TL;DR:

- SEPA enables fast, safe, and low-cost euro payments across 41 European countries.

- It offers three main schemes: SCT for standard transfers, SCT Inst for real-time payments, and SDD for direct debits.

- Using SEPA strategically improves operational efficiency and cash flow management for European businesses.

Cross-border euro payments have a reputation for being slow, expensive, and bureaucratic. That reputation is outdated. SEPA makes cross-border payments as fast, safe, and efficient as domestic transfers across 41 countries and territories. For European business owners managing supplier payments, payroll, or customer collections across borders, this is a game changer. This guide breaks down exactly what SEPA is, how its payment schemes work, how it compares to SWIFT, and what compliance pitfalls to watch out for so you can use it with confidence.

Table of Contents

- What is SEPA and why was it created?

- How SEPA payment schemes work: SCT, SCT Inst, and SDD

- SEPA vs. SWIFT: Choosing the right system for your business

- SEPA compliance, risks, and common pitfalls for businesses

- A smarter approach: SEPA is more than just compliance

- Streamline cross-border business banking with Demivolt

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| SEPA streamlines euro payments | Businesses in 41 European countries can send and receive euro payments just like domestic transfers. |

| Three payment schemes | SEPA Credit Transfer, Instant Credit Transfer, and Direct Debit serve different business needs. |

| Compliance is critical | Proper mandate management and IBAN use are essential to avoid rejections and comply with requirements. |

| SEPA vs SWIFT | Use SEPA for euro-zone payments; SWIFT remains key for currencies or destinations outside SEPA. |

What is SEPA and why was it created?

SEPA stands for Single Euro Payments Area. It is a payment integration initiative that allows businesses and consumers to make cashless euro transactions across 41 European countries and territories using the same rules, standards, and processing times as a domestic payment. In practical terms, sending euros from a business account in Germany to a supplier in Portugal is no different from sending money to a supplier down the street.

SEPA is an initiative enabling cashless euro payments across 41 European countries and territories as fast, safe, and efficient as domestic payments. The area includes all 27 EU member states plus Iceland, Liechtenstein, Norway, Switzerland, the United Kingdom, Monaco, San Marino, Andorra, and Vatican City. This wide geographic reach means most European business relationships fall within the SEPA zone.

Before SEPA, cross-border euro payments were treated like international wire transfers: slow, expensive, and inconsistent. Banks applied different fees, used different formats, and had different processing timelines. The European Payments Council (EPC), working alongside EU regulators, created SEPA to eliminate that fragmentation.

Here is what SEPA standardizes:

- Payment formats: All transactions use ISO 20022 XML messaging standards

- Processing timelines: Consistent across all participating countries

- IBAN usage: One account number format works everywhere in the zone

- Fee structure: No distinction between domestic and cross-border euro fees

- Participant rules: All banks and payment institutions follow EPC rulebooks

“The goal was simple: make paying someone in another European country as easy as paying your local supplier.” This principle drives every SEPA rule and update.

For business owners, SEPA directly reduces the cost and friction of managing EU payment independence from card networks for euro transactions. If you are still using legacy international transfer methods for euro payments within Europe, you are likely paying more and waiting longer than necessary. Opening a business bank account online that is SEPA-enabled is the first practical step toward fixing that.

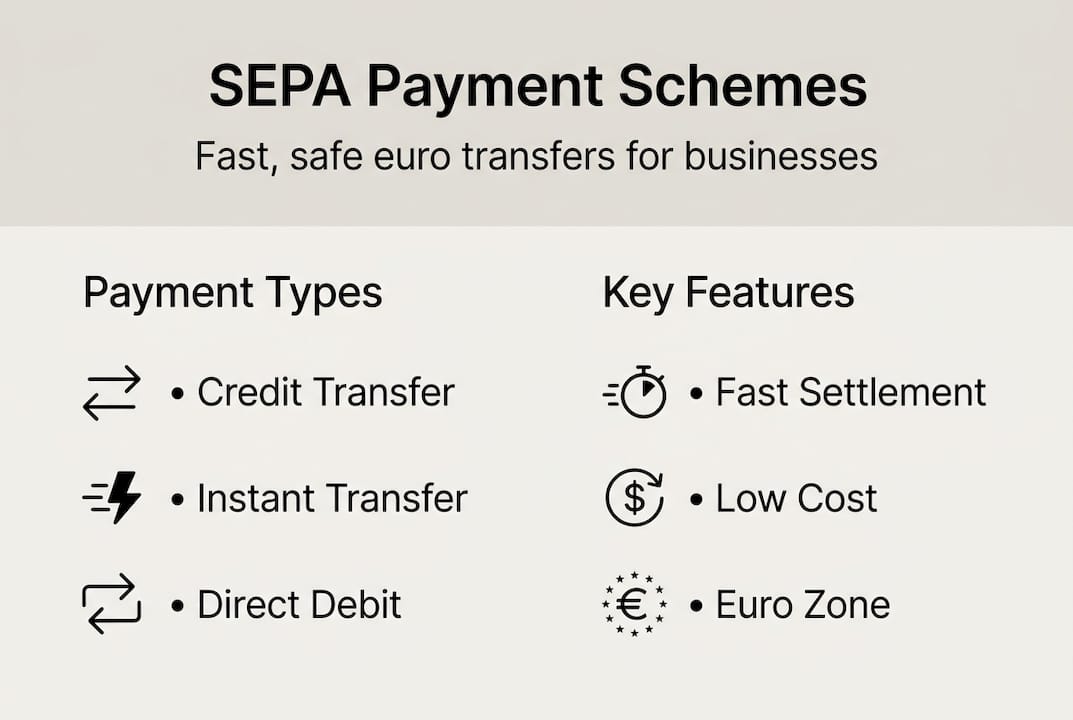

How SEPA payment schemes work: SCT, SCT Inst, and SDD

SEPA includes three main payment schemes: Credit Transfer, Instant Credit Transfer, and Direct Debit, each with distinct features designed for different business use cases.

SCT (SEPA Credit Transfer) is the standard push payment. Your business initiates a transfer from your account to a recipient’s IBAN. SCT processing uses IBAN only, with payments delivered in 1 business day. It is ideal for supplier invoices, payroll runs, and one-off payments where same-day settlement is not critical.

SCT Inst (SEPA Instant Credit Transfer) is the real-time version. Payments settle in under 10 seconds, 24 hours a day, 7 days a week, including weekends and public holidays. The current transaction limit is €100,000 per payment. This scheme is transforming how businesses handle urgent payments, cash flow gaps, and time-sensitive transactions.

SDD (SEPA Direct Debit) is a pull payment. Your business collects funds directly from a customer’s or partner’s account, but only after receiving a signed mandate authorizing the collection. SDD comes in two flavors: SDD Core (for consumers and businesses) and SDD B2B (business-to-business only, with stronger creditor protections).

| Scheme | Direction | Settlement | Best for |

|---|---|---|---|

| SCT | Push (you send) | D+1 business day | Invoices, payroll, supplier payments |

| SCT Inst | Push (you send) | Under 10 seconds | Urgent payments, 24/7 operations |

| SDD Core | Pull (you collect) | D+1 to D+2 | Subscriptions, utilities, consumer billing |

| SDD B2B | Pull (you collect) | D+1 | B2B recurring collections |

All three schemes rely on fintechs and SEPA efficiency to deliver faster, lower-cost processing than traditional banks typically offer. Smart businesses are also separating business finances from personal accounts to keep SEPA collections and transfers clean and auditable.

Pro Tip: If your business collects recurring payments from European customers, SDD B2B offers stronger protections than SDD Core because customers cannot dispute an authorized debit the way consumers can. Set it up correctly from the start and you will avoid most return payment headaches.

SEPA vs. SWIFT: Choosing the right system for your business

SEPA and SWIFT are not competitors in the traditional sense. They solve different problems. Knowing when to use each one saves your business time, money, and operational confusion.

SEPA is faster and cheaper than SWIFT for euro-zone transactions, using only IBAN and euro currency. SWIFT, on the other hand, is a global messaging network that supports dozens of currencies and connects banks worldwide. If you need to pay a supplier in Japan, the United States, or Brazil, SWIFT is your only option. If you are paying a supplier in France, the Netherlands, or Poland in euros, SEPA is almost always the better choice.

| Feature | SEPA | SWIFT |

|---|---|---|

| Coverage | 41 European countries | 200+ countries worldwide |

| Currencies | Euro only | Multi-currency |

| Speed | D+1 or under 10 seconds | 1 to 5 business days |

| Cost | Low to zero fees | Higher fees, correspondent charges |

| Identifier | IBAN only | IBAN + BIC/SWIFT code |

| Best use case | Euro payments within Europe | Global or non-euro transfers |

Here is where businesses commonly get this wrong:

- Sending euros to a SEPA-zone country via SWIFT instead of SCT, paying unnecessary fees

- Assuming SEPA works for non-euro currencies like Polish zloty or Danish krone (it does not)

- Using SWIFT for urgent euro transfers when SCT Inst would settle in seconds

- Not knowing their payment provider supports both systems, leading to manual workarounds

Understanding how SWIFT payments work alongside SEPA gives your business the full picture. The practical rule: default to SEPA for euro payments in Europe, and use SWIFT for everything else.

SEPA compliance, risks, and common pitfalls for businesses

SEPA’s ease of use can create a false sense of security. The system is well-designed, but it has strict rules. Businesses that ignore them face payment failures, delays, and in some cases, regulatory exposure.

SEPA payments are governed by EPC rulebooks and EU law, specifically the Payment Services Directive 2 (PSD2). Every participating institution must follow these rules, and your business is responsible for submitting correct, compliant payment instructions.

The most common pitfalls, in order of frequency:

- Wrong IBAN: A single incorrect digit causes an immediate reject. Always validate IBANs before processing batch payments.

- Missing or expired SDD mandate: Collecting funds without a valid, signed mandate is unauthorized and triggers returns.

- Insufficient funds: Payments return with reason code AM04. Build retry logic into your payment workflows.

- Incorrect creditor identifier: SDD requires a unique creditor ID. Using the wrong one invalidates the collection.

- Late mandate notification: SDD Core requires advance notice to debtors before collection. Missing this window gives customers grounds to dispute.

Businesses managing SDD collections should treat mandate administration as a core operational function, not an afterthought.

Edge cases matter here: rejects, returns, and recalls each have standardized reason codes (AM04 for insufficient funds, AC01 for invalid IBAN, MD01 for missing mandate). SDD refunds are possible up to 8 weeks after collection, or up to 13 months if the direct debit was unauthorized. That 13-month window is significant for businesses with high-volume consumer collections.

Pro Tip: Map every SEPA reason code to a specific internal action in your operations playbook. When AM04 fires, your team should automatically queue a retry. When MD01 fires, your team should contact the customer for a new mandate. Systematic responses reduce revenue leakage.

For SME banking compliance, staying current with EPC rulebook updates is non-negotiable. The EPC releases annual rulebook versions, and payment providers must certify compliance. Working with a regulated fintech that handles rulebook updates automatically removes that burden from your team.

A smarter approach: SEPA is more than just compliance

Most businesses treat SEPA as a box-checking exercise. Get the IBAN, set up the payment, move on. That mindset leaves real value on the table.

The businesses getting the most from SEPA are the ones using it as a foundation for operational efficiency. That means running payroll through SCT on a fixed schedule, automating supplier payments with batch SCT files, using SDD B2B for predictable B2B revenue collection, and leveraging SCT Inst for real-time treasury management between accounts.

When you layer automation on top of SEPA’s infrastructure, the compounding benefit is significant. Fewer manual payment errors. Lower processing costs. Faster cash flow cycles. Better reconciliation because every SEPA transaction carries structured remittance data.

The contrarian view here is that SEPA is not just a payment rail. It is a banking trends and SEPA enabler for digital transformation. Businesses that integrate SEPA deeply into their financial workflows, rather than treating it as a compliance obligation, consistently outperform those that do not. The infrastructure is there. The question is whether your business is using it strategically or just using it.

Streamline cross-border business banking with Demivolt

If SEPA is the infrastructure, the right banking partner is what makes it work smoothly for your business every day.

Business banking with Demivolt gives European businesses dedicated IBAN accounts, full SEPA and SWIFT payment capabilities, and automated payment workflows built for compliance from day one. Onboarding is fast, transparent, and designed for modern businesses that cannot afford weeks of back-and-forth with a traditional bank. Whether you are managing supplier payments across multiple SEPA countries, running recurring SDD collections, or need instant euro transfers for time-sensitive operations, Demivolt’s platform handles it in one place. Explore how Demivolt can simplify your cross-border payment operations today.

Frequently asked questions

What is a SEPA payment in simple terms?

A SEPA payment is a euro transfer between banks in 41 European countries, processed with the same speed and ease as a domestic payment.

How long does a SEPA payment take to complete?

SEPA Credit Transfers settle D+1, meaning the next business day, while Instant SEPA payments are completed in under 10 seconds around the clock.

What information do I need to send a SEPA payment?

IBAN only is used for SEPA Credit Transfers, so you need the recipient’s IBAN and their name to initiate the payment.

What are the main reasons a SEPA payment fails?

SEPA rejects and returns most commonly occur due to an invalid IBAN, insufficient funds in the sender’s account, or a missing or unauthorized direct debit mandate.

Is SEPA or SWIFT better for cross-border payments?

SEPA is faster and cheaper for euro payments within Europe, while SWIFT is the right choice for transfers involving other currencies or destinations outside the SEPA zone.

Recommended

- Demivolt | News – How fintechs facilitate cross-border payments for SMEs

- Demivolt | Blog – What is SWIFT payment? How it works for SMEs

- Demivolt | Blog – Business banking for SMEs: services, compliance & cross-border

- Demivolt | Blog – Open a business bank account online in Europe: step-by-step

- Moldova Joins SEPA in 2025: What It Means for Founders, Exporters, and Remote Businesses » Incorpore