TL;DR:

- Proper process design ensures compliance, reduces reconciliation, and prevents unauthorized spending.

- Modern EMI platforms enable instant virtual card issuance, scaling, and better cross-border fee management.

- Ongoing policy review and controls are vital for long-term success and operational efficiency.

Foreign exchange fees eating into your margins, employees making unauthorized purchases, and reconciliation piling up at month-end — these are not edge cases. They’re the daily reality for finance managers running business card programs across Europe. The good news is that a well-designed card issuance process eliminates all three problems before they start. This guide walks you through every stage, from choosing the right partner to optimizing spend controls, so you can launch a card program that actually works for a modern, cross-border SME.

Table of Contents

- What you need to get started

- Step-by-step business card issuance process

- Designing spend controls and approval workflows

- Common pitfalls and troubleshooting tips

- Expected results and program optimization

- Our take: Why business card issuance success is about process, not just product

- Ready to simplify your SME card program?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Five-step process | Follow a proven five-step process from purpose definition to card issuance and launch. |

| Instant virtual cards | Virtual cards can be issued instantly and are ideal for cross-border SME spend control. |

| Compliance matters | KYC/KYB checks and PSD2 compliance are essential for a smooth, legal program launch. |

| Hybrid programs boost flexibility | Combining virtual and physical cards increases acceptance and control for SMEs. |

| Significant cost savings | Consolidating card solutions can save SMEs up to €20,000 annually. |

What you need to get started

Before you issue a single card, you need the right foundation. Skipping this step is the single most common reason card programs stall or create compliance headaches later.

Core requirements

According to card issuing for business, the issuance process for European SMEs typically involves five key steps, starting with selecting a compliant issuing partner. That partner must be either an Electronic Money Institution (EMI) or a licensed bank operating under PSD2, which is the EU’s Payment Services Directive. PSD2 requires strong customer authentication, transparent fee disclosure, and strict data handling. If your partner is not PSD2 compliant, you face legal exposure and potential account freezes.

Here’s what you’ll need ready before you begin:

- Issuing partner: An EMI or bank with PSD2 authorization and Mastercard or Visa certification

- KYC/KYB documents: Company registration, ownership structure, director ID, and proof of address

- ERP or accounting system: For integration with expense data (Xero, QuickBooks, SAP, or similar)

- Spend policy draft: A written set of rules governing card limits, merchant categories, and approval flows

- Cross-border jurisdiction mapping: A list of countries where employees will spend, so you can verify EMI passporting rights

EMI passporting is particularly important for cross-border SMEs. It means your issuing partner’s EU license is recognized across member states without requiring separate local licenses. If you’re opening a business bank account for the first time in Europe, choosing a partner with multi-market EMI authorization saves significant time and legal cost.

Platforms built on pre-integrated Mastercard infrastructure, such as those connected to Mastercard Product Express, dramatically accelerate the compliance and technical setup. Instead of building integrations from scratch, you get pre-certified modules that already meet EU regulatory standards.

| Requirement | Traditional bank | Modern EMI/fintech |

|---|---|---|

| PSD2 compliance | Yes, but slow to verify | Built in, automated |

| KYC/KYB timeline | 5-15 business days | 1-3 business days |

| Multi-market passporting | Limited | 30 to 60+ markets |

| ERP integration | Manual/custom | Pre-built API connectors |

| Virtual card support | Rare | Standard |

Understanding the account benefits for SMEs available through modern fintech platforms makes it much easier to justify the switch from a traditional banking setup.

Pro Tip: Choose an issuing partner certified for 60 or more markets from day one. Your business footprint will almost certainly grow, and retrofitting a limited platform is far more expensive than starting with one that scales.

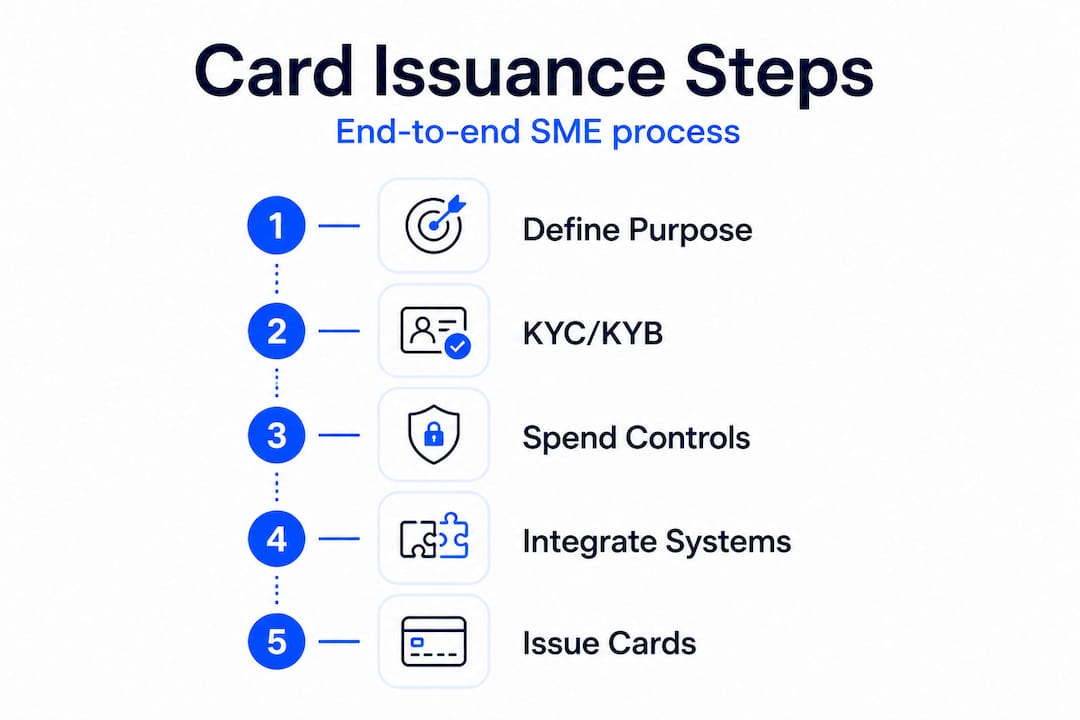

Step-by-step business card issuance process

Once your documents, partner, and internal policies are lined up, execution becomes straightforward. The five steps below are drawn from real SME deployments across Europe.

Step 1: Identify your purpose and choose your issuing partner. Decide whether you need cards for employee travel, vendor payments, project budgets, or a mix. This determines the card types (virtual, physical, or hybrid) and the controls you’ll need. Then finalize your EMI or bank partner based on the market coverage, fee structure, and integration options you mapped in the preparation phase.

Step 2: Complete KYC/KYB verification. Submit your corporate documents through your partner’s onboarding portal. Most modern platforms complete this in 1-3 days. Delays happen when documents are incomplete or when beneficial ownership structures are complex. Prepare a clean corporate structure chart in advance to avoid back-and-forth.

Step 3: Design spend policies, limits, and controls. Set per-card daily and monthly limits, restrict merchant category codes (MCCs) to relevant spend types, and define who approves card requests. This step is covered in greater depth in the next section, but don’t rush it. Poorly designed policies cause more reconciliation problems than any technical issue.

Step 4: Integrate with your accounting or ERP system. Map card transactions to your chart of accounts, set up automated receipt matching, and configure real-time reporting. If your ERP does not have a native connector, most modern issuing platforms provide API documentation for custom integration.

Step 5: Issue cards and launch with testing. Virtual cards can be issued instantly, with zero wait time after approval. Physical cards typically take 3-7 business days for delivery. Always run a controlled test with two or three internal users before rolling out to the full team. Verify that spending triggers the correct accounting entries, approval notifications fire correctly, and declined transactions are logged properly.

| Feature | Virtual card issuance | Traditional bank physical issuance |

|---|---|---|

| Issuance speed | Instant (0 seconds) | 5-10 business days |

| Volume scalability | Unlimited per account | Limited, manual requests |

| Spend controls | Real-time, granular | Basic, often post-purchase |

| Cross-border FX fees | Often 0% with modern EMIs | 1.5-3.5% per transaction |

| 3D Secure | Standard | Varies |

| Integration with ERP | API-native | Manual export/import |

Platforms operating under Mastercard Product Express give SMEs access to pre-certified compliance and faster program launches, which is especially valuable if you’re targeting multiple EU markets simultaneously.

For a more detailed walkthrough on the virtual card component, the guide on issuing virtual cards covers platform selection, policy setup, and API integration in practical terms.

Pro Tip: Start with virtual-only issuance for your first 30 days. It’s faster, cheaper to test, and lets you validate your spend controls before committing to physical card logistics.

Designing spend controls and approval workflows

Control and approval design is where many programs succeed or fail. A card program without solid controls is a liability. One with overly rigid controls frustrates employees and defeats the efficiency gain.

Key controls to configure

- Spend limits: Set daily, weekly, and monthly caps per card and per cardholder role

- Merchant category codes (MCCs): Whitelist or blacklist specific merchant types (e.g., allow SaaS subscriptions, block gambling)

- Card type rules: Single-use virtual cards for one-time vendor payments, recurring virtual cards for subscriptions, physical cards for travel

- Geographic restrictions: Limit cards to specific countries or regions to prevent out-of-scope spend

- ATM access: Disable ATM withdrawals on virtual cards by default, as most virtual cards do not support ATM use

Approval workflows add a second layer of protection. Before a card is issued or a limit is raised, require sign-off from a finance manager. This pre-issuance approval step is the most effective single control you can implement to prevent misuse. For cross-border operations, compliance best practices specifically recommend mapping approval workflows to jurisdiction, so that cards used in higher-risk markets require additional sign-off.

Poor spend controls don’t just create fraud risk. They create audit risk. If your card transactions can’t be tied to approved budgets and policy-compliant merchants, your finance team faces weeks of manual reconciliation every quarter. That time has a real cost, and it compounds as your headcount grows.

Hybrid programs, where some employees carry physical cards for in-person vendor acceptance and virtual cards for online spend, are increasingly common. The key is setting distinct policies for each card type rather than applying a blanket rule. A sales team member traveling to a trade fair has different needs than a marketing manager buying digital advertising.

Reviewing modern banking trends for compliance shows that role-based user management is becoming a baseline expectation, not a premium feature. Build your workflows around roles, not individuals, so that controls hold even when team members change.

Pro Tip: Before you scale, run a full test cycle with a small group. Trigger edge cases deliberately: try spending at a blocked merchant, exceed a limit, and submit a request without approval. Fix what breaks before it breaks at scale.

Common pitfalls and troubleshooting tips

Even well-planned card programs hit problems. Knowing where things typically go wrong lets you troubleshoot faster and avoid the most costly mistakes.

Inadequate KYC/KYB preparation. The most common launch delay. Companies submit documents that are outdated, missing ultimate beneficial owner information, or formatted incorrectly for the platform. Fix: Create a KYC/KYB document pack before you begin onboarding, reviewed by someone familiar with EU AML requirements.

Integration failures. When card data does not flow correctly into your ERP, you end up with reconciliation issues that take weeks to untangle. Fix: Test every integration in a sandbox environment before going live. Map transaction fields manually if needed to ensure every entry lands in the right account.

Ignoring hybrid card needs. Issuing only virtual cards works for most online spend, but it creates friction when employees need to pay vendors who only accept physical cards. Fix: Build a small physical card allocation from day one, even if most of your program is virtual.

Skipping policy review cycles. Card policies set at launch quickly become outdated as your business grows into new markets or changes spend patterns. Fix: Schedule a policy review every quarter in your finance team calendar.

Underestimating consolidation savings. Many SMEs run multiple card products simultaneously, which multiplies fees and admin overhead. Consolidating onto a single platform saves up to €20,000 per year versus running fragmented card programs, with additional savings from reduced invoice processing costs.

Following SEPA transfer best practices alongside your card program ensures that your full payment stack, both card spend and bank transfers, operates under consistent controls and reporting standards.

Expected results and program optimization

Once your card program is live and controls are validated, the benefits compound quickly. Here’s what a well-run program delivers:

- No FX fees on cross-border spend with modern EMI platforms (up to €20,000/month for some providers)

- Instant virtual card issuance for new hires, project teams, or urgent vendor payments

- Lower reconciliation workload, with automated receipt matching and real-time reporting replacing manual exports

- Audit-ready records, with full transaction logs linked to approved budgets and spend policies

- 1% cashback on qualifying spend with select platforms, adding passive savings to your finance results

The empirical benchmarks from consolidated SME card programs show up to €20,000 in annual savings versus managing multiple card products, along with measurable reductions in invoice processing costs.

| Metric | Legacy multi-card setup | Consolidated modern program |

|---|---|---|

| Annual card program cost | €20,000+ | Significantly lower |

| FX fee per transaction | 1.5-3.5% | 0% (up to €20k/month) |

| Reconciliation time per month | 15-25 hours | 3-5 hours |

| Card issuance time | 5-10 days (physical) | Instant (virtual) |

| Audit trail quality | Manual, incomplete | Automated, complete |

For ongoing optimization, review your spend analytics quarterly. Look for categories where employees consistently approach limits (a signal to adjust policies, not just raise limits), and identify any merchant codes that generate disputed or unrecognized transactions. Scaling your hybrid setup by region, adding physical cards only in markets that require them, keeps costs in check while maintaining coverage.

Exploring international payment efficiency for SMEs gives additional context on how card programs fit into a broader cross-border payment strategy, including SWIFT and SEPA alignment.

Our take: Why business card issuance success is about process, not just product

Here’s an uncomfortable truth most fintech providers won’t tell you: the platform matters far less than the process you build around it.

We’ve seen SMEs buy into sophisticated card issuance platforms, complete with real-time dashboards and API-grade controls, and still end up with unauthorized transactions, messy reconciliation, and frustrated employees within six months. The reason is almost always the same. They treated card issuance as a one-time technology purchase rather than an ongoing operational practice.

One concrete example: a fast-growing e-commerce business automated its card approval workflow using a modern EMI platform. The tech worked perfectly. But no one tested what happened when an employee requested a card for a merchant category that should have been blocked. The control was configured incorrectly, the test was never run, and for three months, out-of-policy purchases flowed through undetected. Cleaning it up cost more in finance team hours than the savings from switching platforms in the first place.

The businesses that get the best long-term return from card programs are the ones that treat policy design and integration testing as seriously as they treat product selection. They revisit controls every quarter, not just at launch. They assign clear ownership to the card program, typically a finance manager with authority to approve and revoke access. And they track not just spend, but policy adherence, flagging any transaction that hit an edge case even if it was ultimately approved.

Following business banking trends shows that the highest-performing SMEs increasingly treat their card programs as a live financial control system, one that evolves with the business rather than sitting static after launch.

Pro Tip: Put an annual policy review on your finance calendar from day one. Your business will look different in twelve months. Your card controls should reflect that.

Ready to simplify your SME card program?

Demivolt is built specifically for SMEs that need compliant, efficient, and scalable financial infrastructure across Europe. From dedicated IBAN accounts to virtual and physical card issuance with real-time spend controls, the platform handles the complexity of cross-border payments so your finance team can focus on strategy rather than administration.

Whether you’re launching your first card program or consolidating a fragmented multi-card setup, Demivolt’s business banking solutions give you the tools to move fast without cutting corners on compliance. Explore the step-by-step virtual card issuance guidance to see exactly how Demivolt supports each stage of the process, from KYC onboarding through to spend analytics and ERP integration. Your card program should be an asset, not an administrative burden.

Frequently asked questions

How long does it take to issue a virtual business card?

Virtual cards enable instant issuance — literally 0 seconds after approval — through most modern fintech platforms, making them ideal for urgent or high-volume card needs.

What compliance checks are required for SME card issuance?

KYC/KYB verification is mandatory under EU AML and PSD2 rules, and typically takes 1-3 days to complete when your documents are prepared and submitted correctly.

Can SMEs get both physical and virtual cards?

Yes, most European EMI platforms support hybrid virtual/physical programs, which are especially useful when some vendors only accept physical card payments.

Are there cost savings when consolidating multiple cards into one solution?

Consolidating onto a single card platform saves up to €20,000 per year versus managing multiple fragmented card products, in addition to lower FX fees and reduced reconciliation time.

What’s the main difference between fintech and traditional bank card issuance?

Fintechs offer instant API issuance with no personal liability and better FX rates, while traditional banks typically require guarantees and take significantly longer to process physical card requests.

Recommended

- Demivolt | Blog – How to issue virtual cards for SME finance teams: 2026

- Demivolt | Blog – How to manage multiple accounts: A step-by-step guide for SMEs

- Demivolt | Blog – Types of Business Bank Accounts: Find the Right Fit for Your SME

- Demivolt | Blog – Business banking for SMEs: services, compliance & cross-border