TL;DR:

- International payments are vital for SME growth, enabling supply chain, payroll, and market expansion.

- Fintech platforms offer faster, cheaper, and more transparent cross-border transactions compared to traditional banks.

- Compliance and regulatory complexity require SMEs to adopt automated, real-time solutions for efficient international payments.

International payments are often dismissed as back-office paperwork, but that framing costs SMEs real money. The truth is that how you move money across borders directly shapes your ability to pay suppliers on time, win new customers, and scale into new markets. Cross-border payments enable SMEs to manage global payroll, collect from international clients, and build supply chains that span continents. This article walks you through why international payments matter, how to choose the right platform, what compliance traps to avoid, and how to turn your payment infrastructure into a genuine competitive advantage.

Table of Contents

- The role of international payments in SME growth

- Comparing traditional banks and fintech solutions

- Cost, speed, and cash flow: The SME impact

- Compliance, risk, and regulatory complexity

- Our take: The real edge—speed, transparency, and compliance mastery

- Unlock smarter international payments with Demivolt

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Unlock new markets | International payments let SMEs access customers, suppliers, and talent worldwide. |

| Cut costs and speed up cash flow | Fintech payment solutions can reduce fees and settlement times by up to 80% compared to banks. |

| Stay compliant and avoid disruptions | Smart compliance tools minimize delays and reduce risks for cross-border payments. |

| Choose the right platform | SMEs should compare banks and fintechs to optimize speed, cost, and transparency. |

| Turn payments into a strategic advantage | Efficient, transparent international payments give SMEs a competitive edge. |

The role of international payments in SME growth

Most SME owners think about international payments only when something goes wrong: a supplier is waiting, a payroll run is late, or a customer can’t complete checkout in their currency. That reactive mindset is expensive. The smarter approach is to treat cross-border payments as a core business function, not an afterthought.

The numbers back this up. The global cross-border payments market is projected to reach $550 billion by 2033, with SMEs growing at 8.5% annually. B2B payment volumes alone are expected to exceed $35 trillion by 2028. These are not enterprise-only figures. SMEs are driving a significant share of that volume, and the ones who optimize their payment infrastructure early are capturing disproportionate market share.

Here is what international payments actually enable for a growing SME:

- Supply chain reliability: Paying overseas suppliers on time builds trust and often unlocks better pricing or priority fulfillment.

- Global payroll: Hiring contractors or employees in other countries requires reliable, low-cost currency conversion.

- Customer acquisition: Accepting payments in local currencies removes friction and increases conversion rates in new markets.

- Revenue diversification: Multiple income streams in different currencies reduce dependency on any single market.

Despite this, SMEs enabling cross-border trade still face significant barriers. A striking 78% of SMEs rely on traditional banks for international transactions, and more than half report unfair pricing as a top complaint. Delays, opaque fees, and poor exchange rates quietly erode margins on every transaction.

“International payments are not just a cost center. For SMEs operating across borders, they are the connective tissue of the entire business model.”

Understanding SWIFT payments for SMEs is a good starting point, but the landscape has shifted significantly. Modern payment rails and fintech platforms now offer SMEs options that simply did not exist five years ago. Staying informed about global commerce trends is no longer optional for businesses with cross-border ambitions.

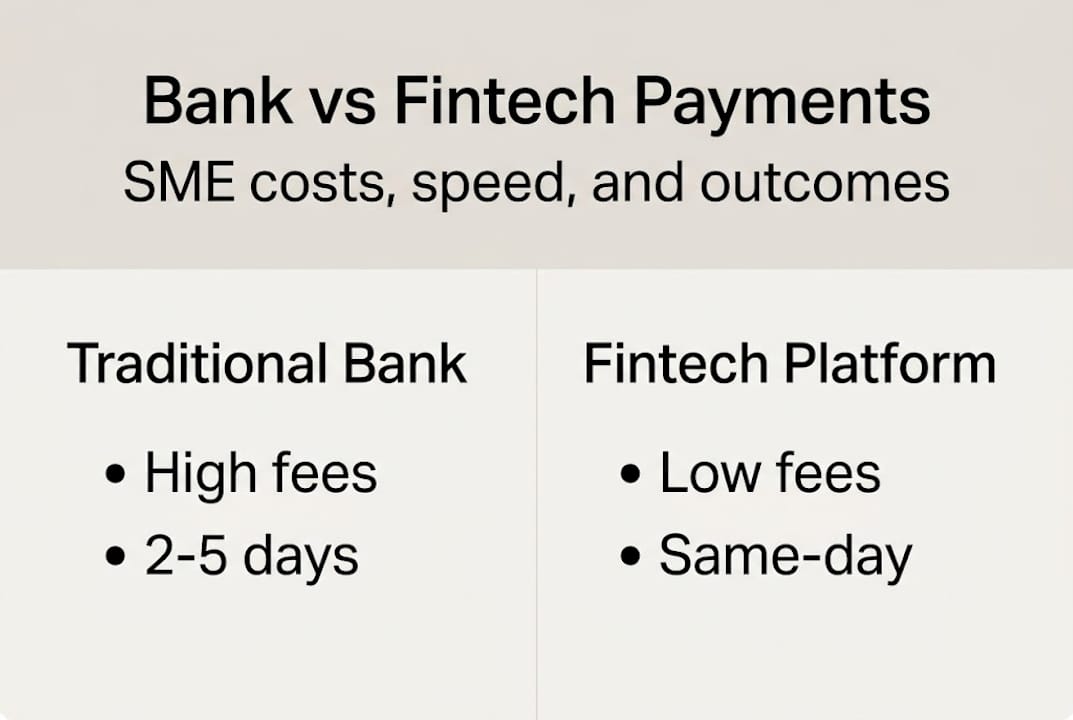

Comparing traditional banks and fintech solutions

Choosing the right payment platform is one of the highest-leverage decisions an SME can make. The difference between a bank wire and a fintech transfer is not just a few dollars in fees. It is settlement time, cash flow predictability, and the ability to move fast when opportunities arise.

Traditional banks route international payments through the SWIFT network, which relies on a chain of intermediary banks. Each intermediary adds its own fee. Bank-based SWIFT transfers typically cost $20 to $50 to send, plus $10 to $20 per intermediary, with FX markups of 4 to 6% and settlement times of 2 to 5 business days. For a business sending $50,000 to a supplier, that markup alone can cost $2,000 to $3,000 per transaction.

Fintech platforms work differently. Multi-currency accounts and fintech rails reduce FX markups to 0.4 to 1%, charge minimal flat fees, and often settle same-day using local payment networks. Real-time tracking means you know exactly where your money is at every step.

| Feature | Traditional bank | Fintech platform |

|---|---|---|

| FX markup | 4 to 6% | 0.4 to 1% |

| Sending fee | $20 to $50 | $2 to $10 |

| Settlement time | 2 to 5 days | Same-day to 2 days |

| Real-time tracking | Rarely | Standard |

| Multi-currency accounts | Limited | Common |

Here is a practical framework for deciding which to use:

- Routine supplier payments: Use fintech for speed and cost savings.

- Large or unusual transactions: Banks may offer more familiarity and support for complex deals.

- Payroll in multiple currencies: Fintech platforms with multi-currency wallets are far more efficient.

- Compliance-heavy corridors: Check whether your fintech provider is regulated and covers the relevant jurisdictions.

Pro Tip: Before committing to any platform, run a side-by-side cost comparison using a real recent transaction. Plug in the exact amount, currency pair, and destination. The difference is often far larger than expected.

Exploring fintech payment solutions designed for SMEs gives you a clearer picture of what modern infrastructure looks like. The fintech infrastructure advances of the last few years have made enterprise-grade payment tools accessible to businesses of all sizes. For more practical guidance, the business payment tips section covers a wide range of operational scenarios.

Cost, speed, and cash flow: The SME impact

The gap between knowing fintech is cheaper and actually feeling the impact in your business comes down to cash flow. For an SME managing tight margins, a 3-day payment delay is not an inconvenience. It can mean missing payroll, delaying a product launch, or losing a supplier relationship.

78% of SMEs using traditional banks wait 2 to 5 days for funds to reach international suppliers. Fintech platforms cut that to 1 to 2 days, with many transactions settling in real time. That speed difference compounds over dozens of transactions per month.

| Scenario | Bank transfer | Fintech transfer |

|---|---|---|

| $10,000 supplier payment | $600 to $1,000 in fees and FX | $40 to $100 |

| Settlement time | 3 to 5 days | Same-day to 1 day |

| Monthly volume ($100K) | $6,000 to $10,000 cost | $400 to $1,000 cost |

The cost reduction potential when switching from banks to fintech for routine international payments is 60 to 80%. That is not a marginal improvement. For an SME processing $1 million in annual cross-border payments, that difference could free up $50,000 to $80,000 per year.

Here are practical steps to optimize your payment workflow:

- Batch payments where possible: Consolidate multiple smaller transfers into one to reduce per-transaction fees.

- Use local payment rails: Platforms that settle via local networks (like SEPA in Europe) are faster and cheaper than SWIFT for regional transfers.

- Set up multi-currency accounts: Hold balances in the currencies you use most to avoid constant conversion costs.

- Automate recurring payments: Scheduled transfers reduce manual errors and ensure suppliers are paid on time.

Pro Tip: Map your top 10 payment corridors by volume and frequency. Negotiate or select platforms specifically optimized for those routes. Generic solutions often underperform on specific currency pairs.

Improving business banking efficiency is not just about cutting costs. It is about building the operational agility to move fast. Staying current on digital payments innovation helps SMEs anticipate shifts before they become disadvantages.

Compliance, risk, and regulatory complexity

Speed and cost savings mean nothing if your payments get blocked. Compliance is the layer most SMEs underestimate until it bites them. And in 2026, the regulatory environment for international payments is more complex than ever.

Every cross-border payment touches at least two regulatory jurisdictions. Multi-jurisdiction compliance overlaps affect approximately 60% of international SME transactions, involving requirements from OFAC sanctions lists, EU regulatory frameworks, AML (anti-money laundering) rules, and KYC (know-your-customer) checks. A single transaction can trigger reviews from multiple authorities simultaneously.

The most common compliance pain points for SMEs include:

- False positives in sanctions screening: Automated systems flag transactions based on name matches or country codes, even when the underlying transaction is fully legitimate. These holds can last days.

- De-risking by banks: Large banks sometimes exit entire payment corridors to reduce their own compliance burden, leaving SMEs without service in specific regions.

- FX volatility during compliance holds: If a payment is delayed 3 days due to a compliance review, the exchange rate you locked in may no longer apply.

- Inconsistent KYC requirements: Different platforms and jurisdictions require different documentation, creating administrative overhead that slows onboarding and payments.

“Compliance is not a one-time checkbox. It is an ongoing operational function that needs to be built into your payment processes from day one.”

The good news is that technology is catching up. AI-driven compliance tools now reduce false positive rates significantly, allowing legitimate transactions to clear faster without sacrificing accuracy. For SMEs dealing with volatile currency pairs, understanding FX risk mitigation strategies is equally important. The goal is to build a payment infrastructure where compliance is automated, not manual.

Our take: The real edge—speed, transparency, and compliance mastery

Here is what most articles on international payments miss: the biggest opportunity cost for SMEs is not the fees themselves. It is the time and mental bandwidth spent managing slow, opaque payment processes. Every hour your finance team spends chasing a delayed wire or reconciling an unexplained deduction is an hour not spent on growth.

The SMEs we see pulling ahead in cross-border markets share three traits. First, they treat payment infrastructure as a strategic asset, not a utility. Second, they choose platforms where compliance is built in, not bolted on after a problem occurs. Third, they use real-time visibility to make faster decisions, whether that means releasing inventory, confirming a supplier order, or closing a deal.

Conventional wisdom says to stick with your bank because it is safe. But safety and speed are not mutually exclusive anymore. The fintech insights available today show that regulated fintech platforms can match or exceed bank-level security while delivering dramatically better operational performance. The SMEs who recognize this early are the ones setting the pace.

Unlock smarter international payments with Demivolt

If the gap between your current payment setup and what is possible feels wide, you are not alone. Most SMEs we work with discover significant inefficiencies only after they start comparing their costs and settlement times against modern benchmarks.

Demivolt is a regulated European fintech platform built specifically for businesses like yours. From dedicated IBAN accounts and SEPA and SWIFT payment management to real-time tracking and compliance-ready infrastructure, everything is designed to give you control and speed. You can explore business banking solutions that match your cross-border payment needs, whether you are optimizing existing workflows or building a new international payment strategy from the ground up.

Frequently asked questions

What are the main benefits of using international payments for SMEs?

International payments give SMEs direct access to global markets, enabling smoother supply chains, faster revenue collection from overseas clients, and the ability to manage global payroll without relying on costly intermediaries.

How do fintech solutions compare to traditional banks for international payments?

Fintech platforms offer FX markups of 0.4 to 1% compared to the 4 to 6% typical of banks, plus same-day settlements and real-time tracking that traditional banks rarely provide.

What compliance challenges should SMEs expect with international payments?

SMEs must navigate sanctions screening and AML/KYC requirements across multiple jurisdictions, and false positives in automated screening can delay or block legitimate transactions without warning.

Why do international payment delays negatively impact SME cash flow?

78% of SMEs using banks wait 2 to 5 days for funds to reach suppliers, which disrupts inventory purchasing, payroll cycles, and supplier trust when timing is critical.

How can SMEs mitigate FX risk when paying or receiving internationally?

Using fintech platforms with multi-currency accounts and low FX markups lets SMEs hold balances in target currencies, reduce conversion frequency, and access more transparent rate structures than traditional banks offer.

Recommended

- Demivolt | Blog – Modern business banking trends: boost efficiency & compliance

- Demivolt | Blog – Business banking for SMEs: services, compliance & cross-border

- Demivolt | News – How fintechs facilitate cross-border payments for SMEs

- Demivolt | Blog – What is SWIFT payment? How it works for SMEs

- swift-gpi - Prominence Bank