TL;DR:

- Payment fraud across the EU reached €4.2 billion in 2024, with digital banking offering solutions to address security and efficiency challenges.

- Modern digital banking streamlines onboarding, enhances compliance, and supports real-time, cost-effective cross-border payments.

Payment fraud across the European Economic Area reached €4.2 billion in 2024, a 17% increase year over year, with credit transfers alone jumping 24%. For European SMEs and e-commerce operators, that figure isn’t just a statistic — it’s a direct threat to cash flow, customer trust, and regulatory standing. The good news is that modern digital banking was built precisely to address these problems. This article walks you through what digital banking actually means in practice, how it compares to traditional payment rails, and which tools give your business a measurable compliance and cost advantage in 2026.

Table of Contents

- Why digital banking matters for EU SMEs

- What makes digital banking different?

- SEPA Instant vs. card payments: Costs, speed, and compliance

- Fast, compliant cross-border payments in 2026

- Our take: What most digital banking guides miss

- Next steps: Modern banking with Demivolt

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Digital banking cuts SME costs | Open banking and SEPA Instant payments reduce transaction fees for European SMEs. |

| Compliance and security first | Modern digital banks use real-time compliance tools and strong authentication to fight growing fraud risks. |

| Cross-border payments made easy | New platforms allow SMEs to send and receive money instantly, even in multi-currency environments. |

| Onboarding remains a hurdle | SMEs still face bank onboarding rejections, making digital banking choices crucial for growth. |

Why digital banking matters for EU SMEs

If you’ve tried opening a traditional business bank account in the last few years, you already know the frustration. SME onboarding challenges are not just anecdotal complaints. According to the ECB SAFE Survey Q1 2026, a net 24% of European SMEs reported higher bank interest rates in Q1 2026, and the composite financing gap widened by 3%. SMEs represent 99% of all EU businesses and generate over half of total turnover, yet they face a 7% onboarding rejection rate and severe credit constraints — reaching as high as 37.8% in Germany.

These aren’t minor inconveniences. When a growing business cannot access credit or open a compliant account quickly, it loses time, opportunities, and momentum. Every week spent navigating slow onboarding is a week you’re not executing on growth.

Beyond financing, compliance obligations are intensifying. The EU’s AML (anti-money laundering) rules, PSD2 requirements, and upcoming PSD3 updates are pushing businesses to document every payment and demonstrate due diligence. Failure to do so carries real regulatory and reputational consequences.

Here’s a clear picture of what’s pushing European SMEs toward digital banking solutions:

- Slow traditional onboarding: Legacy banks can take weeks to verify and approve business accounts, creating cash flow delays for new operations

- High rejection rates: 7% of SMEs are turned away outright, with small operators and startups disproportionately affected

- Cross-border friction: Multi-currency payments through correspondent banking networks add fees, delays, and foreign exchange risk

- Rising fraud exposure: Credit transfer fraud alone costs EU businesses billions annually, and users bear 85% of losses on unauthorized transfers

- Compliance complexity: Meeting KYC, AML, and SCA obligations across multiple jurisdictions strains small finance teams

“The financing gap and fraud burden are not separate problems. They both stem from the same root cause — legacy infrastructure that was designed for a different era of commerce. Digital banking is the structural fix.”

Modern digital banking trends are directly responding to these pain points by offering purpose-built infrastructure for today’s business model.

What makes digital banking different?

The short answer: digital banking removes the middlemen, automates compliance, and gives you real-time visibility into every payment. The long answer requires unpacking a few core technologies.

Open banking via PSD2 APIs is foundational. Open banking explained in plain terms means that banks and payment service providers are required under EU law to open their data and payment systems via standardized APIs. This allows your business software, accounting tools, or custom platforms to initiate payments (PIS — Payment Initiation Services) or access account information (AIS — Account Information Services) directly.

As PSD2 APIs enable account-to-account (A2A) transactions that bypass card networks entirely, delivering lower costs, real-time confirmation, and built-in Strong Customer Authentication (SCA). Compared to cards — which route through acquirers, card schemes, and issuers, adding layers of fees and chargeback risk — open banking A2A flows are cleaner and more direct.

Key features that distinguish digital banking from traditional setups:

- SEPA Instant payments: Near-real-time euro transfers, available 24/7/365, no batch processing delays

- Virtual and physical business cards: Issued instantly with spend controls and role-based access for team members

- Multi-account structures: Separate IBANs for different business functions, subsidiaries, or currency accounts

- Built-in compliance tools: Automated KYC checks, transaction monitoring, and audit trails that satisfy AML obligations

- API integrations: Connect your ERP, accounting software, or e-commerce platform directly to your banking layer

Pro Tip: When evaluating digital banking platforms, ask specifically whether their compliance tools are embedded in onboarding or bolted on afterward. Embedded compliance is faster and generates cleaner audit trails.

The practical difference is stark. A traditional bank might take 10 to 15 business days to onboard your company. A well-built digital banking platform can verify your business documents and open a functional IBAN account in hours, with payment capability from day one. Business account benefits extend beyond speed — you get ongoing transaction transparency that legacy banks struggle to match.

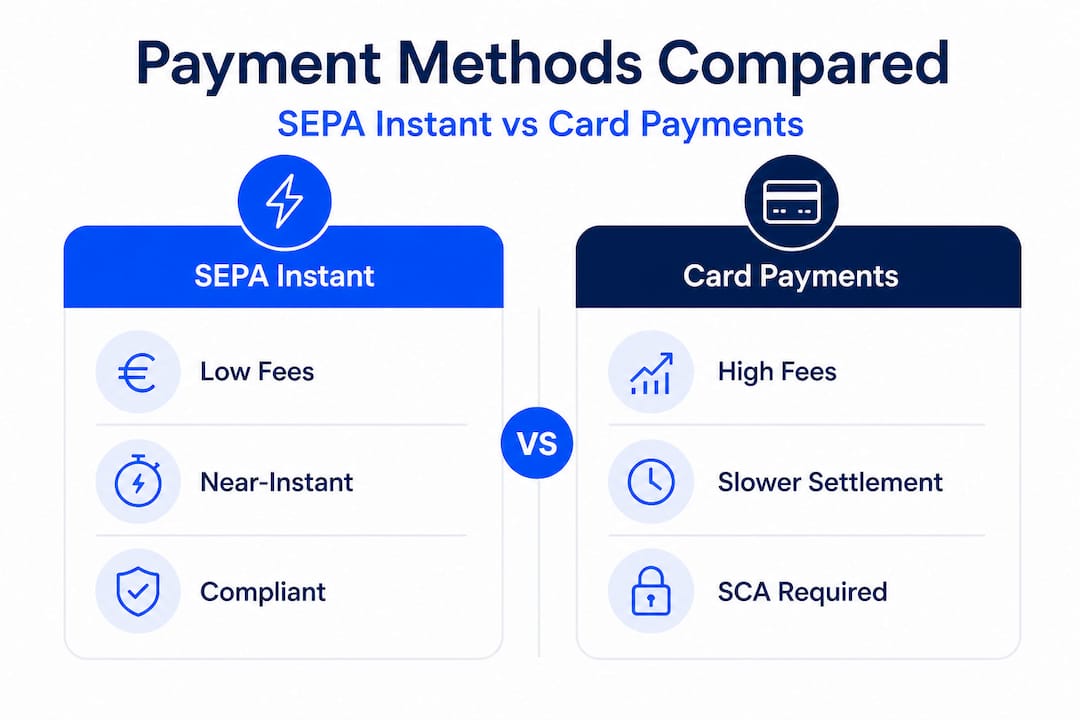

SEPA Instant vs. card payments: Costs, speed, and compliance

This comparison matters more in 2026 than it ever has. SEPA Instant is now mandatory for euro-zone payment service providers, and its adoption is reshaping what businesses should expect from their payment infrastructure.

| Feature | SEPA Instant | Card payments |

|---|---|---|

| Transaction fee | Zero to low flat fee | 0.5% to 3% MDR (merchant discount rate) |

| Speed | Up to 10 seconds | T+1 to T+3 settlement |

| Chargebacks | None (VoP protects against misdirected payments) | High exposure, expensive to dispute |

| SCA compliance | Built in | Depends on issuer implementation |

| Currency | Euro only | Multi-currency |

| Availability | 24/7/365 | Subject to card network uptime |

| Mandatory status | Required for euro PSPs by 2025/27 | Voluntary |

SEPA Instant volumes now represent 17% to 23% of total SEPA payment volume, and that share is climbing fast as the mandatory rollout accelerates. The zero-chargeback model alone is a major advantage for e-commerce operators who routinely lose 0.5% to 1% of revenue to disputed card transactions.

Here’s how to decide when SEPA Instant is the smarter choice over cards:

- High-value B2B transactions: Card MDR on a €50,000 invoice could cost €1,500. SEPA Instant typically costs a fraction of that, often under €1.

- Recurring supplier payments: Automate and schedule SEPA Instant transfers instead of managing card-on-file arrangements that expire or get blocked.

- Time-sensitive settlements: When cash flow timing matters — for example, paying a supplier to secure stock — 10-second settlement beats a 3-day card clearing cycle.

- Compliance-sensitive industries: SEPA Instant’s built-in SCA and Verification of Payee (VoP) reduce fraud exposure without adding friction for your team.

Pro Tip: If your business sells to other European businesses rather than consumers, SEPA Instant should be your default payment rail. The cost savings compound quickly across a year’s worth of transactions.

SEPA transfer best practices include keeping your payee list clean and verified, using VoP to confirm recipient IBANs before every new payment, and setting up pre-authorized payment templates for your regular counterparties. SEPA payments explained in detail give you the full regulatory context for building a compliant payment workflow.

Fast, compliant cross-border payments in 2026

If you operate across EU borders or sell to markets like Sweden, Denmark, or Poland where the euro isn’t the local currency, cross-border payment speed has traditionally been your biggest operational headache.

That changed significantly in late 2025. The ECB’s TIPS (TARGET Instant Payment Settlement) infrastructure now supports cross-currency interlinking, connecting euro SEPA Instant flows with Swedish SEK and Danish DKK since October 2025. This means a eurozone SME paying a Swedish supplier no longer waits days for a correspondent bank chain to complete the transfer.

What this means for your business in practical terms:

| Currency pair | Old method | New TIPS method |

|---|---|---|

| EUR to SEK | 2 to 4 days via SWIFT/correspondent | Near-instant via TIPS interlinking |

| EUR to DKK | 1 to 3 days | Near-instant via TIPS interlinking |

| EUR to EUR (cross-border SEPA) | Same day to next day | Under 10 seconds |

The digital euro pilot adds another dimension to watch. While the ECB’s retail digital euro currently targets consumer use, its infrastructure could eventually support business-to-business non-euro transactions with defined holding limits. SMEs should monitor this closely because it could reshape liquidity management for multi-currency operations.

Key regulatory developments to track in 2026:

- PSD3 draft implementation timelines and what they mean for open banking API standards

- DORA (Digital Operational Resilience Act) requirements for third-party fintech providers your business relies on

- EU AML Authority (AMLA) oversight expansion affecting cross-border payment screening obligations

- VoP (Verification of Payee) rollout across all EU member states, expected to reduce misdirected payment fraud significantly

SWIFT payment tips remain relevant for non-EU cross-border payments, particularly for markets in North America, Asia, and the Middle East where SEPA infrastructure doesn’t apply. For intra-EU flows, however, SEPA Instant and TIPS are quickly making SWIFT redundant.

Statistic callout: Cross-currency TIPS payments went live across EUR, SEK, and DKK in October 2025, marking the first time real-time settlement worked across different European currencies without a correspondent bank intermediary.

To streamline banking workflows for cross-border operations, the practical recommendation is to consolidate your payment infrastructure under a single platform that supports both SEPA Instant and SWIFT, gives you multi-IBAN capability, and offers API access so your finance team isn’t manually processing every international payment.

Our take: What most digital banking guides miss

Most digital banking content focuses on features. Speed. Fees. APIs. That’s useful, but it misses the harder truth: technology doesn’t solve cross-border payment pain on its own. Implementation, oversight, and compliance discipline are what actually determine whether your business benefits.

Here’s what we’ve consistently observed: SMEs that switch to digital banking and then try to run it like a traditional bank account end up disappointed. They automate the payment rails but skip the compliance workflows. They get SEPA Instant access but don’t set up payee verification. Then a misdirected payment or a fraud incident lands on their desk, and they blame the platform.

The ECB data tells the real story. Credit transfer fraud rose 24% in 2024, and users bear 85% of losses on unauthorized transfers. SCA reduces fraud risk dramatically — fraud is 17 times higher for non-EEA cards without SCA enabled — but only if you actually implement it correctly and don’t override it for convenience.

Compliance isn’t the boring part of digital banking. It’s the part that protects your margin.

We’ve also seen businesses underestimate the onboarding quality of their chosen platform. A fast onboarding process is great. But a fast onboarding process backed by robust KYC and ongoing transaction monitoring is what keeps you compliant and keeps your account operational 12 months later. Ask every platform you evaluate: what happens after onboarding? What triggers a review? How do you notify me?

The third blind spot: fraud tactics evolve faster than most guides acknowledge. Social engineering, manipulation of SCA exemptions, and APP (authorized push payment) scams are growing threats that go beyond what built-in fraud tools alone will catch. The businesses that stay protected combine platform-level controls with human review protocols for any new or unusual payment instructions.

Rising payment fraud in 2026 is not a technology problem that will be solved by a better API. It requires a culture of financial vigilance, not just a better dashboard.

Next steps: Modern banking with Demivolt

Putting digital banking principles into practice starts with choosing the right infrastructure partner — one that handles compliance, payment speed, and operational flexibility without requiring you to stitch together five different tools.

Demivolt business banking is built precisely for the SMEs and e-commerce businesses this article speaks to. You get dedicated IBAN accounts, SEPA and SWIFT payment capabilities, virtual and physical business cards with role-based access, and onboarding that meets EU regulatory standards from day one. Funds are held in segregated accounts, giving you the protection and transparency your business operations require. If you want to go deeper on the open banking layer and how it integrates with your existing workflows, you can explore open banking on the Demivolt blog and see exactly how A2A payments and PSD2 API access can reduce costs for your business.

Frequently asked questions

What is SEPA Instant and how can it help my SME?

SEPA Instant is a euro payment rail that settles transfers in under 10 seconds, with low or zero fees compared to the 0.5% to 3% merchant discount rate on card transactions — and no chargeback risk. For SMEs managing cash flow, it’s a faster and cheaper alternative to card-based B2B payments.

Do digital banks help reduce payment fraud?

Yes. Digital banking platforms implement Strong Customer Authentication by default, and SCA reduces fraud exposure dramatically: non-EEA cards without SCA experience fraud rates 17 times higher than SCA-protected transactions. Real-time monitoring adds another layer of detection for unusual patterns.

How does open banking cut costs for small businesses?

PSD2 API-powered A2A payments bypass card networks entirely, removing the acquirer, card scheme, and issuer from the payment chain. That elimination of intermediaries directly reduces transaction costs and simplifies reconciliation for small businesses.

Are digital cross-border payments really instant now?

For key European currency pairs, yes. TIPS interlinking launched in October 2025 connects euro SEPA Instant payments with SEK and DKK, enabling near-instant cross-border settlements for compliant European businesses without going through correspondent bank chains.

Recommended

- Demivolt | Blog – How to streamline your digital business banking workflow

- Demivolt | Blog – Business banking for SMEs: services, compliance & cross-border

- Demivolt | Blog – International payments for SMEs: efficiency, compliance, growth

- Demivolt | News – How fintechs facilitate cross-border payments for SMEs