Managing international business accounts often means battling slow onboarding, opaque transfer fees, and limited support for EU SEPA, SWIFT, and multi-currency flows. Traditional banks and legacy providers either lock useful tools behind high minimum balances, add hidden currency markups, or delay account setup for weeks. After reading you will be able to compare five modern business banking and payment platforms, each offering dedicated IBANs and multicurrency support, to find the best fit for your company’s cross-border finance needs.

Table of Contents

- Demivolt

- Vialet

- Holvi

- Wise (formerly TransferWise)

- Revolut

- Comparative Analysis of Financial Platforms for SMEs

Demivolt

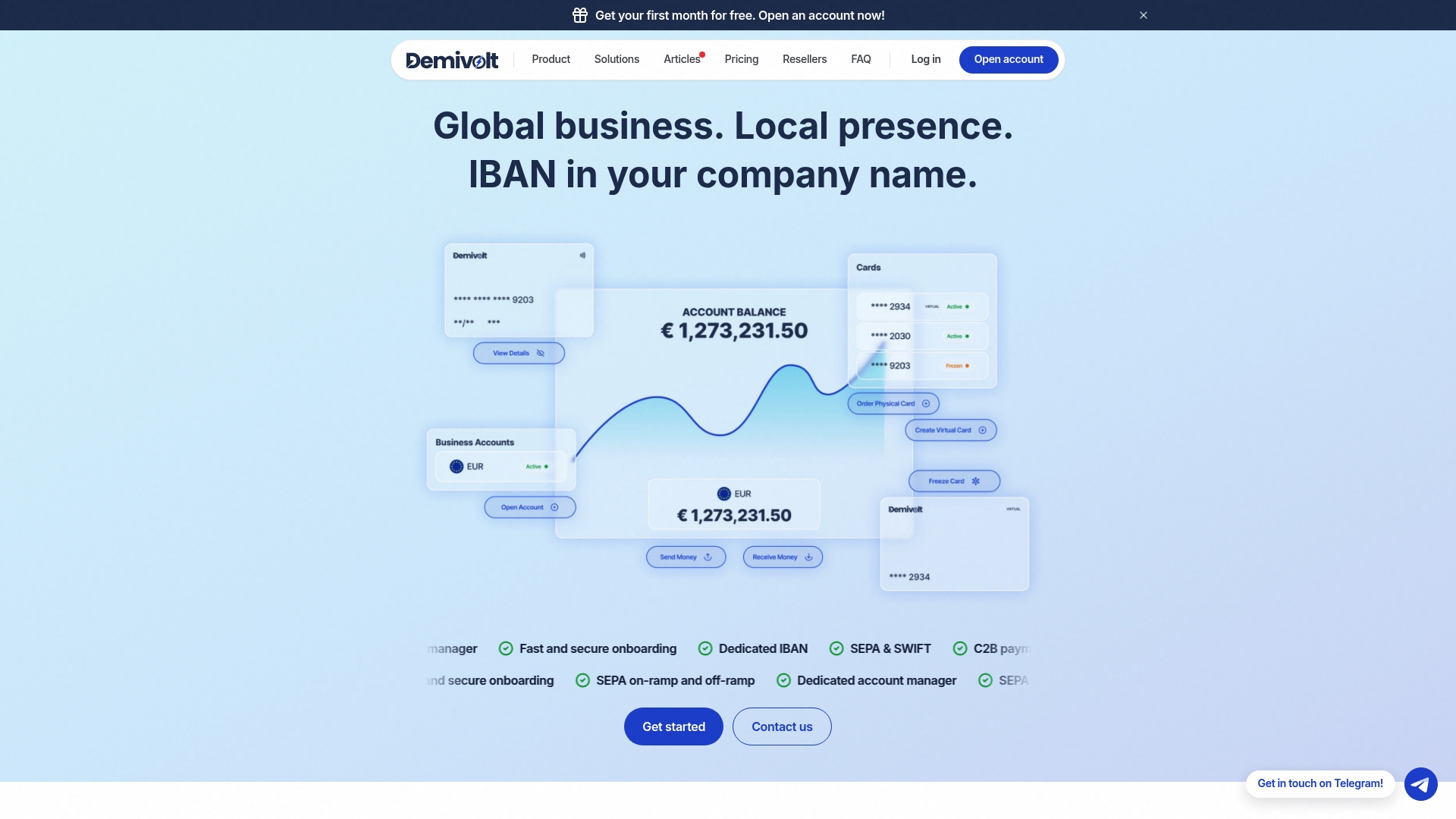

At a Glance

€0.40 outgoing SEPA and a free first month make Demivolt useful for teams that move lots of low-value transfers inside the EU. According to the company, it runs on regulated EU EMI infrastructure and issues dedicated IBANs for each business.

Core Features

Dedicated IBAN for each company sits alongside multi-account structures so teams can separate revenue, payouts, and pooled funds from one admin console. Role-based user management lets finance staff, approvers, and external accountants have distinct access.

The platform supports SEPA and SWIFT transfers, SEPA on-ramps and off-ramps, and C2B payments. Physical and virtual business cards are listed as coming soon and card controls are expected to be managed from the same dashboard.

Key Differentiator

According to the company, Demivolt’s regulated EU EMI infrastructure plus per-company IBANs and transparent fees target cross-border SMEs that need compliance-first banking without heavyweight legacy relationships. That combination aims to reduce reconciliation friction for international operations.

Pros

-

Faster onboarding and a dedicated account manager reduce back-and-forth for compliance checks. This helps teams get accounts and IBANs issued sooner than long manual bank setups.

-

Transparent fees with clear per-transfer pricing and a free opening month make cash flow forecasting easier compared with hidden traditional bank charges.

-

Support for both SEPA and SWIFT means businesses can centralize EU and non-EU payments while keeping a single platform for outbound controls.

-

Multi-currency support and multi-account structures let growing SMEs isolate currency exposure and client funds without opening multiple legacy bank relationships.

-

A Reseller program enables advisors and partners to refer clients and earn recurring commissions, which can turn a compliance service into a predictable revenue stream.

Cons

- Card issuance is limited right now. Virtual and physical cards are listed as coming soon, so you cannot rely on full card-based expense workflows at launch.

Notable Integrations

Demivolt lists Open Banking (PSD2) connectivity for account linking and a generic Payment Gateway integration for merchant flows. These integrations let you pull transaction data and connect inbound payments to reconciliation engines.

Who It’s For

SMEs, digital businesses, and regulated companies operating across EU borders that need clear pricing, dedicated IBANs, and a compliance-aware provider. Good for firms that want a modern alternative to legacy banks but still need formal regulatory coverage.

Unique Value Proposition

Regulated EU EMI infrastructure with dedicated IBANs and explicit per-transfer fees gives cross-border SMEs predictable costs and clear account separation. According to the company, onboarding is fast and managed with a dedicated account manager, which reduces compliance friction when you scale.

Real World Use Case

A Lithuanian export business centralizes receipts and payouts on Demivolt, issues virtual cards for contractors, and uses separate IBANs per revenue stream to simplify VAT and reconciliation across markets. The reseller program lets their accountant refer similar clients.

Pricing

Free account opening and a free first month. Outgoing SEPA €0.40. Incoming SWIFT €25. Outgoing SWIFT €30. The vendor advertises transparent fees and positions typical usage as cheaper than traditional banks.

Website: https://demivolt.com

Vialet

At a Glance

Instant issuance of virtual Visa and Mastercard cards lets teams start spending within minutes, which is useful for marketing and distributed expense programs. The vendor advertises high-volume payouts and API automation aimed at marketplaces and affiliates, with EU regulatory coverage cited in product materials.

Core Features

- Dedicated IBANs for multi-currency, borderless account structures.

- SEPA and SWIFT rails for inbound and outbound international transfers.

- Virtual Visa and Mastercard cards with instant issuance for programmatic spend.

- Real-time multi-currency exchange with competitive rate execution.

- High-volume payouts and mass transfer automation via REST APIs and webhooks.

Key Differentiator

Engineered payment rails that target complex, regulated businesses. Vialet focuses on throughput and compliance tooling so platforms can process large batches of payouts and run FX flows at scale while keeping operations under a single provider.

Pros

- Fast setup for small transfers. Accounts can be opened quickly for modest volumes, which helps pilots and proofs of concept launch sooner.

- FX execution is live and competitive. The vendor reports real-time rates and instant execution for standard currency corridors.

- Built for volume. The payout automation and API-first approach handle repeated mass transfers without manual work.

- Regulatory posture. Vialet states it operates as a licensed European EMI and keeps client funds in segregated accounts with Tier-1 banks, which matters for risk teams.

- Integration friendly. APIs and platform connectors make it possible to plug Vialet into e-commerce and marketplace stacks.

Cons

- Support responsiveness is a recurring complaint. Trustpilot and other reviews in the product data report slow or unhelpful responses from support.

- Compliance friction. Operational delays and account blocks tied to KYC and policy checks occur often enough to be mentioned by customers.

- Pricing opacity. Published materials are vague; the vendor directs buyers to contact sales for fees and limits, which complicates budgeting for high-volume flows.

- Not ideal for urgent fixes. The combination of slower support and compliance holds makes it risky for teams that need immediate resolution of payment failures.

When It May Not Fit

If your business needs instant, hands-on support for high-risk flows, this will be frustrating. Teams that expect 24/7 live support and transparent, fixed fee schedules will find the vendor’s policy and response patterns a bad match.

Notable Integrations

- SEPA, SWIFT

- Visa and Mastercard networks

- Open Banking APIs

- E-commerce platforms such as WooCommerce, Magento, PrestaShop

- Identity and verification provider Ondato

Who It’s For

Ambitious, high-growth companies and marketplaces that require scalable payout rails, multi-currency accounts, and virtual card programs. Best for businesses with engineering resources to integrate APIs and teams prepared for compliance-driven operational pauses.

Unique Value Proposition

High-volume payout automation and instant virtual card issuance give platforms the plumbing to pay thousands of recipients and control programmatic spend. According to the company, that combination reduces manual reconciliation and lowers internal operations headcount for payout cycles.

Real World Use Case

A marketplace uses Vialet to issue dedicated IBANs, run FX conversions in real time, and push daily mass payouts to vendors via the API. According to the vendor, the setup supports thousands of recipients and centralizes reconciliation into one automated flow.

Pricing

The vendor requires direct contact for pricing. Fees and limits vary by volume, currency mix, and compliance profile, so request a tailored quote and sample fee schedule before pilot launch.

Website: https://vialet.eu

Holvi

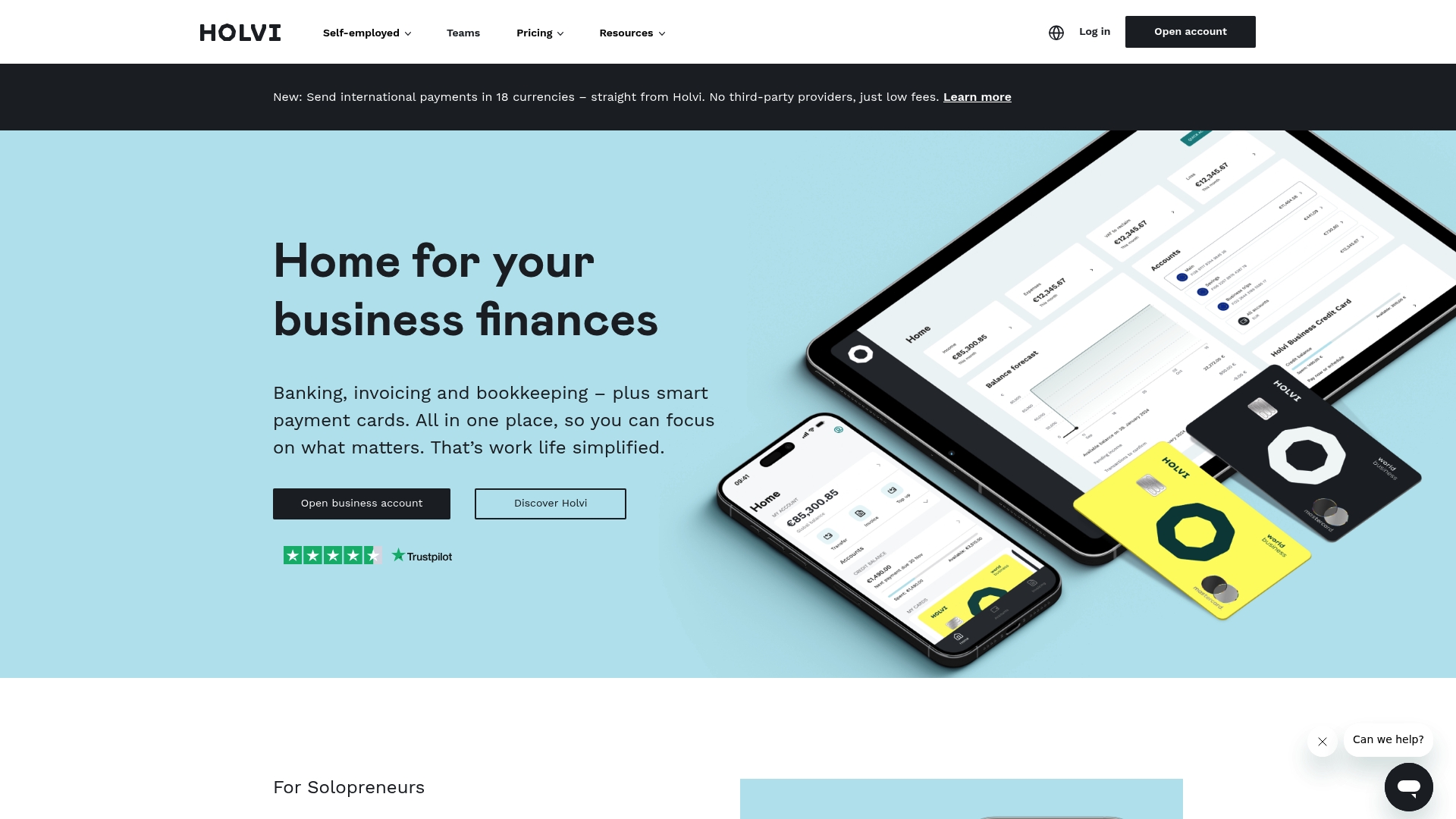

At a Glance

International transfers in 18 currencies with transparent pricing and no third-party provider markup is a standout feature aimed at freelancers and microbusinesses who send or receive payments abroad.

According to the company, Holvi operates as a regulated payment institution in the EU and pairs that with banking-adjacent tools for everyday business finance.

Core Features

Business accounts deliver IBANs across multiple currencies, letting you receive payments like a local entity in many markets.

Integrated invoicing and sales tools speed client billing, while receipt scanning and expense categorization prepare basic bookkeeping entries for tax time.

The platform also issues digital and physical payment cards and supports mobile payments via Apple Pay and Google Pay.

Key Differentiator

Holvi uniquely bundles account IBANs, invoicing, expense capture, and multi-currency transfers in one interface aimed at microbusinesses and solo professionals.

That single-place approach reduces the juggling of separate bank, invoicing, and card services for small operators who want fewer logins and less admin overhead.

Pros

-

User-friendly interface makes everyday tasks such as sending invoices and scanning receipts fast and predictable rather than fiddly.

-

Integrated invoicing lets you generate, send, and track client invoices without jumping between separate tools, which shortens payment cycles for many freelancers.

-

Expense management with receipt scanning reduces manual data entry and helps prepare paperwork for accountants and tax filings.

-

Mobile-first cards and support for Apple Pay and Google Pay suit digital sellers and contractors who pay or get paid on the go.

-

Pricing tiers start low and are affordable for small-scale operations, including a free plan for basic needs.

Cons

-

Several users report intermittent support or payment delays; support responsiveness appears inconsistent across cases.

-

Recent pricing and policy adjustments have caused frustration among long-term customers who relied on older terms.

-

Bookkeeping and reporting remain basic; firms that need advanced accounting automation will still export data to external software.

-

Some users raise questions about ongoing reliability and compliance changes, which creates uncertainty for larger or compliance-sensitive businesses.

When It May Not Fit

Not suited for larger enterprises that need cash-pooling, advanced reporting, or multi-entity accounting. If your workflows require automated bookkeeping across multiple ledgers, Holvi will feel limited and you will need supplementary accounting software or an ERP.

Support inconsistency also makes it a poor choice for teams that require guaranteed SLA-style responsiveness.

Notable Integrations

Holvi lists connectivity for mobile payments such as Apple Pay and Google Pay, and it advertises accounting software connections generally, though specific partners were not specified in the product data.

Who It’s For

Self-employed professionals, freelancers, and very small companies that want a single app for invoicing, expense capture, and multi-currency banking. Good for international contractors who need local-style IBAN receipts without complex treasury requirements.

Unique Value Proposition

Holvi’s business accounts include IBANs across multiple currencies, plus built-in invoicing and receipt capture in the same app. For solo entrepreneurs who trade internationally and do their own bookkeeping, that reduces the number of tools and manual reconciliation steps required each month.

Real World Use Case

A freelance graphic designer issues invoices in euros, collects payments to a euro IBAN, scans receipts into the app, and sends occasional transfers in British pounds without adding foreign exchange middlemen. Daily admin drops from hours to a few focused actions.

Pricing

Plans vary by market starting from a free Holvi Flex tier up to business plans. Paid tiers generally range from about €9 per month to €50 per month depending on accounts, transaction volume, and added tools.

Website: https://www.holvi.com

Wise (formerly TransferWise)

At a Glance

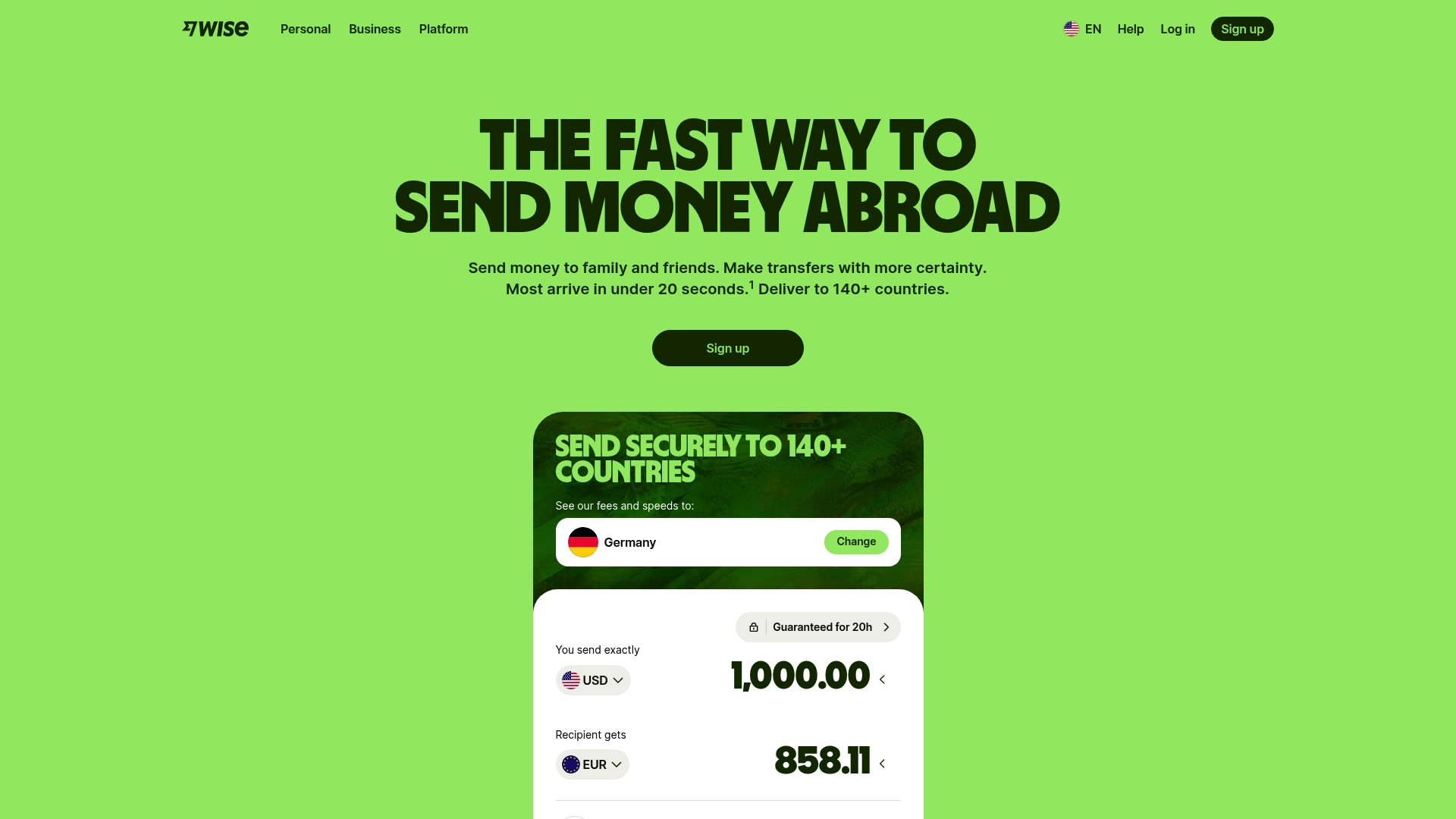

Wise reports that transfers often arrive within seconds and that it uses mid-market exchange rates with upfront fees. That combination is the most concrete advantage for businesses moving money across borders, according to the company.

Core Features

Wise supports sending and receiving international payments, holding balances in more than 50 currencies, and issuing a Multi Currency Card for spending abroad. The platform also offers an interest program for USD, GBP, and EUR balances and provides a business API for automation.

Key Differentiator

According to the company, Wise combines real-time mid-market rates with transparent fee breakdowns and rapid payment routing. The vendor advertises these traits as the primary reason customers avoid traditional bank markups and opaque charges.

Pros

- Easy onboarding and a straightforward app experience. Most users set up accounts and initiate first transfers without a long learning curve.

- Transparent fees and an upfront rate display reduce surprise costs for cross-border payouts.

- Fast throughput for many corridors. Wise reports that certain transfers settle in seconds or minutes rather than days.

- Multi currency balances plus the Multi Currency Card let freelancers and small teams hold, convert, and spend without juggling separate local accounts.

- API access supports automated pay runs and integrates with accounting workflows for bookkeeping efficiency.

Cons

- Some users report verification holds and delays. Verification can require documentation and manual review with variable timelines.

- Customer service response times are inconsistent for complex disputes, based on third-party reviews.

- Occasional unexpected fees or refund processing delays have been reported in public feedback.

- Not an in-person banking option. No branch access for cash deposits or teller services.

When It May Not Fit

Wise is unsuited for businesses that need high transaction limits without extensive verification. It is also a poor match for companies that require physical branch services or cash handling. Large enterprises needing bespoke treasury features may prefer a commercial bank or a specialized payments partner.

Notable Integrations

- API for business and fintech integrations lets finance teams automate payouts and reconcile at scale.

- Connects with common accounting software to map payments and bank-like balances into ledgers and expense workflows.

Who It’s For

Freelancers, expats, and small to medium enterprises that move money internationally and want lower exchange costs and faster settlement than many traditional banks offer. Also useful for businesses that can operate fully online without branch needs.

Unique Value Proposition

Wise reports mid-market exchange rates with transparent, itemized fees and fast rails for many currency pairs. For teams paying suppliers or contractors across borders, that arithmetic often reduces FX cost and speeds cash flow compared with conventional bank transfers.

Real World Use Case

A U.S. freelancer pays a European supplier in euros, converts funds at the vendor‑reported mid-market rate, and the recipient accesses funds on a Multi Currency Card the same day. Accounting records map cleanly via the Wise API to the freelancer’s bookkeeping platform.

Pricing

Fees vary by corridor, amount, and payout method. Wise provides a fee calculator on its site so you can preview the exact cost before sending funds.

Website: https://wise.com

Revolut

At a Glance

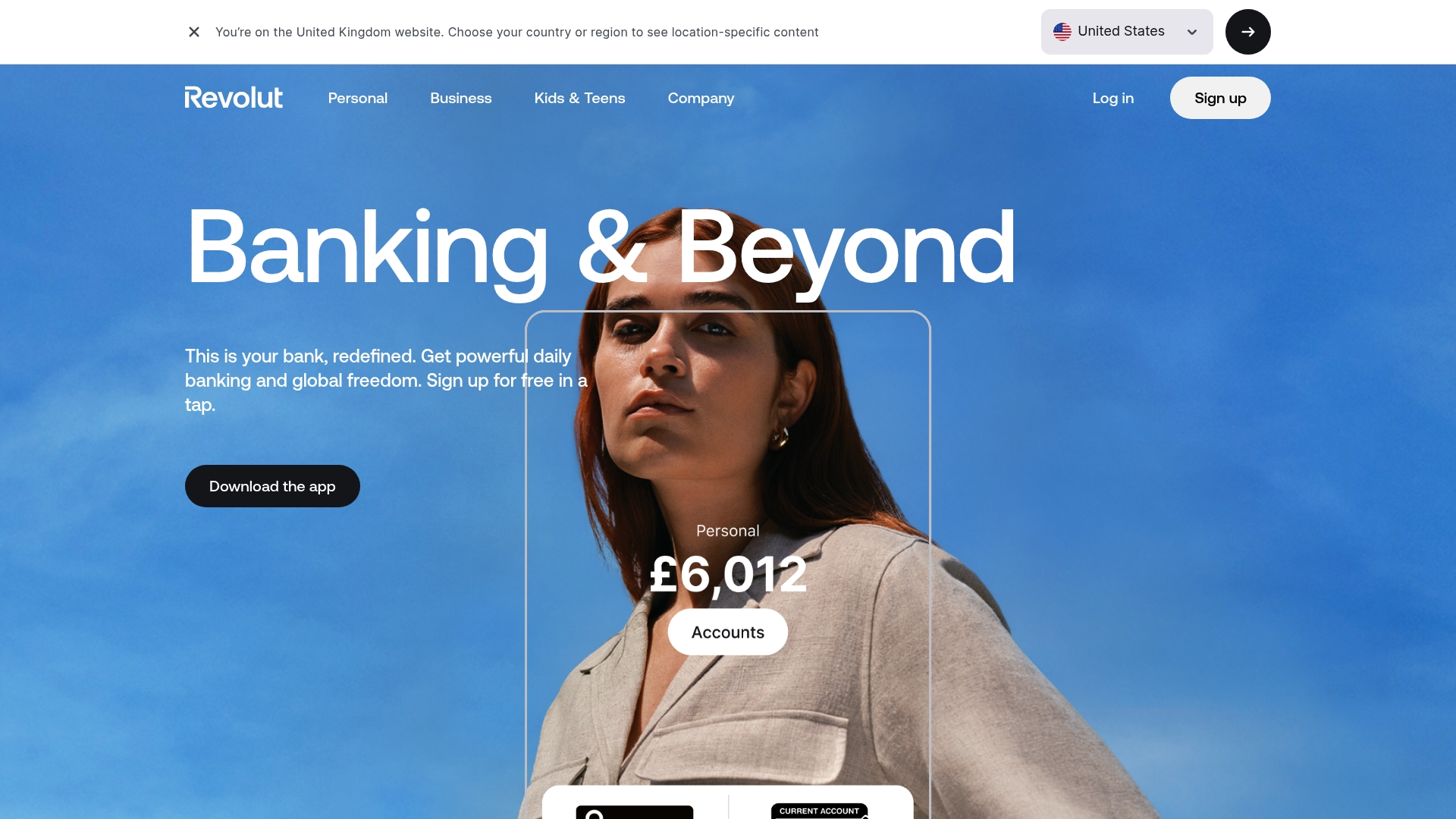

Revolut reports over 70 million customers worldwide and supports multi-currency accounts in 36 currencies, which makes holding and spending multiple currencies simple for frequent travelers and international businesses. The app pairs competitive FX with card controls and in-app financial tools.

Core Features

- Multi-currency accounts with local and foreign currency balances.

- Real-time exchange rates with no weekday markup and instant currency conversion.

- Virtual and physical debit cards with quick freeze and disposable virtual cards for one-off payments.

- In-app investing for stocks and cryptocurrencies plus savings accounts with up to 4% AER interest.

- AI assistant AIR for instant support and proactive fraud defenses for account protection.

Key Differentiator

Revolut advertises real-time interbank exchange rates and no weekday FX markup on many conversions. That pricing model plus multi-currency wallets and fast card issuance positions it as a payment-first digital bank for people and companies transacting across borders.

Pros

- The app is intuitive and makes transfers, currency conversion, and card management feel fast and direct. Setup and card issuance happen in minutes.

- Competitive exchange pricing during market hours keeps conversion costs low for frequent FX volumes. This is a clear cost advantage for cross-border payees.

- Travel friendly. Holding local currency and instant spending with minimal fees reduces reliance on cash or expensive card markups.

- Extra features like savings accounts, investing, and rewards let small businesses consolidate financial tasks in one mobile interface.

- Security features and fraud monitoring are prominent in the app and marketing materials which aim to reduce unauthorized activity.

Cons

- Account lockouts and identity verification steps can be frequent and disruptive for busy users who need immediate access.

- Weekend FX markups and occasional fee changes introduce unpredictability for finance teams expecting fixed conversion costs.

- Dispute resolution and some customer support threads can be slow or unsatisfying for commercial transaction disputes.

- Credit products are limited compared with traditional banks which matters for companies needing loans or mortgages.

When It May Not Fit

If your company needs full retail banking services like mortgages or business lending, Revolut is not a substitute for a high-street bank. Companies operating in the US, Australia, or Singapore may see reduced functionality where Revolut lacks a full local banking license. Frequent account verifications can interrupt time-sensitive payments.

Notable Integrations

- Sage

- QuickBooks

- Xero These connections help export transactions and reconcile accounts in common accounting platforms used by SMEs.

Who It’s For

Tech-savvy SMEs, export-focused small businesses, and remote teams that run international payroll, pay suppliers in multiple currencies, or travel regularly. Ideal when you prioritize low FX costs and fast card issuance over traditional lending features.

Unique Value Proposition

Revolut advertises real-time interbank exchange rates with no weekday markup as a concrete pricing advantage for cross-border transactions. Combine that with multi-currency wallets, instant virtual cards, and integrated accounting connectors and you get a compact toolkit for managing international cash flow.

Real World Use Case

A freelance digital nomad or small consultancy holds euros and dollars, issues instant virtual cards for contractors, and sends client invoices paid in local currencies. FX conversions happen during market hours at competitive rates and bookkeeping exports feed QuickBooks.

Pricing

Free basic account available. Paid personal and business plans run from £3.99 per month (Plus) up to £55 per month (Ultra) with higher limits, travel perks, and expanded rewards.

Website: https://www.revolut.com

Comparative Analysis of Financial Platforms for SMEs

When evaluating financial platforms tailored for SMEs, Demivolt stands out by offering transparent per-transaction fees combined with regulatory-compliant infrastructure, directly addressing the needs of cross-border operations. In contrast, competitors prioritize alternate strengths such as immediate card issuance, comprehensive API integration, and tools tailored for freelancers.

Predictability and Transparency in Transaction Fees

Demivolt sets itself apart with its clear, upfront pricing model for transactions, ensuring businesses can accurately forecast cash flow without surprise fees. For example, outgoing SEPA transfers incur a straightforward cost of €0.40. On the other hand, platforms like Vialet and Holvi demonstrate pricing opacity or reliance on quote-based systems, which may pose challenges for businesses seeking cost predictability.

However, Demivolt’s offerings in this area are counterbalanced by competitors such as Wise, renowned for its mid-market FX rates devoid of significant markups. For businesses heavily involved in currency conversion, the benefits of Wise’s transparent currency exchange approach could be compelling.

Features Supporting Operational Scalability

Demivolt enables businesses to scale effectively through dedicated, segregated IBANs and multi-account structures, enhancing financial management and compliance. Additionally, its regulated EMI foundation provides a reassurance level not found in platforms focused solely on speed and accessibility, such as Revolut, which targets tech-savvy SMEs needing immediate cards and wallet setups.

On the other hand, Vialet supports high-volume payouts through its API-friendly architecture suitable for marketplaces. This emphasis on programmability and automation makes Vialet more attractive for businesses requiring scalable payout solutions than Demivolt’s current slightly limited integration points.

Choosing the Right Platform for Your Needs

Different platforms serve distinct business profiles:

- Choose Demivolt if you require transparent per-transaction fees and a compliance-aware structure, particularly for SMEs operating across EU borders.

- Choose Vialet for its robust API integrations and scalability in high-volume transactional flows.

- Choose Holvi if you are a freelancer or sole proprietor needing an all-in-one platform for invoicing, IBANs, and transactional tools.

- Choose Wise for its mid-market exchange rates and accessible cross-border payment systems.

Our Recommendation

Demivolt uniquely combines transparent per-transaction pricing with compliance-focused EMI infrastructure, making it the preferred choice for European SMEs engaged in predictable payment flows. However, if your business leans heavily on API integrations for mass payouts or requires instant card issuance for spending programs, Vialet or Revolut may better fulfill those specific needs. For businesses desiring clear and direct payment processing aligned with regulatory standards, Demivolt provides an excellent operational fit.

Digital Banking Solutions Comparison

In assessing options for SMEs requiring cross-border transactions, compliance, and multi-currency capabilities, consider the following key features and distinctions.

| Product | Core Feature | Key Differentiator | Best For | Pricing | Notable Limitation |

|---|---|---|---|---|---|

| Demivolt | Dedicated IBANs and SEPA/SWIFT support | Regulated EU EMI infrastructure with transparent fees | SMEs operating across EU borders | Free for first month, €0.40 outgoing SEPA | Card issuance currently unavailable |

| Vialet | Instant Visa/Mastercard issuance with APIs | High-volume payouts and FX processing | Affiliates and marketplaces with mass payouts | Not disclosed | Complaints about slow support responsiveness |

| Holvi | Integrated invoicing and receipt capture | Combined business tools with multi-currency IBANs | Freelancers managing simple finances | €9–€50/month based on tier | Basic bookkeeping and support inconsistencies |

| Wise | Transparent mid-market FX rates | Real-time transfer speed and predictable fees | Freelancers and SMEs moving money internationally | Fee varies by transaction; fee calculator online | Verification holds create potential delays |

| Revolut | Multi-currency accounts and instant virtual cards | Real-time interbank rates with mobile-first tools | Tech-savvy SMEs with minimal cash needs | Free to £55/month depending on plan | Frequent account verifications may interrupt payments |

Discover Smarter Business Banking Beyond LinkedIn Alternatives

If you are exploring lt.linkedin.com alternatives, you might be looking for reliable platforms that support cross-border business needs with transparency and compliance. Teams handling international payments face challenges like complex onboarding, opaque fees, and fragmented account control. Demivolt solves these issues by offering dedicated IBANs, clear per-transfer fees, and fast onboarding tailored for European SMEs moving money within and outside the EU.

Experience how Demivolt empowers businesses with multi-account management and compliance-first infrastructure. Open your digital-first business account today and manage SEPA and SWIFT payments confidently. Take charge by opening your dedicated IBAN and enjoy transparent pricing that simplifies forecasting.

Frequently Asked Questions

What is the pricing structure for Demivolt, and how does it benefit low-value transfers?

Demivolt charges €0.40 for outgoing SEPA transfers, with a free first month for new users. This transparent pricing structure helps businesses that engage in frequent, low-value transactions to manage their cash flow effectively without worrying about hidden fees.

How does Demivolt’s dedicated IBAN feature improve financial management for SMEs?

Demivolt provides a dedicated IBAN for each company, allowing SMEs to separate revenue, payouts, and pooled funds within one admin console. This multi-account structure simplifies financial tracking and enhances compliance, making it easier for businesses to manage their international operations.

Can I use Demivolt for both SEPA and SWIFT transfers, and how does this flexibility help my business?

Yes, Demivolt supports both SEPA and SWIFT transfers. This flexibility allows businesses to centralize their payment operations, making it easier to manage EU and non-EU transactions all from a single platform, which reduces reconciliation friction.

What sets Demivolt apart compared to Vialet when handling compliance for cross-border transactions?

While Vialet offers fast setup for high-volume payouts, Demivolt’s focus on regulated EU EMI infrastructure and dedicated IBANs makes it a better fit for businesses needing strong compliance support. Demivolt’s workflow minimizes compliance friction while onboarding, which is crucial for scaling SMEs.

How does Demivolt’s reseller program work, and what advantages does it provide?

Demivolt offers a reseller program that allows advisors and partners to refer clients and earn recurring commissions. This not only creates a revenue stream for accountants and financial advisors but also helps spread awareness of the compliance services, making it an attractive option for firms that work with various SMEs.