TL;DR:

- Traditional banks often reject SMEs due to vague compliance concerns and registration abroad.

- Digital providers like neobanks and EMIs enable rapid, online account opening within days.

- Proper documentation, sector compliance, and choosing the right provider increase approval chances.

Traditional banks turn away thousands of European SMEs every year, often citing vague compliance concerns or simply because the company is registered abroad. If you’ve spent weeks gathering paperwork only to receive a rejection letter, you’re not alone. The process of opening a business bank account in Europe has historically been slow, opaque, and frustrating, especially for companies with cross-border operations. This guide breaks down exactly what documents you need, how to choose between digital banks and EMIs, and how to complete the entire process online, often in just a few days.

Table of Contents

- What you need: Requirements for opening a business bank account in Europe

- Choosing the right digital provider: Banks, neobanks, and EMIs

- Step-by-step process: Opening your EU business bank account online

- Troubleshooting: Common issues and special cases

- A fresh perspective: Why digital solutions are winning for European SMEs

- Open your EU business account easily with Demivolt

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Prepare documents | Have your company papers and address proofs ready to prevent delays. |

| Choose digital-first providers | Neobanks and EMIs offer faster setup and better cross-border features than traditional banks. |

| Follow step-by-step process | Complete online forms, upload all required documents, and finish KYC checks for smooth activation. |

| Check for special risks | Non-residents and high-risk sectors should use specialist EMIs and expect extra compliance checks. |

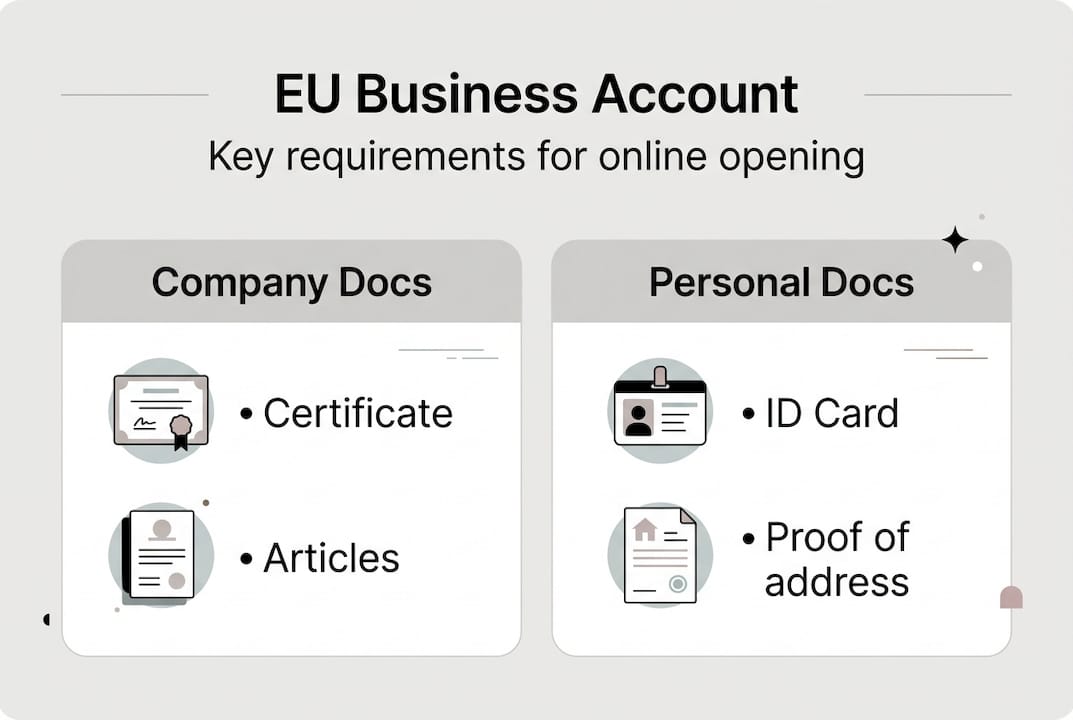

What you need: Requirements for opening a business bank account in Europe

Before you start any application, you need to know precisely what the provider expects. Missing even one document can push your timeline back by weeks. The good news is that digital providers have standardized this process significantly, so preparation is straightforward once you know the list.

The required documents for compliant opening include your company registration certificate, government-issued ID and proof of address for all directors and ultimate beneficial owners (UBOs) holding more than 25% of the company, proof of your business address and activity, a description of your business model, and documentation of your source of funds. Every person in a control position must be verified individually.

Here’s a quick overview of what each stakeholder typically needs to provide:

| Stakeholder | Required documents |

|---|---|

| Company | Registration certificate, articles of association, proof of address |

| Directors | Passport or national ID, proof of residential address |

| UBOs (>25%) | Passport or national ID, proof of residential address |

| Business activity | Invoices, contracts, website, or business plan |

| Source of funds | Bank statements, shareholder agreements, or audited accounts |

For non-EU or non-resident businesses, the bar is higher. Providers apply enhanced due diligence, meaning they may request additional layers of documentation such as certified translations, notarized copies, or a detailed explanation of why you need a European account. The non-resident account requirements vary by jurisdiction, but the principle is consistent: the less local presence you have, the more you need to prove legitimacy.

Compared to traditional banks, neobanks and digital providers accept a broader range of company types and process documents entirely online. Traditional banks often require in-person branch visits and may reject applications from foreign-registered entities outright.

Common mistakes that cause delays or rejections include:

- Submitting expired IDs or documents older than three months

- Providing a virtual office address without supporting activity evidence

- Leaving the business model description vague or generic

- Forgetting to include UBOs who hold indirect ownership stakes

- Submitting low-resolution scans that fail automated verification

A 36% rejection rate for foreign firms lacking proper preparation is a stark reminder that documentation quality matters enormously.

Pro Tip: Build a single shared folder with every document, organized by stakeholder. Label each file clearly (e.g., “Director_JohnSmith_Passport”). Providers that use automated document review will process clean, well-labeled files significantly faster than disorganized uploads.

Choosing the right digital provider: Banks, neobanks, and EMIs

Once you have all your documents ready, the next decision is choosing the right banking partner. Not every provider suits every business type, and picking the wrong one can mean restarting the process from scratch.

The three main options for European SMEs are traditional banks, neobanks, and Electronic Money Institutions (EMIs). Each has a different risk appetite, speed, and feature set.

| Provider type | Approval speed | Non-resident friendly | Monthly cost | SEPA/SWIFT |

|---|---|---|---|---|

| Traditional bank | 2 to 8 weeks | Low | Low to medium | Yes |

| Neobank (e.g., Qonto, Finom) | 24 hours to 3 days | Medium | Low | SEPA yes, SWIFT limited |

| EMI (e.g., Wise, Revolut) | 1 to 5 days | High | Low | Both |

Digital neobanks and EMIs like Revolut, Wise, Finom, and Qonto enable online EU business accounts in as little as 24 hours, providing EU IBANs for SEPA transfers and multi-currency support. This speed advantage is transformative for SMEs that need to start transacting immediately.

Traditional banks offer full services including lending and overdraft facilities, but they are notoriously slow, charge higher fees, and frequently reject non-resident applicants. If you don’t have a physical office in the country, your chances at a traditional bank drop sharply.

For opening accounts with digital banks, the process is entirely remote, which matters greatly for international founders. You don’t need to fly to Frankfurt or Amsterdam to open an account.

Key considerations when choosing:

- Residents vs. non-residents: EMIs are far more accessible for non-EU founders

- Transaction volume: Some neobanks cap monthly outgoing payments for new accounts

- Currency needs: If you transact in USD, GBP, or CHF regularly, multi-currency EMIs win

- Sector: High-risk industries (crypto, gaming) need specialized providers

Pro Tip: Lithuania-based EMIs, regulated by the Bank of Lithuania, are widely regarded as the most accessible option for non-EU companies. The regulatory framework there is pragmatic, and many providers have streamlined KYC processes specifically for international applicants. If you’re based outside the EU, start your search here.

For businesses in sensitive sectors, check the EMI solutions for non-residents before applying anywhere, since some providers will decline entire industries regardless of documentation quality.

Step-by-step process: Opening your EU business bank account online

You’ve settled on your provider. Now let’s walk through the end-to-end process so you know exactly what to expect at each stage.

The entire digital onboarding process is designed to be completed from your laptop or phone. Here’s how it works in practice:

- Choose your provider based on your company’s residency, sector, and transaction needs. Confirm they support your country of incorporation before proceeding.

- Register online using your business email and basic company details. Most platforms ask for your company name, registration number, and country of incorporation at this stage.

- Upload your documents through the provider’s secure portal or mobile app. Some platforms use live video verification for director identity checks. Have your document folder ready before you start.

- Complete KYC and AML checks. This is the KYC/AML requirements stage where the provider verifies identities, screens for politically exposed persons (PEPs), and reviews your source of funds. Be honest and thorough here. Inconsistencies are the top cause of delays.

- Receive your IBAN and activate features. Once approved, you’ll get your EU IBAN, which is immediately usable for SEPA transfers. You can then activate multi-currency wallets and order virtual or physical business cards.

The step-by-step process from sign-up to active account typically takes between one and three business days with most digital providers.

Stat callout: Digital sign-ups take just 10 to 15 minutes to complete. Most approvals arrive within 1 to 3 days for providers like Finom, Revolut, and Wise, compared to weeks with traditional banks.

Pro Tip: Do not start the application unless all directors and UBOs can complete identity verification within 48 hours. Many applications stall simply because one stakeholder is traveling or unavailable. Coordinate everyone before you click “submit.”

Troubleshooting: Common issues and special cases

Even with solid preparation, some businesses hit obstacles. Knowing the most common failure points in advance lets you navigate them without losing momentum.

The most frequent causes of rejection or delay include:

- Incomplete documentation: Missing UBO information or outdated proof of address

- Vague business activity: Descriptions like “consulting” or “trading” without specifics raise flags

- Virtual-only offices: Providers want evidence of real business activity, not just a registered address

- High-risk sector flags: Crypto, gaming, adult content, and gambling are blocked by many providers entirely

- Inconsistent information: Discrepancies between your application and public company records

For non-residents and non-EU founders, the numbers are stark. Non-EU companies face rejection rates of 7 to 36% at traditional banks, while specialized EMIs approve 70 to 90% of applicants when documentation is complete.

“EMI approval is 70 to 90%, versus 10 to 30% for traditional banks if you’re not EU-based.”

If your application is paused for additional information, respond quickly and thoroughly. Providers typically give a 5 to 10 business day window before closing the application. Treat every information request as a compliance conversation, not a bureaucratic hurdle. Explain your business clearly, attach supporting evidence, and avoid vague answers.

For high-risk sectors, the path forward is specialization. Some EMIs focus specifically on crypto businesses or regulated gaming operators. Check the EU account opening best practices for your sector before applying broadly, since a rejection from one provider can sometimes affect your standing with others.

The EMI approval rates for well-prepared applicants are dramatically higher than traditional banking alternatives, which is why most cross-border SMEs now default to digital-first providers.

A fresh perspective: Why digital solutions are winning for European SMEs

Here’s a view that most banking guides won’t give you: traditional banks are not a safe default. They feel safe because they’re familiar, but for the majority of European SMEs, they are actually the riskier choice.

80% of EU SMBs use digital banking monthly, and that number keeps climbing. This isn’t a trend driven by novelty. It’s driven by outcomes. Digital providers offer faster IBANs, lower fees, remote onboarding, and multi-currency support that traditional banks simply cannot match at the SME price point.

The contrarian insight here is about over-preparation. Most guides tell you to prepare your documents. We’d go further: over-prepare them. Write a two-page business model summary even if no one asks for it. Include a clear source-of-funds narrative even if the form only has a text box. Providers are making risk decisions, and every extra piece of credible information tips the scale in your favor. The businesses that get rejected are almost never rejected because of what they do. They’re rejected because the provider couldn’t understand what they do.

The one honest caveat: if your business needs credit facilities, overdrafts, or complex lending products, a traditional bank relationship still has value. But for payments, IBANs, and day-to-day cross-border operations, digital is not just faster. It’s better.

Open your EU business account easily with Demivolt

Ready to make your next move? Demivolt is built specifically for European SMEs that need a fast, compliant, and fully digital banking solution without the friction of traditional institutions.

With business banking with Demivolt, you get a dedicated EU IBAN, full SEPA and SWIFT payment support, multi-currency capabilities, and virtual and physical business cards, all managed through a single platform. Onboarding is transparent, secure, and designed to meet EU regulatory standards from day one. Whether you’re a resident EU company or an international SME expanding into European markets, Demivolt gives you the financial infrastructure to operate with confidence. Explore the platform and start your application today.

Frequently asked questions

What documents are needed to open a business bank account in Europe?

You’ll need a company registration certificate, IDs for all directors and UBOs holding more than 25%, proof of business address, and a clear description of your business activity and source of funds.

How quickly can I open a business account with a digital bank or EMI?

Most digital providers approve accounts within 24 hours to 3 days after all documents are submitted and verified, compared to several weeks with traditional banks.

Can non-EU or non-resident businesses open EU business accounts?

Yes, but you should expect enhanced compliance checks and higher rejection rates at traditional banks. Specialized EMIs for non-residents approve 70 to 90% of well-prepared applicants and are the recommended route.

What causes a business bank account application to be rejected?

The most common reasons are incomplete documentation, vague business descriptions, and operating in restricted sectors. A 36% rejection rate among unprepared foreign applicants shows how much preparation matters.