IBAN’s role in seamless international payments: 2026

TL;DR:

- Most international payment failures result from simple IBAN errors, not fraud or system issues.

- IBAN is a standardized account identifier that improves cross-border payment accuracy and speed.

- Virtual IBANs offer SMEs multi-currency management, rapid setup, and scalable payment solutions.

A staggering 72% of international payment failures stem from basic formatting or account number errors, not complex fraud or system outages. For finance and operations managers at SMEs running cross-border trade, that number should stop you cold. Every failed payment means delayed supplier relationships, frozen cash flow, and potential compliance flags. IBAN, the International Bank Account Number, was built specifically to eliminate these errors by standardizing how bank accounts are identified globally. This guide breaks down how IBAN works, why virtual IBANs are reshaping SME finance, and what practical steps you can take right now to reduce payment friction and stay compliant.

Table of Contents

- What is IBAN and how does it work?

- IBAN in cross-border payments: A gamechanger for SMEs

- Virtual IBANs: Scalability and multi-currency advantages

- Pitfalls, compliance, and risk: Getting IBANs right

- A smarter IBAN strategy for tomorrow’s cross-border trade

- Unlock seamless global payments with Demivolt

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Reduce payment errors | Validating IBANs prevents costly mistakes and speeds up cross-border transactions. |

| Empower SME growth | Virtual IBANs help SMEs manage multiple currencies and scale global operations efficiently. |

| Stay compliant | Proper IBAN use and validation are now essential for meeting new international compliance rules. |

| Know the limits | Pair IBAN use with fraud controls and awareness of non-IBAN countries for real risk reduction. |

What is IBAN and how does it work?

IBAN stands for International Bank Account Number. It is a globally recognized, standardized format for identifying a bank account across borders. Think of it as a postal address for your money: without the right format, the payment simply cannot find its destination.

Every IBAN follows a fixed structure:

- Country code (2 letters): Identifies the country where the account is held, e.g., DE for Germany, FR for France.

- Check digits (2 numbers): Calculated using the MOD 97-10 algorithm to catch transcription errors before a payment is sent.

- Bank code: Identifies the specific financial institution.

- Account number: The unique identifier for the individual account.

Here is a quick breakdown of how IBAN lengths vary by country:

| Country | IBAN length | Example format |

|---|---|---|

| Germany | 22 characters | DE89 3704 0044 0532 0130 00 |

| France | 27 characters | FR76 3000 6000 0112 3456 7890 189 |

| Netherlands | 18 characters | NL91 ABNA 0417 1643 00 |

| Spain | 24 characters | ES91 2100 0418 4502 0005 1332 |

The MOD 97-10 algorithm is the backbone of IBAN’s reliability. When you enter an IBAN, the system rearranges the digits and divides them by 97. If the remainder is not 1, the IBAN is invalid. This catches the vast majority of typos before any money moves. As Tax1099 explains, IBAN facilitates accurate routing of payments through built-in checks, reducing errors at the source.

IBAN does not work alone. For international wires, it pairs with a SWIFT/BIC code (Bank Identifier Code), which identifies the bank itself rather than the account. IBAN tells the network where the money goes; BIC tells it which bank to route through. Both are required for most cross-border SWIFT transfers.

For SMEs, understanding this distinction matters. Sending a payment with the IBAN but the wrong BIC can still cause delays or rejections, even if the IBAN passes its checksum. Always verify both identifiers before initiating a payment. You can find guidance on IBAN validation essentials to build this into your standard payment workflow.

Pro Tip: Run every new IBAN through a validation tool before adding it to your payment system. Most banking platforms and payment APIs offer free IBAN validation. This single step eliminates the majority of avoidable payment failures.

IBAN in cross-border payments: A gamechanger for SMEs

For SMEs operating within Europe, IBAN’s biggest practical benefit is its integration with SEPA, the Single Euro Payments Area. SEPA covers 36 to 41 countries, enabling instant, low-cost euro transfers that settle in seconds rather than days. For a business paying a supplier in Poland or receiving a client payment from Spain, this is a genuine operational advantage.

Here is a direct comparison of IBAN versus non-IBAN payment environments:

| Feature | IBAN countries | Non-IBAN countries (US, Canada, etc.) |

|---|---|---|

| Standardized format | Yes | No (routing + account number used) |

| Error validation built in | Yes | Limited |

| SEPA instant payments | Available | Not applicable |

| Settlement speed | Seconds to hours | 1 to 5 business days |

| Transaction cost | Low to zero (SEPA) | Higher correspondent fees |

“SEPA and IBAN together have fundamentally changed what it means to move money across European borders. For SMEs, this is the closest thing to a domestic payment experience for cross-border trade.”

When trading with businesses in the US, Canada, Australia, or Japan, you will not receive an IBAN from your counterpart. These countries use domestic routing systems instead. In those cases, your payment will rely on SWIFT with correspondent banking, which is slower and more expensive. Managing currency risk strategies becomes especially important here, since longer settlement windows increase your exposure to exchange rate movement.

Here are the steps every SME should follow for correct IBAN usage in cross-border payments:

- Collect the full IBAN from your counterpart in writing, not verbally.

- Validate the IBAN using a dedicated tool or your banking platform before entering it into your system.

- Confirm the BIC/SWIFT code matches the bank associated with the IBAN.

- Check the currency your counterpart’s account holds to avoid unnecessary conversion fees.

- Store validated IBANs in a centralized, access-controlled system to prevent re-entry errors.

For SMEs looking to scale their cross-border operations, exploring virtual IBAN solutions for SMEs adds another layer of efficiency on top of these fundamentals.

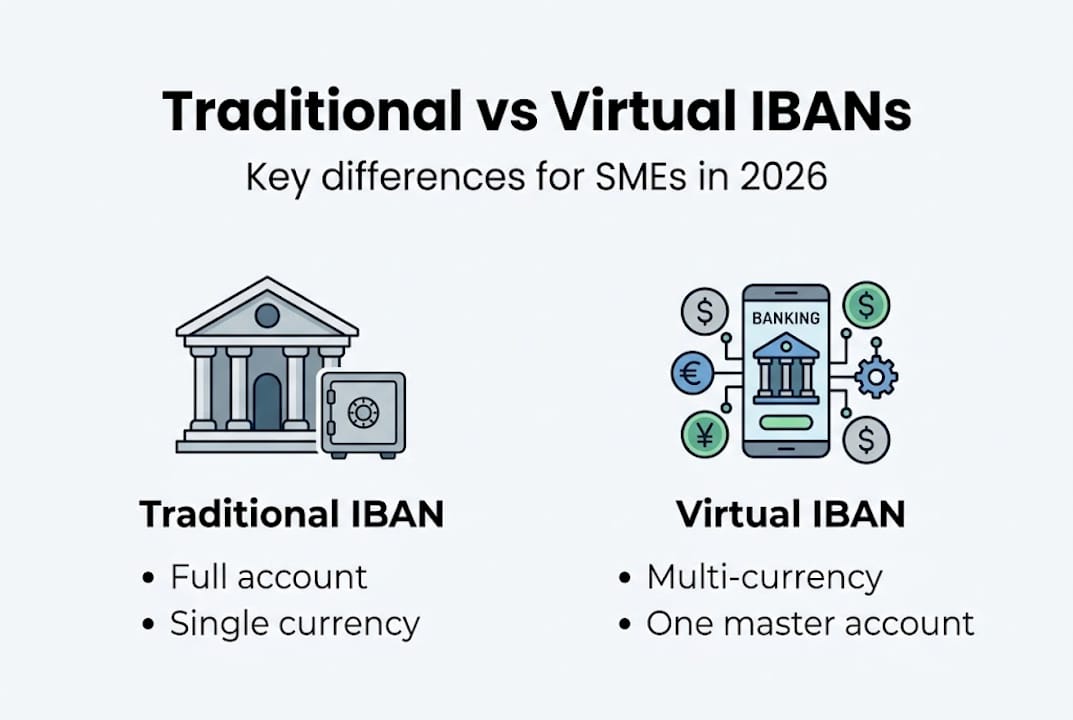

Virtual IBANs: Scalability and multi-currency advantages

A virtual IBAN (vIBAN) looks and functions like a standard IBAN from the outside. The difference is what happens behind the scenes. Instead of being tied to a single physical bank account, a virtual IBAN routes incoming payments to a master account. This lets you assign unique IBANs to different clients, currencies, or business units without opening separate bank accounts for each.

For a growing SME managing payments from ten different countries, this is transformative. Here is what virtual IBANs make possible:

- Multi-currency collection: Assign a unique IBAN per currency so client payments arrive pre-sorted, without manual intervention.

- Automated reconciliation: Each virtual IBAN acts as a tag. Your finance team can match incoming payments to invoices automatically, cutting reconciliation time dramatically.

- Instant setup: No branch visits, no lengthy onboarding per account. Virtual IBANs can be provisioned in minutes through a regulated platform.

- Scalability: Virtual IBANs allow up to 1,000 sub-accounts and instant setup, making them ideal for SMEs scaling globally without adding administrative overhead.

- Cost control: Fewer physical accounts mean lower maintenance fees and simpler month-end reporting.

The contrast with traditional IBANs is stark. A traditional IBAN requires a full bank account, often with minimum balance requirements, compliance checks per account, and manual setup. Virtual IBANs strip that friction away.

When should you choose virtual over traditional? If your business collects payments from multiple clients in different currencies, processes high transaction volumes, or needs to separate payment flows by project or entity, virtual IBANs are the better fit. For a single-currency, low-volume operation, a traditional IBAN may be sufficient. Understanding modern business banking trends helps you make this call with confidence.

For SMEs with more complex treasury needs, pairing virtual IBANs with enterprise currency management tools creates a genuinely powerful setup for virtual IBANs for cross-border operations.

Pro Tip: Only use virtual IBANs issued by regulated Electronic Money Institutions (EMIs) or licensed banks. Unregulated providers may not segregate your funds, creating serious risk if the provider fails.

Pitfalls, compliance, and risk: Getting IBANs right

Knowing how IBAN works is one thing. Avoiding the mistakes that cost businesses real money is another. Up to 8% of international payments are delayed or rejected due to IBAN entry errors. That is not a rounding error. For a business processing 500 international payments a month, that is 40 failed transactions eating into your operations team’s time and your supplier relationships.

Here is a numbered checklist for pre-validating IBANs before every payment run:

- Confirm the IBAN length matches the expected length for that country.

- Run the IBAN through a MOD 97-10 validator.

- Cross-check the bank code within the IBAN against the BIC provided.

- Verify the account holder name matches your records.

- Check whether the account is still active, especially for suppliers you have not paid in over six months.

“The biggest compliance risk for SMEs is not fraud. It is the assumption that a valid checksum means a safe payment. It does not.”

This matters because of Verification of Payee (VoP), a regulatory requirement rolling out across the EU. VoP requires banks to confirm that the account holder’s name matches the IBAN before a payment is processed. This catches a category of fraud that IBAN checksums cannot: authorized push payment (APP) fraud, where you are tricked into sending money to the right IBAN format but the wrong person.

The checksum tells you the IBAN format is correct. It does not tell you the account belongs to who you think it does. Pairing IBAN validation with name matching, geolocation checks, and transaction monitoring is the standard you should be building toward. Explore fintech compliance strategies to understand how modern platforms are automating these controls.

Common pitfalls to watch for:

- Copying IBANs from email signatures where formatting may have broken across lines.

- Storing IBANs in spreadsheets without version control, leading to outdated details being reused.

- Assuming a payment that cleared once will always clear to the same IBAN, even if the supplier changed banks.

Building a process for reducing IBAN payment failures into your payment operations is not optional at scale. It is the difference between a finance team that runs smoothly and one that spends hours chasing failed transactions.

A smarter IBAN strategy for tomorrow’s cross-border trade

Here is the uncomfortable truth most articles skip: using IBAN is not a strategy. It is a baseline. The SMEs winning at cross-border trade in 2026 are not just using IBANs. They are layering validation APIs, virtual account structures, and real-time compliance monitoring on top of them.

Only 35 to 55% of global cross-border payments settle within one hour despite widespread IBAN adoption. The G20 target is 75%. That gap exists because IBAN solves the identification problem, not the infrastructure problem. Correspondent banking delays, currency conversion friction, and inconsistent compliance standards across jurisdictions all still apply.

What this means for you: treat IBAN as the foundation, not the finish line. The businesses that will handle cross-border payment efficiency best are those building payment stacks that combine validated IBANs, virtual account structures, and proactive compliance updates as standards evolve toward the next generation of payment rails. Innovation consistently outpaces simple adoption. The question is whether your payment infrastructure is keeping up.

Unlock seamless global payments with Demivolt

If this guide has shown you anything, it is that getting IBANs right requires more than good intentions. It requires the right infrastructure.

Demivolt business banking gives SMEs dedicated IBAN accounts, virtual IBAN capabilities, and SEPA payment management in one regulated platform, with SWIFT transfers launching soon. Whether you need multi-currency collection, automated reconciliation, or role-based access for your finance team, Demivolt is built for exactly the kind of cross-border complexity you are managing. Onboarding is fast, fees are transparent, and your funds are held in segregated accounts under EU regulatory standards. Explore SME banking and compliance to see how Demivolt fits your operation.

Frequently asked questions

Is IBAN used worldwide or only in Europe?

IBAN is used in over 70 countries, primarily across Europe and parts of the Middle East, but major economies including the US, Canada, Australia, China, and Japan do not use the IBAN system.

How do SMEs benefit from virtual IBANs?

Virtual IBANs route to a master account for multi-currency holding and rapid setup, enabling SMEs to manage multiple currencies, automate reconciliation, and create sub-accounts instantly for faster global trade.

What happens if an IBAN is entered incorrectly?

Up to 8% of international payments are delayed or rejected due to IBAN entry errors, making pre-validation a critical step before processing any cross-border transaction.

Can IBANs help prevent fraud?

IBAN checksum validation catches formatting mistakes but does not prevent fraud on its own; combining it with name matching under VoP requirements and additional transaction controls is necessary for real security.

Recommended

- Demivolt | News – UK banks plan national payments alternative to Visa and Mastercard, citing geopolitical risks

- Demivolt | Blog

- Demivolt | Business Banking Made Clear

- Demivolt | News – Visa Intelligent Authorization modernises payment processing for banks and financial institutions, unlocking ‘era of innovation’

- International business banking guide for US expats in Europe

- Moldova Joins SEPA in 2025: What It Means for Founders, Exporters, and Remote Businesses » Incorpore