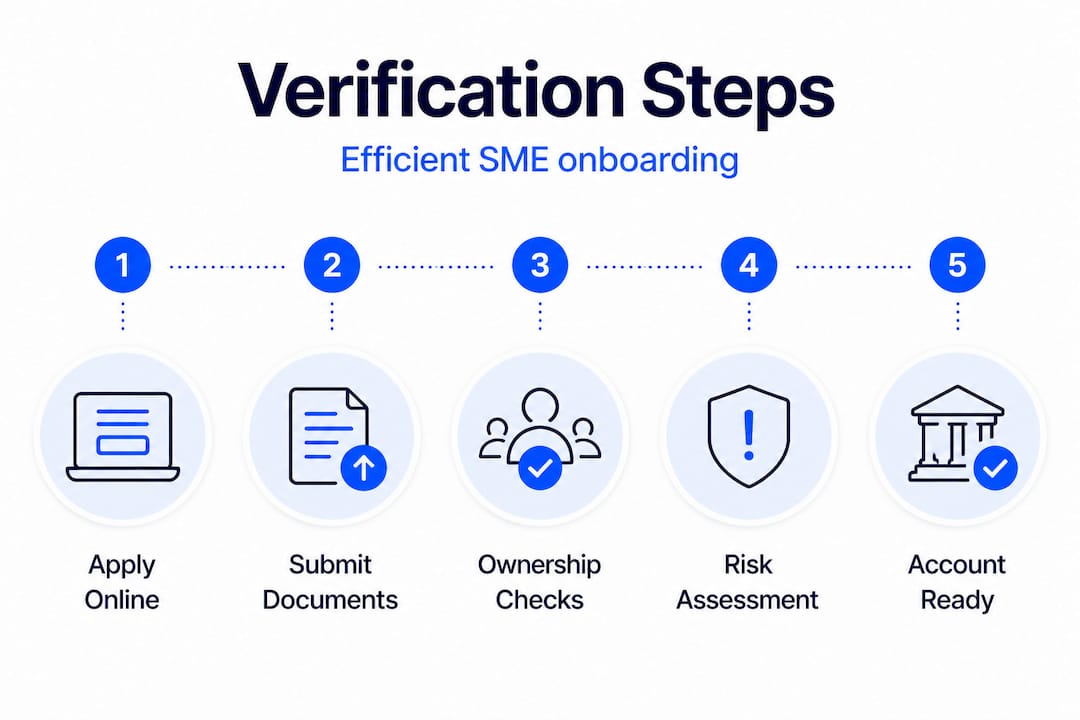

Understanding its importance, let’s break down the nuts and bolts of how business account verification actually happens.

The process follows a logical sequence, though the depth of each step varies based on your business’s risk profile:

- Document collection: Gather official registration certificates, articles of incorporation, proof of address, and identification for all directors and UBOs.

- Ownership and control structure review: The provider maps who owns what percentage of the business and identifies any individuals with significant control.

- Risk screening: The business and its key individuals are screened against politically exposed persons (PEP) lists and adverse media databases.

- Sanctions checks: Real-time checks against global sanctions lists, including EU, UN, and OFAC databases.

- Ongoing monitoring: Automated alerts flag changes in ownership, new sanctions hits, or shifts in the business’s risk profile after the account goes live.

One of the most important decisions your SME can make is choosing between a manual and an automated verification approach. The difference is significant:

| Factor | Manual verification | Automated verification |

|---|---|---|

| Onboarding time | 3-10 business days | Minutes to hours |

| Staff required | 3-5 FTEs for mid-sized firms | Minimal human review |

| False positive rate | Often above 40% | Typically below 20% |

| Scalability | Limited by team size | Scales with volume |

| Error risk | Higher due to manual data entry | Lower with structured data inputs |

Automation cuts onboarding from days to minutes, while benchmarked manual alert-to-customer ratios run at 0.1-0.3 per month and false positive rates are kept below 20-40% with well-designed automated systems. That means fewer unnecessary account holds and faster resolution when issues do arise.

Common blockers in the process include complex ownership chains, missing registry data in certain jurisdictions, and cross-border entities where documents exist in multiple languages or formats. Understanding the full step-by-step account opening process before you begin saves time and avoids surprises.

Pro Tip: Choose banking partners that use tiered risk approaches. Low-risk businesses get fast-tracked through streamlined checks, while higher-risk profiles receive proportionate scrutiny. This prevents your straightforward SME from being held up by processes designed for complex financial entities. You can also use streamlining your workflow strategies to keep documentation organized and ready for rapid submission.

A well-structured SME bank reconciliation guide also helps you maintain the clean financial records that make ongoing verification checks far less disruptive.

Navigating edge cases: Complex accounts and risk scenarios

While most SMEs follow a standard path, it’s important to be prepared for exceptions that often cause the most confusion and delays.

Not every business fits neatly into a single-owner, single-jurisdiction structure. Many SMEs have grown organically, added investors, restructured across borders, or operate through holding companies. These structures create verification edge cases that standard processes aren’t always equipped to handle quickly.

Edge cases like nested ownership, circular ownership, and changing high-risk jurisdictions are addressed with recursive UBO resolution, enhanced due diligence, and risk tiering. Here’s how those scenarios typically break down:

| Edge case | Risk level | Verification approach |

|---|---|---|

| Nested ownership (company owns company) | Medium to high | Recursive UBO mapping |

| Circular ownership structures | High | Manual review plus EDD |

| Cross-country entities | Medium | Multi-jurisdiction document checks |

| Incomplete registry data | Medium | Alternative documentation requests |

| Recent ownership changes | Variable | Re-verification trigger |

| Operations in high-risk jurisdictions | High | Enhanced due diligence |

Enhanced due diligence (EDD) goes beyond standard checks. It involves deeper investigation into the source of funds, the nature of business relationships, and the history of key individuals. For SMEs operating in sectors like crypto, international trade, or financial services, EDD is often triggered automatically.

Risk tiering is how modern platforms manage this efficiently. Rather than applying maximum scrutiny to every account, they assign a risk score and calibrate the depth of review accordingly. A domestic retail business with two local directors gets a different treatment than a holding company with subsidiaries in three jurisdictions.

Pro Tip: Flag ownership changes to your banking provider as soon as they happen, not after the fact. A new investor, a restructured shareholding, or even a change in director can trigger a re-verification requirement. Catching it early prevents your account from being placed on hold during the review period. This is especially relevant if you’re managing multiple SME accounts across different entities or subsidiaries.

Ongoing monitoring is not optional. Financial institutions are required to periodically review account holders and update their risk assessments. SMEs that maintain accurate, up-to-date records experience far fewer disruptions during these reviews. Keeping clarity on account reconciliation ensures your financial records stay consistent with what your provider has on file.

Best practices for SMEs: Making account verification seamless

No SME leader wants to deal with blocked accounts or compliance headaches. Here’s how you can make the process painless and futureproof.

Automation significantly reduces onboarding workload and false positives, which directly improves SME operational efficiency. But technology alone isn’t enough. The businesses that sail through verification are the ones that have built good habits around documentation and process.

Here’s what actually works in practice:

- Keep your corporate documents current. Expired certificates, outdated addresses, or old articles of incorporation are among the most common causes of verification delays. Set a calendar reminder to review these at least annually.

- Maintain a clean UBO register. Know exactly who owns what percentage of your business at all times. If that changes, update your records immediately and notify your banking provider.

- Choose digital-first banking partners. Providers with robust digital onboarding infrastructure process verifications faster, with fewer errors, and with clearer communication when issues arise.

- Train your finance team on what triggers re-verification. New directors, significant ownership changes, and expansions into new jurisdictions all require updated checks.

- Use automation for recurring verification needs. Many platforms now offer perpetual KYB, meaning your business is monitored continuously rather than reviewed only at onboarding.

- Monitor your account status proactively. Don’t wait for a payment to fail before checking whether your verification is current. Build a quarterly review into your compliance calendar.

Staying current with modern business banking trends helps you identify when new tools or platforms could reduce your compliance burden. The fintech landscape moves quickly, and solutions that were unavailable two years ago are now standard features on leading platforms.

For newer businesses, building a solid startup bookkeeping process from day one creates the financial paper trail that makes verification straightforward from the very first account opening.

What most SMEs get wrong about verification—and how to fix it

Having seen the benefits of best practices, it’s worth reflecting on why so many SMEs still fall into the same traps, and what real-world experience reveals about getting verification right.

The most common mistake is treating account verification as a one-time event. Business owners submit their documents, get approved, and never think about it again. Then, two years later, a director leaves, a new investor comes in, or the company restructures, and suddenly the bank’s records no longer match reality. The account gets flagged, payments are delayed, and the finance team scrambles to gather documents they should have had ready all along.

The second mistake is underestimating automation. Many SME finance managers still rely on spreadsheets and email chains to manage compliance documentation. That approach works until it doesn’t. A missed renewal, a misfiled certificate, or an overlooked ownership change can cascade into a compliance incident that takes weeks to resolve.

There’s also a tendency to view verification as the bank’s problem rather than a shared responsibility. Regulators are clear: businesses have an obligation to provide accurate, current information. When something goes wrong, the institution bears the regulatory liability, but the SME bears the operational consequences.

The fix is straightforward but requires a mindset shift. Treat verification as an ongoing compliance framework, not a paperwork exercise. Build it into your business calendar. Assign clear ownership within your finance team. Use digital banking workflow tips to automate reminders and document management wherever possible.

The SMEs that handle this best are the ones that stop asking “what does the bank need from us?” and start asking “what does our compliance posture look like today?” That shift from reactive to proactive is what separates businesses that operate smoothly from those that get caught off guard.

Streamline your business account verification with Demivolt

If you want to avoid compliance bottlenecks and unlock smoother day-to-day finance, consider solutions built specifically for SME needs.

Demivolt is a regulated European fintech platform designed to make business banking fast, compliant, and transparent for modern SMEs. The platform’s digital onboarding process is built around current EU regulatory standards, meaning your verification experience is structured, clear, and significantly faster than traditional banking. Demivolt supports dedicated IBAN accounts, SEPA and SWIFT payments, multi-account structures, and role-based user management, all within a framework that keeps your compliance posture current. If you’re ready to move beyond manual processes, explore the fintech onboarding guide to see how a purpose-built platform handles verification without the friction.

Frequently asked questions

What documents are usually needed for business account verification?

Most banks require official business registration certificates, proof of ownership structure, and government-issued identification for all directors and beneficial owners. Additional documents may be requested depending on your business type or jurisdiction.

How long does business account verification take for SMEs?

Automated solutions can reduce onboarding from days to minutes, compared to manual checks that typically take 3-10 business days. The complexity of your ownership structure is the main variable that affects timing.

What happens if a business fails verification?

Accounts may be blocked or access denied until the missing or inaccurate information is corrected and resubmitted. In some cases, the bank may request additional documentation or escalate to enhanced due diligence before reinstating access.

Why are some SME accounts considered high risk during verification?

Incomplete registry data and high-risk jurisdictions increase a business’s risk score and typically trigger enhanced due diligence or longer review periods. Complex ownership structures, such as nested or circular shareholding arrangements, have the same effect.

Recommended

- Demivolt | Blog – Business account benefits for European SMEs in 2026

- Demivolt | Blog – Why Dedicated Business Accounts Matter for European SMEs

- Demivolt | Blog – Modern business banking trends: boost efficiency & compliance

- Demivolt | Blog – Business banking for SMEs: services, compliance & cross-border