TL;DR:

- Managing multiple cross-border accounts has become accessible for SMEs thanks to fintech platforms that enable rapid, API-driven setup. Proper preparatory documentation, including up-to-date KYB packages and ownership charts, significantly reduces delays and verification time. Ongoing compliance and strategic automation optimize cross-border payment operations at scale, ensuring efficiency and regulatory adherence.

Managing multiple accounts across currencies and jurisdictions sounds like a treasury problem reserved for large corporations. It isn’t. SMEs and digital-first businesses running cross-border operations face the same complexity, often without dedicated finance teams to absorb the friction. The multi-account setup process is where most of that friction concentrates: mismatched documents, confused entity types, manual verification loops, and delayed account access. The good news is that compliant fintech platforms have compressed what used to take weeks into something far more manageable. Account setup completes within 24 hours after KYB verification on modern API-driven platforms. This guide walks you through the full process, from document prep to account optimization.

Table of Contents

- Understanding the prerequisites for multi-account setup

- Step-by-step multi-account setup process with automation

- Best practices and common pitfalls during multi-account setup

- Verifying and optimizing multi-account setups for scaling cross-border payments

- Why most multi-account setups miss key efficiencies and how to get them right

- Explore Demivolt’s multi-account solutions for seamless business banking

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Streamlined setup process | Multi-account setups can complete within 24 hours after digital KYB on compliant fintech platforms. |

| Essential KYB documents | Collect and verify key entity documents like incorporation certificates and beneficial owner IDs upfront. |

| API automation saves time | Using API integration reduces setup time significantly compared to manual account creation. |

| Avoid common delays | Submitting stale documents and misclassifying entity types cause frequent verification delays. |

| Optimize account management | Verify accounts promptly and use batching and FX timing to cut costs for cross-border payments. |

Understanding the prerequisites for multi-account setup

Before you touch an application form or initiate an API call, your documentation needs to be in order. This is where most SMEs lose days, sometimes weeks, and where the gap between a smooth setup and a painful one is decided.

Every entity in your structure requires its own verification package. KYB requires 3-5 core documents per entity, including Certificate of Incorporation, Memorandum or Articles of Association (MoA/AoA), and government-issued IDs for all ultimate beneficial owners (UBOs). Complex group structures involving holding companies, subsidiaries, or nominee arrangements push verification timelines to 10-15 business days. Plan for that reality before you begin.

Core KYB documents you will need per entity:

- Certificate of Incorporation (issued within the last 3 months where required)

- Memorandum and/or Articles of Association

- Proof of registered business address

- Government-issued photo ID for each UBO holding 25% or more

- Proof of UBO address (utility bill or bank statement, typically no older than 3 months)

- Corporate ownership chart for entities with layered structures

One thing most multi-account setup guides skip entirely: ongoing monitoring is not optional. Regulatory compliance does not end at account opening. Platforms operating under EU financial regulation will require periodic re-verification, and any material change in ownership or structure triggers a fresh review cycle. Build that expectation into your operations before you sign up.

You should also review our cross-border compliance checklist to make sure nothing falls through the cracks before you begin.

| Document type | Accepted format | Maximum age |

|---|---|---|

| Certificate of Incorporation | Official registry copy | Varies by jurisdiction |

| Proof of address (entity) | Utility bill or bank statement | 3 months |

| UBO photo ID | Passport or national ID card | Valid and not expired |

| UBO proof of address | Utility bill or bank statement | 3 months |

| Ownership chart | Notarized or certified copy | Current as of submission |

Pro Tip: Prepare a dedicated folder per entity with every document labeled clearly. Platforms with automated KYB verification can process a clean, complete submission far faster than one that requires back-and-forth to clarify missing items.

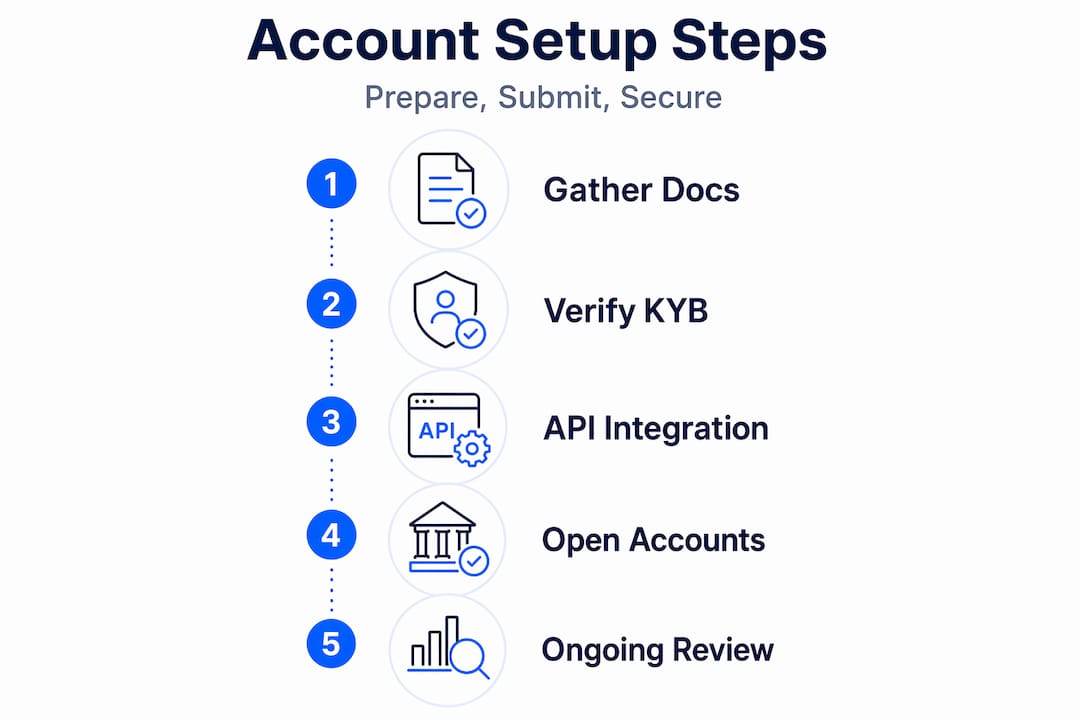

Step-by-step multi-account setup process with automation

With your documents ready, the actual account creation on a capable fintech platform is more technical than most SMEs expect. That is a feature, not a drawback. Automation reduces errors and cuts setup time dramatically.

Manual KYB multiplies setup time by 5x compared to API-driven approaches. For an SME opening accounts in five currencies, that difference is the gap between being operational in a day versus a month. The practical steps below assume you are working with a platform that exposes an API for account creation, which is standard on modern fintech infrastructure.

Step-by-step multi-account creation steps:

- Complete entity KYB. Submit all required documents for each legal entity. This unlocks account creation for that entity.

- Initiate API account creation calls. Specify the currency, country, and account type (dedicated IBAN or virtual account) in each API request.

- Receive account credentials. The platform returns local banking details, including IBAN, sort code, or routing number depending on the currency/region.

- Configure webhook notifications. Set up webhooks to receive real-time alerts for inbound payments, outbound payment status, and account events.

- Test the full payment lifecycle. Send a small inbound transfer and initiate a test outbound payment for each account. Confirm the webhook fires correctly.

- Pilot for 2-4 weeks. Run real but low-volume transactions before fully migrating payment flows. This surfaces edge cases before they become operational problems.

- Scale account creation. Once the pilot is clean, replicate the API workflow for remaining currencies and entities.

Refer to our managing multiple accounts guide for a deeper breakdown of the day-to-day workflow once accounts are live.

Pooled vs. dedicated accounts: what actually matters

| Factor | Pooled accounts | Dedicated accounts |

|---|---|---|

| Cost per account | Lower | Higher |

| Compliance transparency | Lower (harder to trace per entity) | Higher (clear per-entity audit trail) |

| Reconciliation effort | Higher | Lower |

| Regulatory suitability | Limited for regulated entities | Preferred for compliance-heavy operations |

| Local banking details | Shared reference system | Unique IBAN per account |

The compliance case for dedicated accounts is strong if you are operating across multiple jurisdictions or handling client funds. The audit trail alone justifies the marginal cost difference.

Pro Tip: Use a fintech onboarding checklist to map every account you need before starting API calls. Trying to add accounts ad hoc mid-setup creates configuration gaps and reconciliation headaches.

Best practices and common pitfalls during multi-account setup

Knowing the process is essential, but avoiding common pitfalls ensures a smoother setup experience. The mistakes below are not rare edge cases. They show up constantly, and they are all preventable.

The most common mistakes that delay account setup:

- Treating sole proprietors as legal entities. Confusing sole proprietors with legal entities delays verification by 5-10 days. A sole proprietor is a natural person, not a company. Their EIN or registration number belongs to the individual, and KYB requirements apply differently. Getting this wrong at submission forces a manual review and a fresh document request.

- Submitting a DBA (Doing Business As) as a legal entity. A DBA is a trade name, not a legal structure. It does not have its own incorporation documents. Submitting DBA documentation as if it were a registered company is one of the most common first-submission errors and one of the easiest to avoid.

- Using stale documents. Certificates or address proofs older than three months are frequently rejected outright. Many SMEs pull documents from their accounting records without checking the date. Don’t.

- Mismatched entity names on bank statements. For cross-border account openings, the entity name on your bank statement must match the registered legal name exactly. Abbreviations, trading names, or minor variations cause verification failures.

- Incomplete UBO screening. If a UBO appears on a sanctions list or politically exposed persons (PEP) register, the platform must flag the application. Pre-screening your UBOs before submission avoids surprises and accelerates the process.

“Bring a full ownership tree diagram to your KYB submission. Platforms processing complex structures without one spend days requesting clarification. That document alone can shave 5-7 days off your verification timeline.”

Pro Tip: If your entity has a layered ownership structure with multiple holding companies, prepare a certified organizational chart showing percentage ownership at every level. It removes the single most common source of back-and-forth in complex KYB submissions.

You can also use the cross-border compliance tips as a pre-submission checklist to catch errors before they reach the platform.

Verifying and optimizing multi-account setups for scaling cross-border payments

After setup, the focus shifts to confirming everything works as expected and building the operational habits that keep it working as your payment volumes grow.

Verification and optimization steps:

- Confirm local banking details. Immediately after KYB approval, verify that each account has the correct local details: IBAN for EU accounts, sort code and account number for UK accounts. Account setup via API provides local bank details in multiple currencies within 24 hours of verification.

- Test payment rails. Send a small SEPA credit transfer and a SWIFT test payment. Confirm receipt times and fees match your platform’s documentation.

- Verify webhook accuracy. Cross-check webhook event data against your accounting system. A mismatch here, caught early, prevents reconciliation problems at scale.

- Batch outbound payments. Group same-currency outbound payments into batches rather than sending individually. This reduces per-transaction fees and simplifies reconciliation.

- Time FX conversions strategically. If you hold accounts in multiple currencies, monitor interbank rate windows and convert during periods of lower spread. Over time, this produces measurable savings.

- Schedule annual re-verification. Build a reminder system for annual KYB reviews. Regulatory requirements mandate re-verification, and missing a cycle creates compliance exposure.

| Optimization action | Benefit | Frequency |

|---|---|---|

| Batch outbound payments | Reduces transaction fees | Daily or weekly |

| FX timing | Lowers conversion costs | As needed |

| Webhook reconciliation checks | Ensures data accuracy | Weekly |

| UBO and sanctions re-screening | Maintains compliance | Annually or on alerts |

| Local rail usage (SEPA, Faster Payments) | Faster settlement, lower fees | Per payment |

Understanding how local payment rails interact with your accounts is not optional for scaling. Read more about how fintechs facilitate cross-border payments for a practical breakdown of the underlying infrastructure.

Pro Tip: Once your accounts are live, set up a monthly reconciliation review comparing your platform’s transaction records against your accounting system. Early discrepancies are easy to fix. Discrepancies discovered six months later are not.

Also review our IBAN accounts guide for a detailed breakdown of how dedicated IBAN accounts function in practice for cross-border payment flows.

Why most multi-account setups miss key efficiencies and how to get them right

Most multi-account management guides focus on the steps. Few focus on where the real time goes. Here’s what experience actually teaches.

The single biggest efficiency killer in multi-account setups is not complexity. It is documentation overconfidence. SMEs assume their existing corporate documents are ready to submit. Fintechs reject 40% of first-attempt KYB applications because of stale documents older than three months. That rejection resets the clock entirely.

The second efficiency killer is treating the ownership structure as implicit knowledge. Your lawyers and accountants know who owns what. The compliance team at your fintech platform does not, and they cannot proceed without a clear, documented ownership tree. Companies that bring a certified org chart on first submission consistently clear verification faster than those that piece it together reactively.

There is also a meaningful shortcut most SMEs overlook entirely: virtual accounts. For businesses that need local banking details quickly in a new market, a virtual account under an existing verified entity can be issued almost immediately. You get the local IBAN or account number without opening a full new legal entity or waiting for a fresh KYB cycle. This is how experienced operators get operational in a new currency within hours rather than weeks.

The broader lesson is that the process for multi-account setup rewards preparation disproportionately. An hour spent pre-screening your UBOs, organizing documents by entity, and mapping your ownership tree can eliminate five to ten days of verification delays. The businesses that treat documentation as the real work, not the setup form, move fastest.

Learn more about the concrete fintech benefits for SMEs operating across borders and why platform selection matters as much as process design.

Explore Demivolt’s multi-account solutions for seamless business banking

You now have a complete picture of what the multi-account setup process actually requires: the right documents, the right entity treatment, API-driven account creation, and a verification and optimization discipline that keeps everything running cleanly at scale.

Demivolt is a regulated European fintech platform built specifically for this kind of operational need. The platform supports dedicated multi-currency IBAN accounts with local banking details, automated KYB onboarding, SEPA and SWIFT payment management, and role-based access for finance teams managing multiple accounts across entities. Setup is designed to be fast, transparent, and fully compliant with EU regulatory standards, with client funds held in segregated accounts. If you are an SME or digital-first business ready to put a compliant, efficient multi-account structure in place, Demivolt is built for exactly that.

Frequently asked questions

How long does the multi-account setup process usually take with compliant fintech platforms?

Most setups complete within 24 hours after successful KYB verification on API-driven platforms, though complex entities with layered ownership structures may require 10-15 business days for full verification.

What are common reasons for delays in the KYB process during multi-account setup?

The most frequent causes are stale documents over 3 months old, which trigger automatic rejection, and misclassifying sole proprietors or DBAs as legal entities, which adds 5-10 days to the review cycle.

Why is API integration important in multi-account setups for SMEs?

Manual KYB multiplies setup time by five compared to API-driven workflows, which automate account creation by specifying currency and country and return local banking details immediately after verification.

What documents are typically required for KYB verification?

KYB requires 3-5 core documents per entity, including Certificate of Incorporation, Memorandum or Articles of Association, and government-issued IDs for all ultimate beneficial owners, plus ongoing monitoring obligations post-approval.

Recommended

- Demivolt | Blog – How to manage multiple accounts: A step-by-step guide for SMEs

- Demivolt | Blog – Business account verification: compliance and efficiency for SMEs

- Demivolt | Blog – How to issue business cards for SMEs: a step-by-step guide

- Demivolt | Blog – Types of Business Bank Accounts: Find the Right Fit for Your SME