TL;DR:

- AI and automation significantly increase SME banking efficiency, reducing processing times and human error.

- Cross-border payment standards are evolving, demanding faster, multi-currency solutions with structured data compliance.

- SMEs should prioritize regulatory compliance and operational resilience before investing in advanced banking technologies.

Business banking is changing faster than most SME leaders realize. AI and automation are driving dramatic efficiency gains across core banking operations, while new compliance mandates and cross-border payment standards are reshaping what it means to run a financially sound business in Europe. Whether you manage a growing e-commerce brand, a digital services firm, or a cross-border trading operation, the banking decisions you make in 2026 will directly affect your speed, cost, and regulatory standing. This article breaks down the five most important trends, what they mean in practice, and how to act on them.

Table of Contents

- The rise of AI and automation in SME banking

- Cross-border payments and international banking capabilities

- Navigating compliance, regulation, and lending barriers

- Banking choices: Traditional institutions vs. fintech alternatives

- Our view: What most SME leaders miss about banking trends

- Explore banking solutions built for modern SMEs

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| AI drives efficiency | Automation and AI can cut banking tasks from hours to minutes, giving SMEs significant operational gains. |

| Cross-border dominates | Instant payments and multi-currency options are now standard, fueling rapid international SME expansion. |

| Compliance is crucial | New regulations require structured data and real-time screening, pushing SMEs to rethink banking partners. |

| Fintech bridges gaps | Fintechs and neobanks offer fast, flexible solutions where traditional banks lag, especially for lending and global payments. |

| Smart integration wins | SMEs benefit most when they upgrade selectively—adopting only tools that solve real operational or compliance needs. |

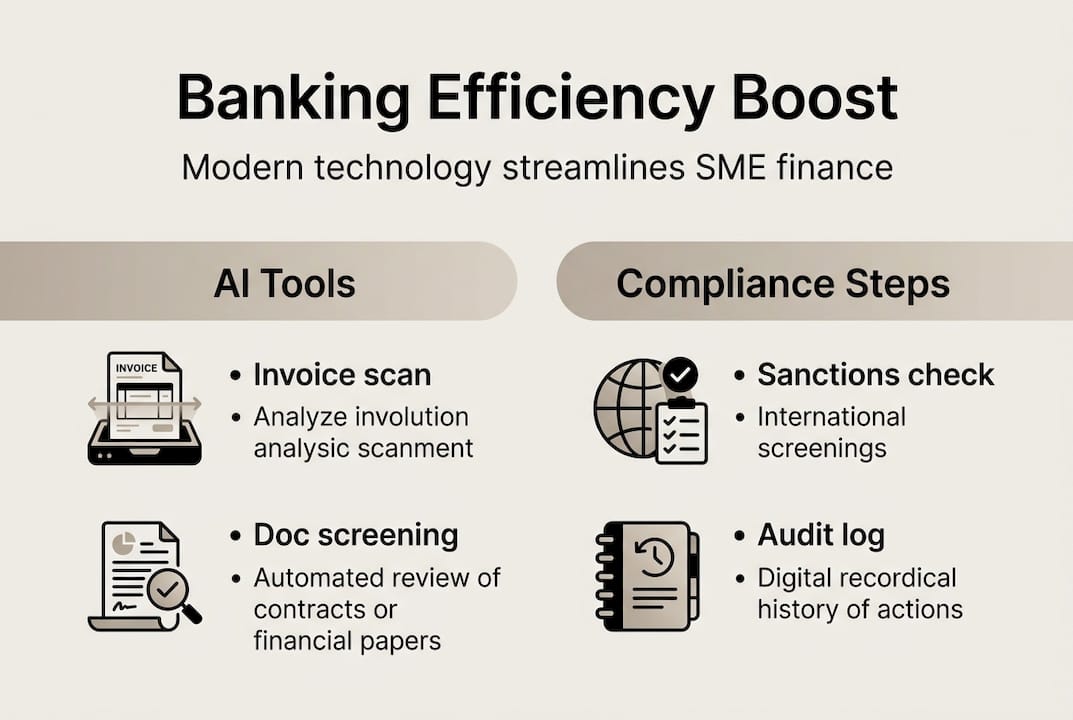

The rise of AI and automation in SME banking

AI is no longer a future concept in business banking. It is already processing invoices, screening documents, and flagging compliance issues in real time. The numbers tell a clear story: case studies show 50% FTE gains and 90% time reductions in core banking processes, meaning teams that once needed ten people to manage financial operations can now do the same work with five. That is not a marginal improvement. That is a structural shift in how SMEs compete.

The most visible change is in document handling. Document processing times have dropped from 10 to 15 minutes per document to under a minute using AI. For a business processing hundreds of supplier invoices or onboarding documents each month, that adds up to thousands of recovered hours annually.

Here is a snapshot of how AI is transforming common SME banking tasks:

| Task | Traditional time | AI-assisted time | Efficiency gain |

|---|---|---|---|

| Invoice processing | 10-15 min | Under 1 min | Over 90% |

| KYC document review | 2-3 days | Hours | 70-80% |

| Payment reconciliation | Manual, hours | Automated, minutes | 60-75% |

| Fraud detection | Reactive | Real-time | Significant |

The practical benefits go beyond speed. Automation reduces human error, creates audit trails automatically, and allows your finance team to focus on decisions rather than data entry. SMEs that embrace fintechs and operational speed are already pulling ahead of competitors still relying on manual workflows.

Key areas where automation delivers immediate SME value:

- Invoice and accounts payable processing with automatic matching and approval routing

- Onboarding and KYC with AI-driven document verification

- Real-time payment monitoring for fraud and compliance flags

- Automated reconciliation across multiple accounts and currencies

Pro Tip: Before investing in any AI banking tool, map your three most time-consuming financial tasks. Target automation there first. Generic platforms that promise everything often solve nothing specific.

The broader context matters too. Fintech innovation in banking is accelerating the adoption curve, meaning the gap between early adopters and late movers is widening every quarter.

Cross-border payments and international banking capabilities

For European SMEs with international ambitions, the payments landscape is shifting fast. Cross-border payment volumes are growing from $194 trillion in 2024 to a projected $320 trillion by 2032, driven by e-commerce growth, global supply chains, and digital services. That scale demands infrastructure that most traditional banks were not built to handle.

SEPA Instant is now the baseline for euro payments within the EU, enabling transfers in under ten seconds around the clock. ISO 20022, the new global messaging standard for financial transactions, is adding structured data to every payment, which means richer information travels with each transfer. By November 2026, the EU mandates structured addresses in all cross-border payment messages, a compliance deadline that will catch unprepared businesses off guard.

28% of UK SMEs plan international expansion, and that figure is rising across continental Europe too. Multi-currency accounts are no longer a luxury for large corporations. They are a practical tool for any SME managing suppliers, clients, or staff across borders.

| Feature | Traditional bank | Fintech/neobank |

|---|---|---|

| SEPA Instant support | Partial or delayed | Standard |

| Multi-currency accounts | Limited, high fees | Flexible, lower cost |

| ISO 20022 readiness | Variable | Built-in |

| Cross-border speed | 1-3 business days | Minutes to hours |

The advantages of modern cross-border payment solutions for SMEs include:

- Dedicated IBAN accounts in multiple currencies

- Real-time payment status visibility

- Automated FX conversion at competitive rates

- Structured data compliance built into the payment flow

The rise of agentic commerce trends is also adding new complexity. AI-driven purchasing agents are beginning to initiate and authorize payments autonomously, which means your payment infrastructure needs to handle programmatic transactions, not just human-initiated ones.

Navigating compliance, regulation, and lending barriers

Compliance is where many SMEs feel the most pressure, and 2026 is adding new layers. The ECB reports a net 7% tightening in lending standards across the euro area, while a €474 billion SME financing gap is pushing businesses toward alternative funding sources. At the same time, regulatory requirements are multiplying.

The Digital Operational Resilience Act, known as DORA, now requires financial entities and their ICT service providers to meet strict resilience standards. For SMEs using banking platforms or payment processors, this means your providers must demonstrate tested recovery plans and incident reporting capabilities. Choosing a non-compliant provider creates operational and legal risk for your business.

Real-time sanctions screening is becoming standard. Every outbound payment must be checked against updated sanctions lists before processing. The November 2026 structured address mandate adds another layer: payments missing compliant address data may be rejected or delayed.

“28% increase in financing costs and collateral requirements, with only 7% of euro area firms using significant AI in their financial operations.”

Here is how SMEs can stay ahead of compliance requirements:

- Audit your current banking provider’s DORA compliance status before Q3 2026.

- Update all payment templates to include structured address fields ahead of the November deadline.

- Review your sanctions screening process to confirm it runs in real time, not in batch.

- Document your ICT risk management procedures, even if you are not a financial institution yourself.

| Compliance area | Deadline/status | SME action required |

|---|---|---|

| DORA ICT resilience | Active 2025 | Verify provider compliance |

| Structured addresses | November 2026 | Update payment templates |

| Real-time sanctions screening | Active now | Confirm provider capability |

| Tighter lending standards | Ongoing | Explore alternative finance |

Pro Tip: Ask your banking provider directly for their DORA compliance documentation. If they cannot produce it quickly, that tells you something important about their operational maturity.

The fintech regulatory impact is significant here. Regulated fintechs often move faster on compliance updates than traditional banks because their infrastructure is built to adapt. Understanding modern financial compliance is no longer optional for SME decision-makers.

Banking choices: Traditional institutions vs. fintech alternatives

Choosing where to bank is one of the most consequential operational decisions an SME can make. The data shows stark differences depending on where you are in Europe. SME loan approval rates range from 96 to 98% in France, 56% in the UK, and just 37.8% in Germany. If you are operating in a low-approval market, waiting for a traditional bank to say yes is a strategy that can stall your growth for months.

Fintech alternatives have grown into a $151.4 billion market precisely because traditional banks leave gaps. Fintechs excel in speed and cross-border API solutions, while banks lead in collateral-based lending for larger, asset-backed facilities.

| Criteria | Traditional bank | Fintech/neobank |

|---|---|---|

| Loan approval speed | Weeks to months | Days |

| Collateral requirements | High | Low to none |

| Cross-border capability | Limited, costly | Built-in, affordable |

| Compliance infrastructure | Established | Modern, adaptive |

| Account opening time | Days to weeks | Hours |

For most European SMEs, the answer is not either/or. It is a deliberate combination. Use traditional banking relationships for long-term credit facilities where collateral works in your favor. Use fintech platforms for day-to-day operations, cross-border payments, and compliance-sensitive workflows where speed and adaptability matter.

Key advantages of fintech banking for SMEs:

- Faster onboarding with digital KYC and automated verification

- Multi-account structures for separating operational and reserve funds

- Role-based access so your finance team has the right permissions without sharing credentials

- API integrations that connect your banking data directly to your accounting or ERP system

The fintech industry reshaping global financial services is not slowing down. SMEs that treat their banking stack as a strategic asset rather than a utility will have a measurable advantage in cost, speed, and resilience.

Pro Tip: Run a simple audit of your last 90 days of banking friction. Count the hours lost to manual reconciliation, delayed payments, or compliance questions. That number is your ROI case for switching or supplementing your current provider.

Our view: What most SME leaders miss about banking trends

Here is the uncomfortable truth: most SME leaders spend more time evaluating their CRM than their banking infrastructure. They chase the latest AI feature announcement while ignoring whether their payment provider will be DORA-compliant by year end. That is a costly mismatch of priorities.

Modernization is not about having the most sophisticated technology. It is about solving the right problems. An SME that automates invoice processing before fixing its cross-border payment delays has optimized the wrong thing. The businesses we see winning are those that start with compliance and operational continuity, then layer in efficiency tools where they create measurable impact.

The hard-won lesson is this: efficiency and compliance beat shiny apps every time. A platform that keeps your funds segregated, processes payments in real time, and passes a DORA audit is worth more than one with a polished interface and no regulatory backbone. Explore business banking insights to keep building on this foundation with practical, actionable guidance.

Explore banking solutions built for modern SMEs

The trends covered in this article are not abstract. They are shaping how European SMEs access capital, process payments, and stay compliant right now. If your current banking setup is creating friction instead of removing it, that is a problem worth solving before it compounds.

Demivolt offers regulated, digital-first SME banking solutions designed specifically for European businesses that need IBAN accounts, SEPA and SWIFT payment capabilities, multi-currency support, and compliance-ready infrastructure. Onboarding is fast, transparent, and built to meet EU regulatory standards. Whether you are expanding cross-border or simply need a banking partner that keeps pace with your operations, Demivolt gives you the control and clarity to move forward with confidence.

Frequently asked questions

How can AI and automation benefit SME banking operations?

AI delivers 50% efficiency gains by streamlining invoice processing, document management, and reconciliation, freeing thousands of hours annually for European SMEs to focus on growth instead of administration.

What are the latest compliance mandates impacting SME banking in Europe?

SMEs face new rules for structured data and real-time sanctions screening, plus DORA for ICT resilience and stricter lending standards that are tightening access to traditional credit across the euro area.

Why are fintech and neobank solutions becoming popular among SMEs?

Fintechs and neobanks offer fast approval, multi-currency accounts, and built-in compliance tools, helping SMEs bridge financing gaps in a fintech alternatives market now valued at $151.4 billion.

How do SME loan approval rates differ across Europe?

Approval rates vary sharply: France sees 96 to 98%, the UK 56%, and Germany 37.8%, making fintech alternatives an essential option for SMEs in lower-approval markets.