TL;DR:

- Cross-border banking fees are often underestimated and can reach €150 to €250 per transaction outside SEPA.

- Digital banking offers SMEs up to 12 times savings on cross-border fees compared to traditional banks.

- Choosing the right banking model depends on transaction types, sector requirements, and technological readiness.

Most business owners assume their banking costs are roughly the same regardless of which provider they use. That assumption is expensive. Cross-border payments can cost SMEs up to 12x more outside SEPA than inside it, and digital solutions can deliver savings of at least 3x on fees compared to traditional banks. If your business sends invoices to clients in the UK, Switzerland, or beyond the eurozone, and you’re still relying on a legacy bank account, you’re leaving a significant portion of your revenue on the table. This guide breaks down the real numbers, compares your options, and helps you choose the right banking model for sustainable cross-border growth.

Table of Contents

- The true cost of cross-border business banking

- Digital, traditional, or hybrid? Choosing the right banking model

- How digital banking boosts European SME efficiency

- Limitations and edge cases: Where digital banking still falls short

- What most SMEs miss—and how to get digital banking right

- Upgrade your SME banking—next steps with Demivolt

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Cross-border cost gap | SMEs can save up to 12 times more on payments with digital solutions compared to traditional banks. |

| Model matters | Choose digital, traditional, or hybrid banking based on your business needs—not hype. |

| Efficiency boost | Digital banking streamlines operations, improves cash flow, and speeds up cross-border settlements. |

| Know the limits | Complex loans and high-risk sectors may still need traditional or hybrid bank partnerships. |

| Resilient approach | Blending digital and traditional banking offers the best balance of savings, speed, and flexibility for European SMEs. |

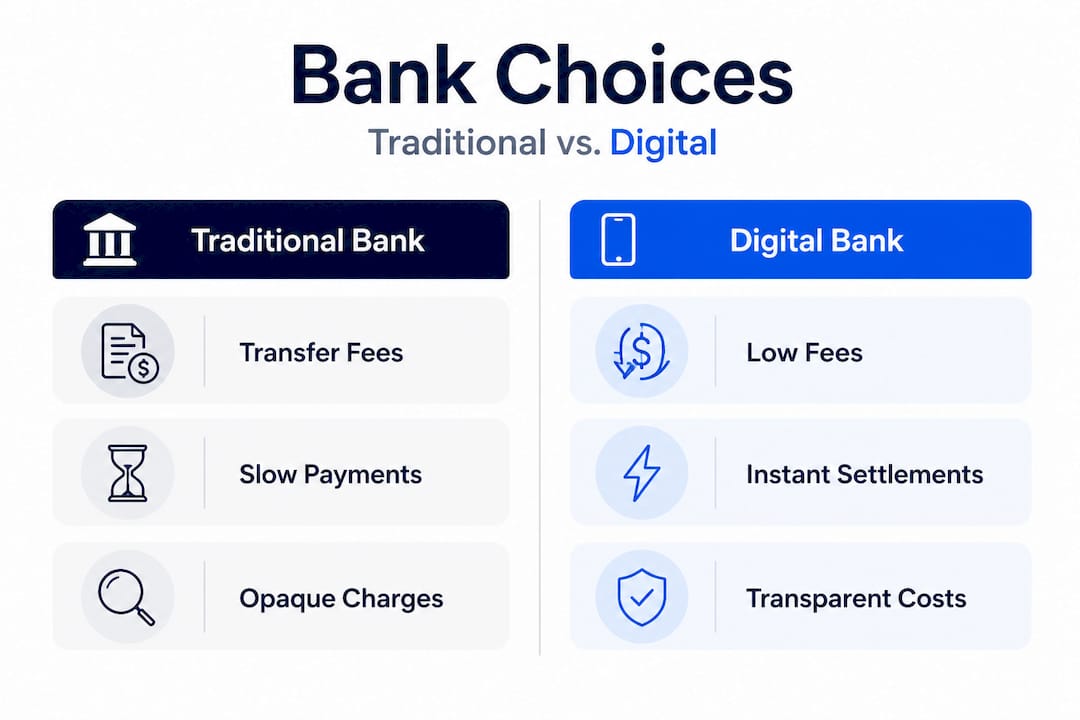

The true cost of cross-border business banking

Cross-border banking fees are one of the most consistently underestimated costs in small business finance. You see the wire transfer fee on your statement and think that’s the full picture. It rarely is.

Traditional banks layer in multiple charges for a single international transaction. There’s the outgoing transfer fee, the currency conversion spread, an intermediary bank fee (sometimes two), and a receiving fee on the other end. For a €5,000 invoice sent to a supplier in the US or UK, total friction costs can easily reach €150 to €250 per transaction before you even account for the 2 to 5 business days waiting for funds to clear.

Here’s how the numbers stack up across different banking models:

| Payment type | Traditional bank | SEPA digital | Hybrid model |

|---|---|---|---|

| Intra-SEPA transfer | €10 to €25 | €0 to €1 | €0 to €5 |

| Non-SEPA (USD/GBP) | €40 to €80 | €8 to €20 | €10 to €25 |

| FX conversion markup | 2% to 4% | 0.5% to 1.5% | 0.5% to 2% |

| Settlement time | 2 to 5 days | Instant to 1 day | 1 to 2 days |

The pattern is clear. Cross-border payments cost SMEs significantly more when routed through legacy infrastructure, but platforms that use how fintechs cut costs through modern payment rails change the equation fundamentally. Crucially, research confirms that interlinking instant payment systems reduces cross-border costs and meaningfully boosts trade volumes, especially for SMEs moving money across high-cost corridors.

Beyond fees, there are hidden costs that rarely appear on a transaction statement. Consider these:

- Staff time: Manually reconciling international payments can consume hours per week.

- FX exposure: Slow settlements mean more time spent exposed to currency fluctuations.

- Missed opportunities: Payment delays can strain supplier relationships and affect credit terms.

- Compliance friction: Legacy banks may freeze or delay non-standard payments without clear explanation, creating business disruption.

Understanding SEPA payments explained is a logical first step for any European SME, since operating within the SEPA framework dramatically reduces transaction friction for euro-denominated trade. But once your business extends beyond the eurozone, financial compliance for SMEs becomes more complex, and so does the cost structure. The smart move is to map exactly where your payments go, then match your banking infrastructure to that reality.

Digital, traditional, or hybrid? Choosing the right banking model

With costs and pitfalls in mind, SME owners must ask: which banking approach actually fits their situation?

The answer depends heavily on your transaction profile, your sector’s regulatory requirements, and how much your business relies on credit facilities. Let’s break each model down clearly.

Pure digital banking suits businesses with high-volume, standardized transactions that don’t require complex lending. If you run a SaaS company, an import/export operation with predictable flows, or a professional services firm billing across Europe, a digital-first platform gives you speed, transparency, and dramatically lower fees. The tradeoff is that hybrid models optimize for complex needs that pure digital solutions may not fully cover, particularly when it comes to property-backed loans, structured credit, or bespoke trade finance.

Traditional banking still holds an edge in a few specific areas. If you’re buying commercial property, financing a large capital project, or operating in a sector that requires dedicated relationship management, a traditional bank’s credit underwriting capabilities and physical infrastructure are hard to replace. The problem is that you’re paying for those capabilities even when you don’t need them, which is the case for most routine transactions.

Hybrid banking is becoming the dominant model among growth-stage European SMEs. The logic is simple: use a digital platform for day-to-day payments, payroll, supplier settlements, and expense management, while maintaining a traditional banking relationship for lending and emergency liquidity. This approach captures efficiency gains without exposing your business to gaps in coverage.

| Business need | Best model |

|---|---|

| Routine SEPA transfers | Digital |

| Multi-currency supplier payments | Digital or hybrid |

| Commercial property lending | Traditional |

| Business card and expense management | Digital |

| Complex trade finance | Hybrid or traditional |

| Real-time cash flow visibility | Digital |

Here’s how to assess your own situation in practical terms:

- Map your payment flows. Categorize every transaction type by frequency, volume, and destination. This gives you a clear view of where costs accumulate.

- Identify your compliance profile. Some sectors face enhanced due diligence requirements that affect which platforms can serve them.

- Evaluate your credit needs. If you access business credit infrequently, digital may be sufficient. High credit dependency points toward hybrid.

- Assess your tech readiness. Digital banking platforms require API integrations, software adoption, and staff training.

Exploring modern banking trends shows that the industry is already moving toward platform-based financial management. Getting ahead of that shift now is a competitive advantage, not just a cost-saving measure. Also worth reviewing is solid business bank reconciliation practice, which becomes far simpler when your banking data is structured and API-accessible from day one.

Pro Tip: Even if you commit to a digital-first model, keep a traditional banking relationship active for lending access. The goal is optionality, not ideological purity. The businesses that navigate disruptions best are those with multiple financial pathways available.

How digital banking boosts European SME efficiency

With the right model in mind, what can SME owners actually expect when they transition to digital banking?

The operational improvements are concrete and measurable. Start with payment speed. SEPA Instant payments clear in seconds. SWIFT alternatives offered by modern fintech platforms typically settle in one business day rather than three to five. For a business managing supplier relationships across five countries, that difference in velocity changes how you negotiate payment terms and manage working capital.

Then there’s automation. Digital banking platforms connect to accounting software, ERP systems, and payroll tools through APIs. Instead of manually entering bank statement data or reconciling payments one by one, transactions flow directly into your accounts. This alone can save a small finance team four to eight hours per week, time that’s better spent on analysis and decision-making.

Consider a practical example. A Spanish manufacturer with suppliers in Poland and Hungary used a traditional bank for all payments. Reconciliation required a part-time bookkeeper every month. After switching to a digital platform with API integration, that same work took two hours. The manufacturer redirected that labor budget toward a second sales hire.

Here’s what digital banking delivers operationally:

- Real-time payment tracking so you always know exactly where funds are.

- Role-based access controls allowing finance team members to initiate or approve payments without sharing credentials.

- Virtual and physical business cards with transaction limits and category controls, reducing rogue spending.

- Multi-account structures that separate operating funds, tax reserves, and project budgets cleanly.

- Automated reconciliation that links every inbound payment to an outstanding invoice.

The neobanking market is projected to reach $7.97 trillion by 2031, with SMEs accounting for 65% of smart digital banking market share. These numbers reflect a structural shift, not a trend. Businesses adopting digital infrastructure now build institutional knowledge and process advantages that compound over time.

“The companies gaining the most from digital banking aren’t necessarily the largest—they’re the ones who connected their banking layer to every other operational system they use.”

For practical implementation guidance, streamlining digital banking workflows is a critical step, as is understanding how international payments efficiency ties directly to compliance and business growth planning. The ECB also confirms that instant payment interlinking boosts trade especially for SMEs in high-cost cross-border corridors.

Pro Tip: Integrate your payment platform with your accounting software before you migrate transaction volume. Starting with clean data from day one eliminates weeks of retroactive cleanup work.

Limitations and edge cases: Where digital banking still falls short

Efficiency is great, but SME owners must also be realistic about digital banking’s limits.

Pure digital banking platforms have made enormous strides, but they don’t solve every problem equally well. Knowing where the gaps are helps you build a banking strategy that doesn’t have unexpected holes.

Non-SEPA and non-euro payments remain costly. While digital platforms offer better rates than traditional banks for SWIFT payments, sending money to markets like Turkey, India, or Brazil still incurs meaningful fees and settlement delays. Even the most advanced fintech platforms depend on the same correspondent banking networks for these corridors. The savings are real but not dramatic. Edge cases involving non-SEPA and non-euro transactions are often best managed through hybrid or traditional banking relationships until truly global instant payment rails mature further.

Here are the scenarios where digital-only solutions most often fall short:

- Commercial real estate lending. Notary processes, legal due diligence, and mortgage structuring require traditional bank involvement in most EU jurisdictions.

- High-risk sector compliance. Businesses in sectors like crypto, gambling, arms, or certain financial services need enhanced due diligence that many digital platforms simply don’t support.

- Trade finance instruments. Letters of credit, documentary collections, and bank guarantees still rely heavily on traditional correspondent banking relationships.

- Emergency credit lines. When cash flow disruptions hit suddenly, traditional banks with established credit relationships can respond faster than newer digital platforms.

“Digital banking is not a universal replacement for traditional finance. It is a dramatically better default for routine operations. The mistake is assuming it eliminates the need for banking relationships entirely.”

Understanding SME risk management across different transaction types is essential for building a resilient financial structure. And if you’re starting fresh or expanding into a new EU market, reviewing a thorough guide to account opening in Europe helps you understand what documentation and compliance steps to prepare for. Don’t overlook the accounting compliance checklist for UK SMEs if you operate across the Channel, since UK and EU compliance requirements diverge in meaningful ways post-Brexit.

The bottom line: digital banking handles the vast majority of SME operational finance better and cheaper than traditional banks. But it works best as part of a broader financial strategy, not as a total replacement.

What most SMEs miss—and how to get digital banking right

Here’s the uncomfortable truth that most guides skip: switching to digital banking is not just a technology decision. It’s a change management challenge.

Most SME owners who struggle with digital banking adoption aren’t struggling because the platforms are difficult. They’re struggling because they migrated their entire payment operation at once, didn’t train their finance team on new workflows, and then blamed the platform when things felt chaotic. The platforms aren’t the problem. The transition strategy is.

The biggest blind spot we see consistently is the assumption that digital banking is inherently better in every scenario. It isn’t. Context determines value. A solo founder running a domestic consultancy in Germany gains different value from digital banking than a 50-person manufacturing business with suppliers across six non-SEPA countries. The efficiencies are real in both cases, but the implementation path looks completely different.

What actually works is a phased approach. Start by routing a defined subset of your payments through the new digital platform, ideally your highest-volume, most standardized transactions first. Monitor settlement times, reconciliation accuracy, and fee outcomes for 60 to 90 days before expanding. This pilot method lets you identify integration issues and workflow gaps without disrupting your entire operation.

The businesses that succeed with digital banking also maintain backup banking options deliberately. Not out of distrust for digital platforms, but because financial resilience requires redundancy. Keep a traditional account active for sector-specific lending, compliance requirements, or emergency liquidity scenarios. Following SEPA transfer best practices gives you a solid foundation for structuring your euro payment flows efficiently once the platform is running.

The owners who extract the most value from digital banking are not the most technologically sophisticated. They’re the ones who blended digital-speed operations with old-school risk discipline. Speed for execution. Caution for structure. That combination is what resilient cross-border SME finance actually looks like.

Upgrade your SME banking—next steps with Demivolt

Ready to upgrade your finances for efficiency and control? Here’s how Demivolt can help.

Business banking with Demivolt is built specifically for European SMEs managing cross-border operations. The platform offers dedicated IBAN accounts, SEPA and SWIFT payment management, virtual and physical business cards, and multi-account structures with role-based access. Onboarding is fast, fully digital, and compliant with EU regulatory standards, so you don’t wait weeks to get operational.

If you’re managing supplier payments across multiple currencies, issuing team expense cards, or simply tired of opaque bank fees eating into your margins, Demivolt’s infrastructure gives you real visibility and real savings. Explore the streamlined digital workflows that Demivolt clients use to reduce payment friction and take control of their cross-border finance from day one.

Frequently asked questions

How much can SMEs really save with digital banking on cross-border transfers?

SMEs can save at least 3x on fees compared to traditional banks, with savings reaching up to 12x for non-SEPA payments where legacy fee structures are most punishing.

Is digital banking always better for European SMEs than traditional banks?

Not always. Digital platforms excel for high-volume routine transactions, but traditional banks serve nuanced lending needs like commercial property finance and complex trade credit better than most digital alternatives.

Are there risks or limits to digital-only banking for high-risk sectors?

Yes. High-risk sectors require enhanced compliance due diligence, and not all digital platforms support the level of documentation and monitoring those sectors need, making hybrid or traditional arrangements necessary.

How do instant payment systems like TIPS boost SME trade?

Instant payment interlinking reduces transaction costs and speeds up cross-border settlements, delivering the most benefit for SMEs operating in high-cost payment corridors outside the core SEPA zone.

What’s the forecast for SME adoption of digital banking in Europe?

SMEs already represent 65% of digital banking market share, and the neobanking market overall is projected to reach $7.97 trillion by 2031, reflecting sustained structural growth driven largely by business users.