TL;DR:

- Virtual cards offer instant issuance and granular spend controls for European SME finance teams.

- Proper preparation, including platform selection and compliance, is essential before issuing virtual cards.

- Hybrid programs combining virtual and physical cards maximize vendor acceptance and operational flexibility.

Reimbursement cycles that drag on for weeks, receipts lost in email threads, and zero visibility into who spent what. These are not minor inconveniences for European SME finance teams. They are real compliance risks and cash flow problems. European SMEs rely on platforms like Payhawk and Revolut Business for instant virtual card issuance with granular expense controls, and for good reason. Virtual cards cut through the noise by giving your team instant, controlled spending power without the chaos of traditional card programs or slow reimbursement workflows. This guide walks you through everything you need to know to issue and optimize virtual cards for your finance team.

Table of Contents

- Understanding virtual cards: What, why, and how they work

- Preparing to issue virtual cards: What finance teams need

- Step-by-step process: How to issue virtual cards effectively

- Common pitfalls and troubleshooting virtual card programs

- A fresh perspective: Why a hybrid approach and supplier enablement fuels real results

- Business banking built for SME finance teams

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Fast issuance | Virtual cards can often be issued instantly after regulatory checks, offering immediate access for SME teams. |

| Granular controls | Finance teams gain powerful spend controls to automate reconciliation, reduce reimbursements, and improve compliance. |

| Hybrid is optimal | A mix of virtual and physical programs with supplier enablement delivers the best results for modern expense management. |

| Platform selection matters | Choosing the right licensed partner and platform is key to fast, compliant virtual card rollout. |

Understanding virtual cards: What, why, and how they work

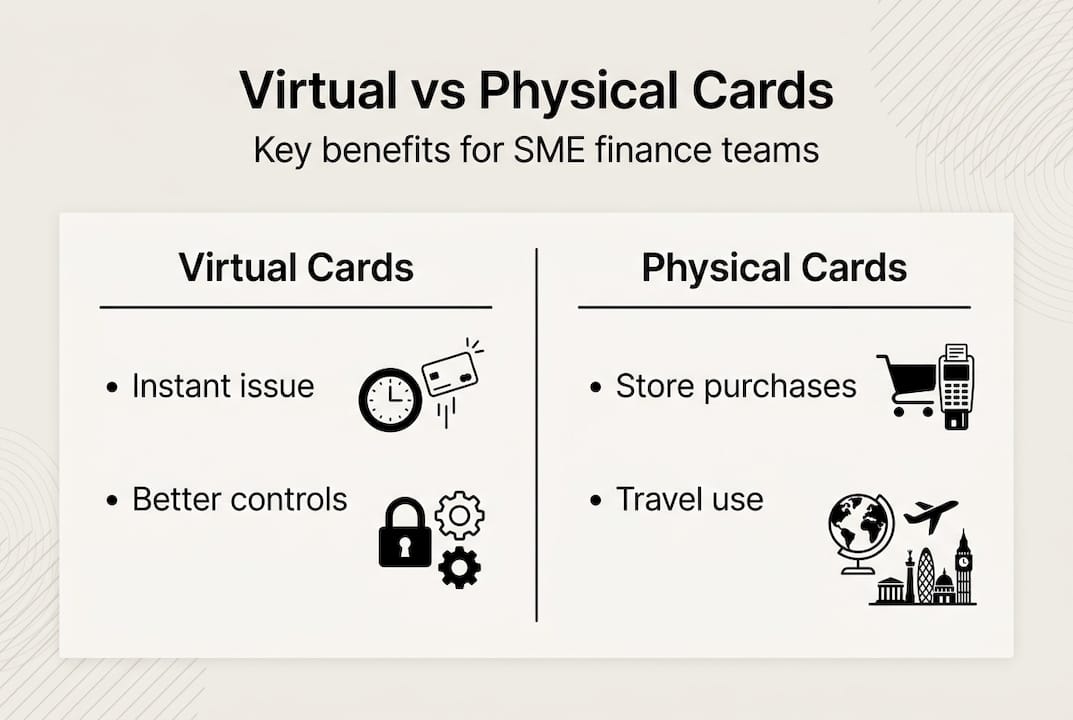

A virtual card is a digitally generated payment card with a unique card number, expiration date, and CVV. It lives entirely online. No plastic, no courier wait, no lost cards. Your finance team can generate one in seconds, assign it to a specific vendor or employee, set a spending limit, and deactivate it the moment the transaction is done.

The difference between virtual and physical cards is not just format. It is function. Physical cards are flexible for in-person purchases, travel, and point-of-sale payments. Virtual cards are purpose-built for online transactions, accounts payable automation, SaaS subscriptions, and supplier payments. Each virtual card can be single-use or recurring, capped at a fixed amount, and locked to a specific merchant category.

For European SMEs, this level of control matters enormously. The virtual card market is projected to reach USD 24.54 billion by 2031, reflecting how fast businesses are moving away from legacy expense tools. And it is not just about convenience. T&E expenses and AI-driven spend grew significantly in recent years, making automated spend controls a strategic priority rather than a nice-to-have.

Key benefits of virtual cards for SME finance teams:

- Instant issuance: No waiting for card delivery. Issue within seconds after setup.

- Granular spend controls: Set limits by amount, merchant type, or time period.

- Real-time tracking: See every transaction the moment it happens.

- Reduced reimbursements: Employees spend directly from company funds, eliminating out-of-pocket cycles.

- ERP and accounting integration: Sync transactions automatically with tools like Xero, NetSuite, or SAP.

- Fraud reduction: One-time use numbers mean stolen credentials are useless.

Leading platforms serving European SMEs include Payhawk, Pleo, Spendesk, Wise Business, and Revolut Business. Each offers varying degrees of integrated expense management with different fee structures and compliance frameworks. Choosing the right one depends on your team size, transaction volume, and ERP ecosystem.

| Feature | Virtual cards | Physical cards |

|---|---|---|

| Issuance speed | Instant | 5 to 10 business days |

| Spend controls | Granular (amount, merchant, date) | Limited |

| Use case | Online, AP, SaaS, subscriptions | POS, travel, in-person |

| Fraud risk | Very low (single-use available) | Moderate |

| ERP integration | Seamless via API | Manual reconciliation |

| Reimbursement need | Rarely | Frequently |

Preparing to issue virtual cards: What finance teams need

Before you issue a single virtual card, your team needs to clear a few important hurdles. Skipping preparation is the fastest way to create compliance headaches down the road.

Here is what you need in place before you start:

- Platform selection: Choose between fintech-native platforms and traditional banks. Fintech options typically move faster and offer better API flexibility.

- KYC completion: Know Your Customer verification is mandatory. Platforms enable instant card issuance after KYC with robust controls, so completing this step unlocks everything else.

- PSD2 compliance: The Payment Services Directive 2 governs how non-banks can issue payment instruments in Europe. PSD2 enables non-banks to issue virtual cards rapidly, sometimes in as little as 28 days from program launch.

- ERP or accounting integration: Map out which systems need to connect. This determines whether you use API-based or file-based data sync.

- Spend policy design: Define who can hold cards, what categories are allowed, and what the approval workflow looks like.

Fintech platforms vs. traditional banks for virtual card issuance:

| Criteria | Fintech platforms | Traditional banks |

|---|---|---|

| Onboarding speed | Days to weeks | Weeks to months |

| Virtual card issuance | Instant post-KYC | Often delayed |

| API availability | Strong, developer-friendly | Limited or legacy |

| Spend controls | Highly configurable | Basic |

| Compliance support | Built-in PSD2 tools | Manual processes |

| Cost structure | Transparent, usage-based | Often opaque |

For regulated issuance, your platform must work with licensed EMI/Bank partners to stay on the right side of EU payment law. This is non-negotiable.

Pro Tip: Do not try to roll out virtual cards across every spend category at once. Start with a pilot program for a single category like SaaS subscriptions or travel bookings. You will spot integration issues early, build internal confidence, and show measurable ROI to leadership before scaling.

Step-by-step process: How to issue virtual cards effectively

With your foundation in place, here is a clear, actionable process your finance team can follow to issue and manage virtual cards from day one.

Step 1: Choose your platform and verify regulatory requirements Confirm your chosen platform is licensed to operate in your country and supports PSD2-compliant issuance. Check whether they partner with a licensed EMI or bank for card scheme access.

Step 2: Complete KYC and onboard your users Submit business verification documents and complete individual KYC for card holders. Most fintech platforms process this digitally within one to three business days. Role-based access should be configured here so finance managers and department heads have the right permissions.

Step 3: Design your spend policies Before issuing any cards, define your rules. Which merchant categories are allowed? What are the per-transaction and monthly limits? Who approves exceptions? Document this clearly so every card holder understands the boundaries.

Step 4: Issue cards via API, batch upload, or portal Most platforms offer three methods. The portal is the simplest for small teams. Batch upload works well for issuing multiple cards at once. API integration is best for high-volume or automated issuance, and embedded card issuing via API can reduce program launch time from a full year down to just 28 days.

Step 5: Integrate with your accounting or ERP system Connect your card platform to your accounting software. This is where you automate reconciliation by mapping transaction data directly to cost centers, projects, or GL codes. Real-time feeds eliminate manual data entry and cut month-end close time dramatically.

Step 6: Monitor, review, and optimize Set up dashboards to track spend by card, category, and department. Review policies quarterly. Adjust limits based on actual usage patterns.

The momentum behind this shift is real. 88% of EU businesses are using or strongly considering virtual cards in 2026. If your team is not already moving in this direction, your competitors likely are.

Pro Tip: Look for platforms that support multi-currency virtual cards and flexible credentials. This is especially useful for cross-border payments where FX costs and currency mismatches can quietly erode your margins.

Common pitfalls and troubleshooting virtual card programs

Even well-prepared teams run into problems. Knowing what to expect makes the difference between a stalled rollout and a smooth one.

The most common pitfalls include:

- Supplier non-acceptance: Some vendors still cannot or will not accept virtual card payments, especially in manufacturing or logistics sectors.

- Legacy ERP limitations: Older accounting systems may not support real-time transaction feeds, forcing manual workarounds.

- Unclear spend policies: Without well-defined rules, employees overspend, use wrong merchant categories, or create reconciliation nightmares.

- Finance and procurement misalignment: When these two teams are not coordinating, duplicate controls and approval bottlenecks appear.

- Underestimating onboarding time: Even with fast platforms, internal change management takes time. Training matters.

Solutions that actually work:

For supplier resistance, run a structured supplier enablement campaign. Contact key vendors directly, explain the payment process, and offer support for setup. Many suppliers simply need guidance, not a hard sell.

For legacy ERP issues, prioritize platforms with pre-built connectors or open APIs. If your ERP is older, a middleware layer can bridge the gap without requiring a full system replacement. Strong expense management integration is often the deciding factor when choosing between platforms.

“ROI uncertainty is one of the most cited barriers to virtual card adoption. But rebate programs, where your card platform shares a percentage of interchange revenue with you, can meaningfully offset transaction fees and shift the economics in your favor.”

Supplier resistance and unclear ROI remain real challenges, but rebates help offset fees and make the business case easier to close with your CFO. Build a simple ROI model before your first board presentation. Include time saved on reconciliation, reimbursement reduction, and fraud prevention.

A fresh perspective: Why a hybrid approach and supplier enablement fuels real results

Here is something most virtual card guides skip: going fully virtual is not always the right move, at least not immediately. Physical cards still serve a genuine purpose for travel, client entertainment, and any spend category where in-person payment is unavoidable. The real power comes from running hybrid card programs where virtual handles the high-volume, automatable spend and physical covers the rest.

The single biggest lever for improving your virtual card program is not the technology. It is supplier acceptance. If your top 20 vendors cannot receive virtual card payments, your automation rate stays low and the ROI case weakens. Invest time upfront in enabling suppliers before you scale.

Compliance and rebate structure matter too, but they are secondary to adoption. A well-structured pilot in one spend category, say SaaS tools or recurring vendor payments, gives you real data, builds internal credibility, and creates a clear path to C-level buy-in. Start small, prove the model, then expand. That sequence works far better than a big-bang rollout that stalls on supplier or ERP issues.

Business banking built for SME finance teams

For finance teams ready to move beyond spreadsheets and manual reimbursements, Demivolt offers a regulated, digital-first platform built for exactly this challenge.

Demivolt is built for European SMEs that need a fast, compliant, and fully digital banking solution. Dedicated IBAN accounts, SEPA payments, multi-account structures, and role-based access — all in one regulated platform. Onboarding is fast, KYC is handled digitally, and virtual and physical business cards are in the works. Join the waitlist to be first in line when they launch. Explore how the platform can centralize your card issuance, automate reconciliation, and give your finance team real-time visibility into every euro spent.

Frequently asked questions

How long does it take to issue a virtual card for my SME in Europe?

Most fintech platforms enable instant issuance post-KYC, while embedded platform APIs can reduce full program deployment to as little as 28 days versus up to a year with traditional banks.

Are virtual cards accepted everywhere physical cards are?

Virtual cards work well for online payments and AP automation, but some POS and travel purchases still require a physical card, which is why hybrid programs remain relevant.

What compliance requirements do we need to meet for virtual card issuance?

You need to work with licensed EMI or bank partners, complete PSD2-aligned KYC checks, and integrate with a regulated payment processor operating under EU law.

How do virtual cards help reduce fraud and control expenses for SMEs?

Granular controls and instant issuance minimize reimbursement risk and fraud by allowing single-use card numbers, merchant-level restrictions, and real-time transaction alerts that flag unusual activity immediately.