TL;DR:

- Industry payment terms like “Net60” significantly influence cash flow and compliance risks in B2B transactions. Understanding ACH codes such as CCD versus PPD is crucial to avoid legal exposure and ensure proper transaction classification. Mastering industry terminology helps streamline operations, reduce disputes, and leverage emerging digital and card-based payment strategies effectively.

If you’ve ever signed off on a contract without fully understanding what “Net60” obligates you to, or processed an ACH payment without knowing whether it needed a CCD or PPD code, you already know that industry terms in b2b payments are not just administrative trivia. They directly affect your cash flow, your compliance exposure, and your relationships with vendors and clients. The terminology has also grown more complex in recent years as digital payment rails, new ACH regulations, and evolving card strategies have added layers that professionals can no longer afford to ignore.

Table of Contents

- Key takeaways

- Core industry terms in B2B payments

- ACH compliance: CCD vs PPD distinctions

- Modern payment trends shaping B2B terminology

- Applying payment term knowledge to real operations

- My take on why terminology mastery is no longer optional

- How Demivolt supports clearer B2B payment operations

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Net terms still dominate | Net30 leads B2B invoicing at 55–65% of invoices, making it the default term most finance teams will encounter. |

| CCD vs PPD is a compliance issue | Using the wrong ACH code exposes your business to unauthorized transaction disputes and regulatory risk. |

| Term graduation reduces bad debt | Starting new clients on shorter terms and extending credit after a payment track record protects seller revenue. |

| Digital payments are majority volume | Nearly half of B2B payments in North America are now initiated digitally, but paper checks still count for 30–35% by transaction volume. |

| Cards are no longer just a payment rail | Commercial cards now bundle identity verification and fraud monitoring, making them a strategic financial tool. |

Core industry terms in B2B payments

Understanding B2B payment terminology begins with the terms printed on most invoices. These are not interchangeable phrases. Each carries legal, financial, and operational weight.

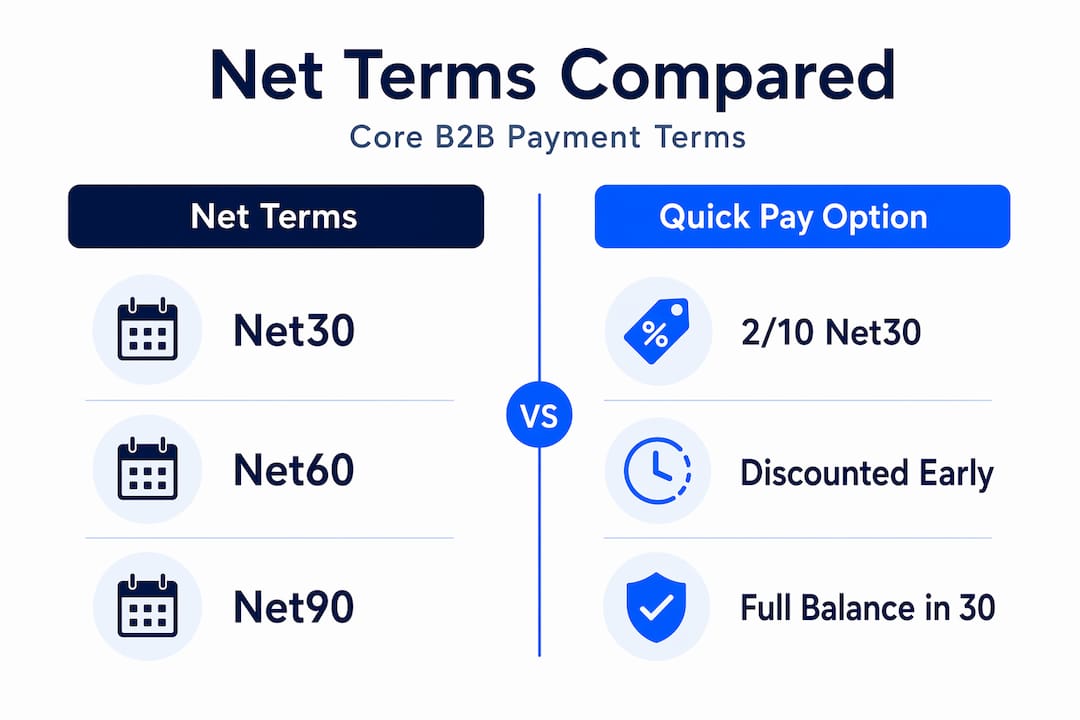

Net terms: Net30, Net60, and Net90

Net terms define how many calendar days a buyer has to pay after receiving an invoice. Net30 remains the dominant term in North America, appearing on 55–65% of B2B invoices. Net60 follows at 15–25%, while Net90 remains rare outside specialized industries like manufacturing or government contracting.

A related phrase you’ll encounter is “2/10 Net30,” which means the buyer receives a 2% discount if they pay within 10 days, but the full amount is still due within 30. This is called dynamic discounting, and it gives sellers a tool to accelerate cash collection without permanently altering their pricing structure.

Common payment methods and what they mean

The payment method shapes the risk profile, cost, and speed of any transaction. Here is a reference breakdown:

| Term | Definition | Typical Use Case |

|---|---|---|

| ACH (Automated Clearing House) | Electronic bank-to-bank transfer through the ACH network | Recurring B2B payments, payroll, vendor settlements |

| Wire transfer | Direct, immediate bank transfer, often used for large sums | High-value or international transactions |

| CCD (Corporate Credit or Debit) | ACH transaction code for business-to-business transfers | Vendor payments, B2B collections |

| PPD (Prearranged Payment and Deposit) | ACH code for consumer account transactions | Consumer direct debit, personal payroll |

| Dynamic discounting | Early payment in exchange for a negotiated discount | Seller cash flow acceleration |

| Term graduation | Progressive extension of credit terms based on payment history | New client onboarding risk management |

Pro Tip: “Net” in payment terms refers to the full invoice amount, with no deductions. If a term says “Net30 minus returns,” that is a customized clause, not a standard definition.

One phrase that trips up many finance teams is “term graduation.” This is the practice of starting a new client on tighter terms, such as cash in advance or Net15, and then progressing them to longer terms only after they have built a track record of on-time payments. It is a credit management strategy disguised as a payment term.

ACH compliance: CCD vs PPD distinctions

This is where common B2B payment phrases stop being academic and start costing real money. The ACH network processes trillions of dollars in transactions, and two of its most consequential classification codes are CCD and PPD.

CCD codes apply strictly to business-to-business ACH transactions, while PPD codes are reserved for consumer accounts. The distinction matters far beyond taxonomy.

Why the wrong code creates legal exposure

CCD transactions are not covered by Regulation E, the federal consumer financial protection regulation. That means if an unauthorized B2B ACH transaction goes through under a CCD code, the dispute window is only two days for returning it, compared to the 60-day window consumers enjoy under PPD rules. Finance teams that process business payments through PPD codes, sometimes because the setup is simpler, are operating outside the rules and creating misclassification risk.

| Feature | CCD | PPD |

|---|---|---|

| Applicable party | Business accounts only | Consumer accounts only |

| Regulation E coverage | No | Yes |

| Dispute return window | 2 business days | Up to 60 days |

| Addenda records | Supported (for remittance data) | Limited |

| Typical use | Vendor payments, B2B collections | Personal payroll, consumer billing |

| Authorization type | Written business authorization | Written consumer authorization |

Account validation and fraud prevention

Another piece of B2B payment industry jargon that carries real compliance weight is “prenote” and “account validation.” NACHA, the governing body of the ACH network, requires originators to validate bank accounts before the first debit. Many businesses skip this step when onboarding new vendors or clients, treating it as a formality. It is not. It is the primary defense against fraudulent account information and misdirected payments.

Pro Tip: Build account validation into your vendor onboarding checklist as a mandatory step, not an optional one. The 30 minutes it takes upfront can prevent weeks of payment recovery if a fraudulent account number gets into your system.

A third code worth knowing in this category is same-day ACH. Same-day ACH enables faster processing of urgent B2B transactions, including payroll corrections and last-minute settlements. It operates within existing ACH infrastructure but uses dedicated processing windows that clear within the business day.

Modern payment trends shaping B2B terminology

The terminology used in B2B payments does not exist in a vacuum. It shifts as the payment methods themselves evolve.

Approximately 45–50% of B2B payments in North America are now initiated digitally. Paper checks still account for 30–35% of transactions by count, though they represent less than 15% of total payment value. That gap between count and value tells you something important: businesses are still writing checks for smaller, less critical transactions while moving larger payments to digital rails. Understanding this pattern changes how you should structure your own payment acceptance strategy.

“Payment acceptance is transitioning from a back-office task to a frontline competitive advantage through smarter payment routing and flexible term adoption.” Source

How commercial cards changed meaning

The phrase “accepting cards” used to mean paying interchange fees in exchange for convenience. That framing is now outdated. Commercial card networks have evolved into what analysts are calling “enterprise identity infrastructure.” This means the card transaction now bundles KYB (Know Your Business) verification, KYC (Know Your Customer) checks, fraud monitoring, and a full audit trail, not just a payment authorization.

For CFOs and finance directors, this reframes the cost-benefit calculation entirely. You are not just paying interchange to accept a card. You are buying identity verification and fraud coverage as part of the transaction fee.

Offering card payment options alongside traditional invoicing can increase on-time payments by 15–25%, particularly for transactions under $10,000. That is a meaningful cash flow improvement that most finance teams have not yet built into their receivables strategy.

Pro Tip: When evaluating payment term strategy for smaller B2B clients, consider offering card payment as the default acceptance method. The faster collection often outweighs the interchange cost.

Applying payment term knowledge to real operations

Knowing the definitions is half the work. The other half is knowing how to apply them.

Treating all customers with identical payment terms is a strategic mistake that high-performing sellers consistently avoid. The practical alternative is term segmentation: categorizing your client base by payment history, transaction volume, and credit risk, then assigning terms accordingly.

Here is a structured process for integrating terminology awareness into your payment workflows:

- Audit your current invoice terms. Identify what percentage of your outstanding receivables sit under Net30, Net60, and Net90. If more than 20% of your receivables are under Net60 or longer, examine whether those terms are actually justified by client risk profiles.

- Classify your ACH transactions correctly. Review every vendor and client receiving ACH payments. Business accounts must be coded CCD. Consumer accounts must be coded PPD. Confirm your payment processor has the correct authorization agreements on file.

- Validate bank accounts before first debit. Run a prenote or use a real-time account validation service for any new banking relationship before initiating an ACH pull.

- Apply term graduation to new clients. Start new accounts on Net15 or prepayment terms. Build a clear internal policy for when and how they earn longer terms, based on payment history rather than relationship pressure.

- Integrate card acceptance for small-ticket B2B transactions. Set a threshold, such as invoices under $5,000, where you actively promote card payment. Use the interchange cost as a receivables acceleration expense rather than treating it as pure overhead.

For teams managing cross-border payments, understanding how digital payment infrastructure operates across SEPA and SWIFT rails adds another terminology layer, including terms like “correspondent banking,” “SWIFT GPI,” and “credit push” vs. “debit pull” transactions.

Pro Tip: Automate your payment term policy wherever possible. Manual term assignment at the invoice level creates inconsistency. A rules-based system tied to client credit scores produces far better cash flow outcomes than individual judgment calls.

My take on why terminology mastery is no longer optional

I’ve watched finance teams lose significant money not because they made bad strategic decisions, but because they used the wrong vocabulary in a vendor contract or processed a batch of ACH transactions under the wrong code. The penalty is never announced in advance. It shows up weeks later as a dispute, a delayed remittance, or a compliance audit finding.

What I’ve learned is that the professionals who consistently avoid these problems treat payment terminology as a living reference, not a one-time onboarding topic. The terminology is genuinely changing. Terms like “dynamic discounting” and “term graduation” were barely discussed five years ago. Today, differentiating terms based on client risk is standard practice among high-performing finance teams.

My honest advice: if your team cannot accurately define CCD, explain dynamic discounting, or describe the term graduation process without looking it up, that is a gap worth closing before it costs you. The terms are not complicated once explained clearly. What is complicated is unraveling a payment dispute or explaining a compliance violation that stems from not knowing them.

The teams I’ve seen handle payments most confidently are the ones who build term literacy into their onboarding, their contracts, and their collections workflows. They treat it as infrastructure, not vocabulary.

— dd

How Demivolt supports clearer B2B payment operations

Managing B2B payments gets significantly easier when your banking infrastructure is built for it. Demivolt offers a regulated European fintech platform where businesses can open dedicated IBAN accounts, manage SEPA and SWIFT payments, and maintain full visibility into inbound and outbound transactions.

If your team is working to tighten compliance around payment term management, account validation, and cross-border operations, Demivolt’s business banking platform provides the infrastructure to support it. Multi-account structures, role-based user access, and segregated client funds make it practical to apply the term segmentation and ACH compliance practices outlined in this article. You can also explore Demivolt’s guidance on automating business payments to reduce manual errors and accelerate collections.

FAQ

What are the most common B2B payment terms?

Net30, Net60, and Net90 are the most widely used B2B payment terms. Net30 appears on 55–65% of B2B invoices in North America, making it the default across most industries.

What is the difference between CCD and PPD in ACH payments?

CCD (Corporate Credit or Debit) is used exclusively for business-to-business ACH transactions, while PPD (Prearranged Payment and Deposit) applies to consumer account transfers. Using the wrong code can create compliance violations and shorten your dispute window from 60 days to just two.

What does term graduation mean in B2B payments?

Term graduation is the practice of starting new clients on shorter payment terms, such as Net15 or prepayment, then extending longer terms after they demonstrate a consistent payment history. It is a risk management approach designed to reduce bad debt exposure while building client trust.

Why do commercial cards matter beyond just accepting payment?

Commercial cards now function as enterprise identity infrastructure, bundling KYB/KYC verification, fraud monitoring, and audit records into each transaction. They also increase on-time payments by 15–25% for smaller B2B invoices, making them a receivables tool, not just a payment option.

What is dynamic discounting in B2B payments?

Dynamic discounting is an arrangement where a buyer pays an invoice before its due date in exchange for a negotiated discount from the seller. It accelerates the seller’s cash flow without permanently reducing prices.