TL;DR:

- IBAN accounts lower cross-border transfer costs by enabling local payment rails like SEPA.

- Proper IBAN management improves payment speed, accuracy, and reconciliation for SMEs.

- Non-IBAN countries require different routing codes and SWIFT, impacting international transfer choices.

Many SMEs assume international transfers are unavoidably slow and expensive. That assumption costs real money. With a properly structured IBAN account, businesses processing regular cross-border payments can save thousands annually on FX margins and transaction fees alone. This guide breaks down exactly what an IBAN account is, how it works for cross-border transactions, and how your SME can manage one effectively. Whether you are expanding into European markets or paying international suppliers, understanding IBAN accounts gives you a real operational edge.

Table of Contents

- What is an IBAN account?

- How IBAN accounts streamline cross-border payments

- Managing IBAN accounts for compliance and multiple currencies

- Alternatives to IBAN accounts: Non-IBAN countries and payment routes

- Our take: What most guides miss about IBAN accounts for SMEs

- Get started with easy business banking

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| IBAN boosts savings | SMEs can save thousands on FX and payment fees by leveraging IBAN accounts. |

| Global payment flexibility | IBAN enables fast, accurate payments within SEPA and across borders with local-like processing. |

| Compliance matters | Proper management of IBAN, especially virtual IBANs, is key to avoiding costly errors and meeting AML regulations. |

| Know alternatives | Not all countries use IBAN—SMEs should understand SWIFT and local routing methods for global payments. |

What is an IBAN account?

Now that you know why IBAN accounts are valuable, it is crucial to understand exactly what sets them apart from standard business accounts.

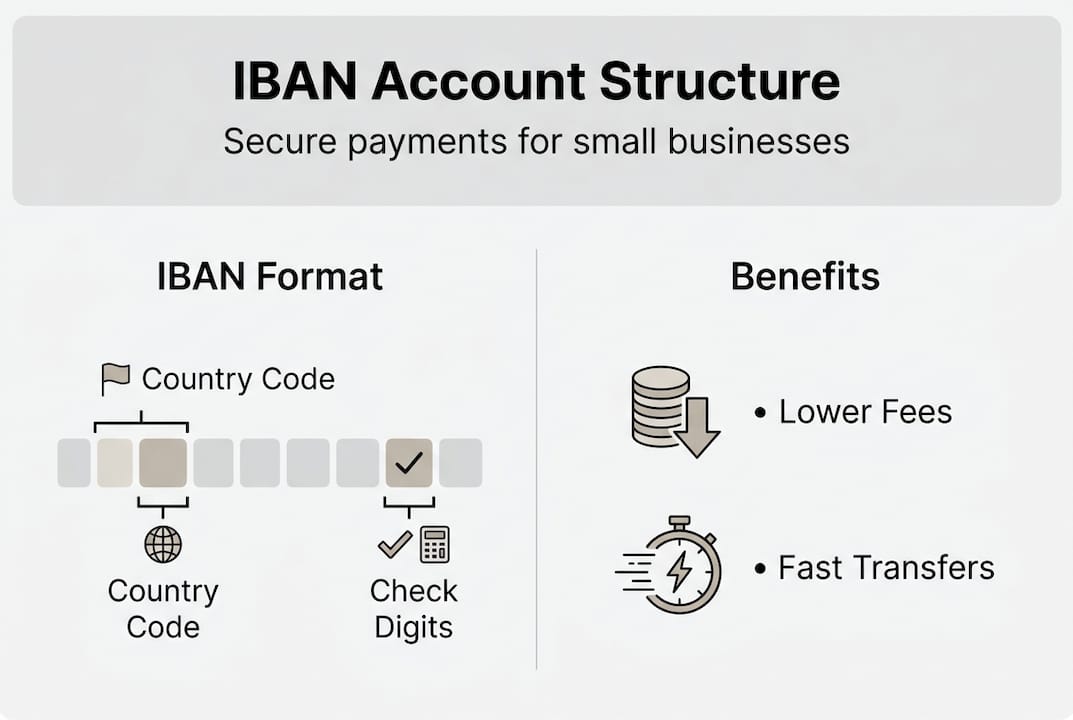

IBAN stands for International Bank Account Number. It is a standardized format used across more than 80 countries to identify bank accounts during international transactions. Think of it as a universal address for your business bank account, one that every participating bank in the world can read and route correctly.

The IBAN standardized structure was designed specifically to eliminate errors in cross-border payments. Before IBAN, banks used different account numbering systems, which caused frequent misroutes, delays, and failed transfers. IBAN brought a common format that automated systems could validate instantly.

Here is what an IBAN looks like and what each part means:

- Country code (2 letters): Identifies the country where the account is held, for example, DE for Germany or FR for France.

- Check digits (2 numbers): Allow automated systems to validate the IBAN before processing, catching typos before they cause failures.

- Basic Bank Account Number (BBAN): Contains the bank code, branch code, and actual account number. Its length and format vary by country.

A German IBAN, for example, is always 22 characters. A UK IBAN is 22 characters. A French IBAN is 27 characters. The format is country-specific but globally recognizable.

How does this differ from a regular business account? A standard domestic account number works fine for local payments, but it lacks the standardized structure that international banking systems require. When you send money abroad using just a local account number, banks fill in the gaps manually, which slows things down and increases errors. An IBAN’s role in international payments is to remove that guesswork entirely.

If you are still comparing your options, reviewing the different types of business bank accounts can help clarify which structure fits your SME’s payment volume and geographic reach. For most SMEs operating across borders, an IBAN account is not optional. It is the infrastructure that makes efficient international trade possible.

How IBAN accounts streamline cross-border payments

Understanding IBAN structure sets the stage for seeing how they transform international payments for SMEs.

The most immediate benefit is cost. Traditional bank wires often carry FX margins of 2% to 4% on top of flat transfer fees. Fintech IBAN solutions bring those margins down dramatically, sometimes to under 0.5%, by enabling local payment rails instead of correspondent banking chains.

Speed is the second major win. Here is a quick comparison of common transfer methods available to SMEs with IBAN accounts:

| Payment Method | Typical Speed | Typical Cost | Best For |

|---|---|---|---|

| SEPA Instant | Seconds | Very low | EU-to-EU urgent payments |

| Standard SEPA | 1 business day | Low | Regular EU supplier payments |

| SWIFT | 1 to 5 business days | Higher | Non-IBAN international payments |

| Virtual IBAN | Instant routing | Low | Reconciliation and multi-payer scenarios |

For SMEs managing supplier payments or customer refunds across Europe, the shift from SWIFT to SEPA Instant alone can cut payment cycles from days to seconds.

Virtual IBANs add another layer of operational efficiency. Instead of sharing one account number with dozens of clients, your SME can assign a unique virtual IBAN to each customer or transaction. All payments route to your master account, but each one is tagged for automatic reconciliation. This is a powerful tool for SME payment efficiency and eliminates hours of manual matching.

Pro Tip: Always validate IBANs before initiating a transfer. Most modern banking platforms include a built-in IBAN validator. Using one costs nothing and prevents the most common cause of payment delays.

There are also mistakes to watch out for. The single biggest operational error SMEs make is IBAN mismatches, entering a character wrong, transposing digits, or copying from an outdated invoice. These errors trigger automatic rejections or, worse, send funds to the wrong account. Building a double-check step into your payment workflow is not optional if you process more than a handful of international transfers per month.

Partnering with the right fintech solutions for cross-border payments gives your SME access to validation tools, real-time payment tracking, and lower fee structures that traditional banks simply do not offer.

Managing IBAN accounts for compliance and multiple currencies

After seeing the cost and speed advantages, SMEs must also be prepared to manage their IBAN accounts with compliance and multi-currency needs in mind.

Here are four practical steps for keeping your IBAN account operations compliant and efficient:

- Establish a clear reconciliation process. Assign unique references or virtual IBANs to each payment source so your finance team can match incoming funds without manual digging.

- Document your AML procedures. Every business using virtual IBANs faces AML risk because payments can be rerouted through intermediary accounts, obscuring the original sender. Have written procedures for verifying payer identity.

- Segregate currencies where possible. If your SME handles EUR, GBP, and USD regularly, consider maintaining separate sub-accounts or wallets per currency to avoid unnecessary conversion costs.

- Run regular compliance audits. At minimum quarterly, review your transaction logs for unusual patterns, dormant accounts, or large unexplained inflows.

Pro Tip: Choose a platform that supports role-based user management. Allowing your accountant view-only access while your CFO handles approvals reduces the risk of unauthorized transactions and strengthens your internal controls.

“Compliance is not a one-time setup. It is an ongoing process that requires the same attention as your payment operations themselves.”

Managing multi-currency accounts adds complexity but also opportunity. Holding funds in the currency they arrive in avoids automatic conversion at unfavorable rates. When you need to convert, timing matters. Platforms that offer rate alerts or forward contracts let you lock in favorable rates ahead of time.

For SMEs new to this, the SME banking compliance framework is a practical starting point. If you are at the stage of setting up your first business IBAN, the process of opening an IBAN account online in Europe has become significantly faster with regulated fintech platforms. And once you scale, managing multiple accounts across currencies and entities requires structured workflows, not just spreadsheets.

Alternatives to IBAN accounts: Non-IBAN countries and payment routes

Beyond Europe, you may encounter markets that do not use IBAN accounts. Here is how to navigate payments in those regions.

Not every major economy uses IBAN. The US, Canada, Australia, China, India, and Japan rely on local routing codes combined with SWIFT for international payments. Understanding their systems is essential if your SME does business in these markets.

| Country | Routing System | Identifier Used | SWIFT Required? |

|---|---|---|---|

| United States | ABA / Fedwire | ABA Routing Number | Yes |

| Canada | EFT | Transit Number + Institution Number | Yes |

| Australia | BSB | BSB Code + Account Number | Yes |

| India | NEFT / IMPS | IFSC Code | Yes |

| Japan | Zengin | Branch Code + Account Number | Yes |

| China | CNAPS | Bank Code | Yes |

SWIFT acts as the bridge when local routing systems cannot connect directly. It is reliable, but it is slower and more expensive than SEPA, typically taking 1 to 5 business days and carrying correspondent bank fees that can stack up.

For SMEs, the key takeaways when paying into non-IBAN countries are:

- Always collect the full set of local routing details, not just the account number.

- Confirm the SWIFT BIC (Bank Identifier Code) for the receiving bank.

- Factor in correspondent bank fees, which can add $10 to $40 per transfer depending on the route.

- Ask your banking provider about national payment alternatives that may offer better routes.

When should your SME use IBAN versus alternatives? Use IBAN whenever possible for European payments. It is faster, cheaper, and more automated. For payments to non-IBAN regions, use SWIFT with full local routing details, and lean on a platform with a transparent SWIFT payment guide to minimize errors and fees.

One underrated risk: SMEs often apply IBAN logic to non-IBAN payments, leaving out critical routing details because they expect the account number to be sufficient. It is not. A missing ABA number or IFSC code will cause a rejection or, in some cases, a misrouted payment that takes weeks to recover.

Our take: What most guides miss about IBAN accounts for SMEs

With a clear view of IBAN and its alternatives, here are lessons SMEs rarely see in mainstream guides.

Most articles about IBAN accounts stop at definitions and fee comparisons. What they skip is the operational reality of running multi-currency, multi-entity payment workflows at scale. Virtual IBANs are genuinely powerful, but SMEs consistently underestimate the reconciliation discipline and AML documentation they require. The tool is not the solution. The process around it is.

Another gap: very few guides acknowledge how much payment infrastructure choices affect your accounting overhead. When your IBAN account is not integrated with your invoicing or ERP system, your finance team spends hours every month doing manual matching. The deeper understanding of IBAN’s role goes beyond cost savings into workflow architecture.

Our honest advice: do not choose a banking platform based on fee tables alone. Look at how it handles reconciliation, what compliance tools it gives you, and whether it grows with your transaction volume. The cheapest option at 10 monthly payments can become the most expensive at 500.

Get started with easy business banking

Ready to move forward? Here is how Demivolt can help your SME manage IBAN accounts easily.

Demivolt is built for exactly this challenge. As a regulated European fintech platform, it gives SMEs dedicated IBAN accounts, SEPA and SWIFT payment capabilities, and multi-account structures designed for cross-border operations.

With Demivolt, you get built-in compliance tools, role-based access controls, and real-time payment tracking, all in one place. Onboarding is fast, transparent, and fully digital. If your SME is ready to stop overpaying on international transfers and start managing payments with confidence, business banking for SMEs at Demivolt is the logical next step. Open your IBAN account and take control of your cross-border payment operations today.

Frequently asked questions

How does an IBAN account reduce international payment costs for SMEs?

IBAN accounts reduce FX margins and transaction fees by enabling local payment rails like SEPA instead of costly correspondent banking chains used in traditional wire transfers.

What happens if there is an IBAN mismatch in cross-border payments?

IBAN mismatches trigger automatic rejections or delays. 34% of SEPA payments are affected by this issue, making accurate account details critical before initiating any transfer.

Can SMEs in the US, Canada, or Australia use IBAN accounts for international payments?

No. These countries rely on local routing codes such as ABA or BSB numbers combined with SWIFT for processing international transfers.

Are virtual IBANs safe for SMEs to use?

Virtual IBANs support efficient reconciliation but carry increased AML risks because payments route through intermediary accounts, requiring documented compliance procedures to use them safely.

Recommended

- Demivolt | Blog – IBAN’s role in seamless international payments: 2026

- Demivolt | Blog – Business banking for SMEs: services, compliance & cross-border

- Demivolt | Blog – SWIFT payment guide: faster transfers for European SMEs

- Demivolt | Blog – International payments for SMEs: efficiency, compliance, growth