TL;DR:

- Most businesses still assume international payments take days, but 75% of SWIFT gpi transfers now settle within 10 minutes. SWIFT operates a global messaging network connecting over 11,000 institutions, with transfer speed, cost, and compliance evolving significantly in 2026. Understanding the full process, costs, and recent innovations is essential for efficient and reliable cross-border payments.

Most businesses assume international payments take days, no exceptions. That assumption is now outdated. 75% of SWIFT gpi payments reach the beneficiary bank within 10 minutes. That is a dramatic shift from the “wait three to five business days” era many finance teams still budget for. Yet understanding what SWIFT transfers actually are, how they are processed, what they cost, and where they still fall short is essential before you wire your next cross-border payment. This guide covers all of it, with practical detail your finance team can use right now.

Table of Contents

- What is a SWIFT transfer?

- How the SWIFT transfer process works

- How fast are SWIFT transfers in 2026?

- How much do SWIFT transfers cost?

- Recent changes and common pitfalls with SWIFT in 2026

- A fresh perspective: what most businesses miss about SWIFT transfers

- Supercharge your cross-border payments with Demivolt

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| SWIFT’s global reach | SWIFT connects over 11,000 institutions, enabling secure international payments nearly everywhere. |

| Speed improvements | Modern SWIFT gpi can deliver funds within 10 minutes to 24 hours for most payments, but local delays may still occur. |

| Costs and transparency | Fees and FX markups can be 1–5% or more, so businesses should always check the potential charges and use modern tracking tools. |

| Recent upgrades | ISO 20022 is now the standard for cross-border SWIFT payments, enabling enhanced data and faster reconciliation. |

| Best practices | Accurate payment details and understanding of the process help avoid common SWIFT transfer issues for your business. |

What is a SWIFT transfer?

SWIFT stands for Society for Worldwide Interbank Financial Telecommunication. It is not a bank. It does not hold or move your money. Instead, it operates a secure global messaging network that allows financial institutions to communicate payment instructions to each other in a standardized format.

A SWIFT transfer is an international payment that uses this network, connecting over 11,000 institutions across 200+ countries, to securely transmit standardized payment instructions without moving funds itself. The actual movement of money happens through correspondent banking relationships, which we will cover shortly.

Here are the core terms you need to know before initiating any SWIFT payment:

- BIC/SWIFT code: An 8 or 11 character identifier assigned to each financial institution. It tells the network exactly which bank and branch should receive the payment instructions.

- IBAN: International Bank Account Number. This identifies the specific account at the receiving bank. Essential for European transfers and increasingly required globally.

- MT103: The standardized SWIFT message format used for single customer credit transfers. This is the electronic equivalent of a paper wire instruction, and it travels between banks on the SWIFT network.

- Correspondent bank: A third-party bank that holds accounts on behalf of other banks in foreign markets. These intermediaries make it possible to route funds between institutions that do not have a direct relationship.

A SWIFT code tells the network where to route the payment instruction. The IBAN tells it whom to pay. Without both, the payment will likely be delayed or rejected.

Understanding how SWIFT payment works at a structural level gives you a significant advantage when troubleshooting delays or comparing it to newer payment rails like SEPA or local real-time systems.

How the SWIFT transfer process works

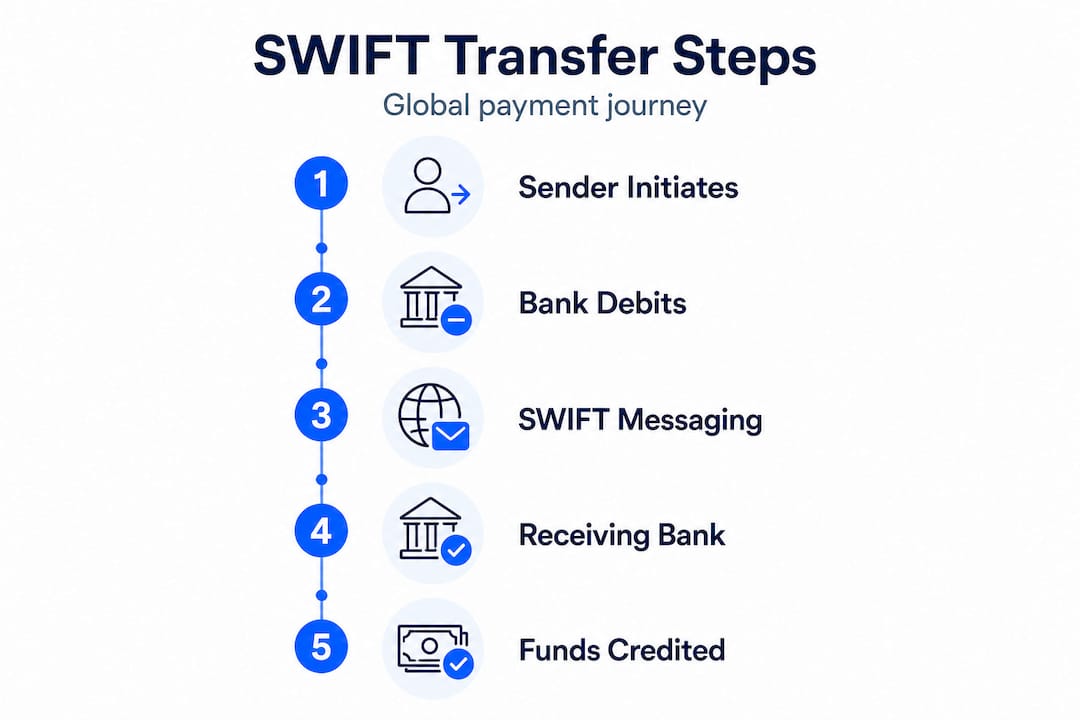

When you initiate a SWIFT transfer, a fairly precise sequence of events kicks off behind the scenes. Most businesses only see the “send” and “received” stages. Knowing what happens in between helps you anticipate problems before they become expensive ones.

- You submit the payment instruction. You provide your bank with the recipient’s SWIFT/BIC code, their IBAN or account number, the bank name and address, the transfer amount and currency, and any reference information.

- Your bank debits your account. The sending bank deducts the funds and generates a SWIFT message (typically an MT103 or, increasingly, an ISO 20022 MX message) with all payment details.

- The message travels through the network. If your bank and the recipient’s bank have a direct relationship (called a nostro/vostro account arrangement), the message travels directly. If not, it routes through one or more intermediary correspondent banks.

- Compliance and AML screening. At each stop, the receiving institution runs the payment through anti-money laundering (AML) and sanctions screening. Any mismatch or flag can trigger a hold.

- The recipient bank credits the account. Once the final bank receives the cleared instruction, it credits the beneficiary’s account. The entire cycle can take minutes or multiple business days depending on the route.

The process from initiation to credit involves the sender providing payment details, the sending bank debiting funds and transmitting a SWIFT message, funds being routed directly or through intermediaries, and the recipient bank crediting after compliance checks are complete.

Pro Tip: Always include a clean payment reference. Vague or missing references trigger manual reviews, which can add days to your settlement time and generate investigation fees on both ends.

Using dedicated IBAN accounts for international payments at your financial institution simplifies the first step considerably. When your account structure is already built for cross-border flows, initiating and reconciling SWIFT payments becomes far less manual.

How fast are SWIFT transfers in 2026?

Speed is where SWIFT’s reputation gets complicated. The traditional assumption of one to five business days is still technically possible, particularly on exotic currency corridors or when manual reviews are triggered. But for the majority of modern SWIFT transactions, that window has compressed significantly.

Traditional SWIFT transfers take 1 to 5 business days, while SWIFT gpi (global payments innovation) has transformed the picture: 75% of gpi-enabled payments reach the beneficiary bank within 10 minutes, and 90% settle within 24 hours when all parties are gpi members.

| Payment type | Typical settlement time | Tracking available? |

|---|---|---|

| Traditional SWIFT | 1 to 5 business days | No |

| SWIFT gpi | Under 10 min (75% of transfers) | Yes, end-to-end |

| SWIFT Go (low-value) | Minutes to hours | Yes |

| SEPA Credit Transfer | 1 business day (within EU) | Limited |

SWIFT gpi was introduced to solve the opacity and unpredictability that frustrated corporate treasurers for decades. It adds a Unique End-to-End Transaction Reference (UETR) to every payment, allowing both the sender and their bank to track exactly where funds are in the pipeline at any given moment.

That said, there are real-world factors that still slow things down:

- Local processing hours: Even if your SWIFT message arrives instantly, the recipient bank may only process incoming credits during specific business hours.

- Currency corridors: Payments to or from markets with limited correspondent banking infrastructure (certain parts of Africa, Southeast Asia, or Latin America) can take longer due to added routing hops.

- Holidays and weekends: Banks in the recipient country observe their own calendar. A payment sent Friday afternoon can sit until Monday or Tuesday in markets with extended weekend closures.

- Compliance holds: Any transaction that triggers an AML alert, no matter how routine your business, will pause settlement until the review is complete.

Pro Tip: Schedule high-value SWIFT payments early in the business week, early in the day (your recipient bank’s local time). This maximizes the chance that same-day processing handles the final credit step.

For a closer look at how to get faster SWIFT transfers for SMEs, the practical steps around bank selection, currency pairing, and payment formatting matter as much as the raw network speed.

How much do SWIFT transfers cost?

Cost is where SWIFT payments have the biggest variance, and where businesses most frequently underestimate their exposure. The sticker price your bank quotes is rarely the final cost.

Fixed fees typically run from $10 to $50 per transfer at both the sending and receiving ends, with intermediary banks also deducting their own fees in transit. FX markups add another 2% to 5% on top of that. The total effective cost can easily reach 1% to 5% or more of the transfer value, depending on the route, currency, and method chosen.

Here is how SWIFT transfer fees break down by type:

- Sender bank fee: Charged by your bank to process and transmit the payment instruction. Typically fixed regardless of amount.

- Intermediary/correspondent bank fee: Each hop in the chain may deduct a fee from the principal amount before passing it along. This is unpredictable unless your bank offers fee guarantees.

- Recipient bank fee: The beneficiary’s bank may charge a receiving fee, either fixed or percentage-based.

- FX conversion markup: If you are sending in a currency different from your account currency, your bank applies a spread over the mid-market rate. This is often the single largest cost and the least transparent.

The charge code you select affects how fees are distributed:

| Charge code | Who pays sender fees | Who pays intermediary fees | Who pays receiver fees |

|---|---|---|---|

| OUR | Sender | Sender | Sender |

| SHA | Sender | Shared/deducted | Recipient |

| BEN | Recipient | Recipient | Recipient |

OUR is often the best choice when you need the recipient to receive the exact amount you specify (such as paying a vendor invoice). SHA is the most common default and often results in the beneficiary receiving slightly less than expected.

Understanding these cross-border payment challenges before you build your payment workflows helps you price international business accurately and avoid shortfalls on vendor relationships.

Recent changes and common pitfalls with SWIFT in 2026

SWIFT is not standing still. The most significant infrastructure change in decades is now live, and it has direct implications for how your payments are processed and what data you need to include.

The ISO 20022 migration is mandatory. The transition to ISO 20022 MX messages became mandatory in November 2025. MT messages (the legacy format, including MT103) are being phased out in favor of MX messages, which carry significantly richer structured data. This means more precise remittance information, better reconciliation, and improved compliance screening. However, it also means that banks still running legacy systems may cause formatting mismatches that generate delays.

The practical result for your business: if your payment instructions contain incomplete or unstructured data, they are more likely to be flagged or held for manual review under the stricter ISO 20022 schema. Clean, complete data is no longer optional.

Common pitfalls to watch for in 2026:

- Incorrect or outdated BIC codes: Banks merge, rebrand, and reorganize. A BIC that worked six months ago may no longer route correctly.

- Missing or abbreviated beneficiary details: ISO 20022 requires structured address fields. Abbreviated or informal entries create processing exceptions.

- Compliance AML flags: Payments to certain sectors, countries, or with unusual reference patterns trigger automated holds that can take days to clear.

- Last-mile processing gaps: Even with gpi tracking, the final credit to the beneficiary’s account is often outside the SWIFT network and depends entirely on the recipient bank’s internal systems.

Exception messages via MT199 or camt.110 can take 10 to 30 days to resolve, and 2% to 5% of all SWIFT transfers require additional investigation. That is a meaningful risk for businesses with tight cash flow cycles or time-sensitive vendor payments.

Pro Tip: Build a buffer into payment schedules for first-time transfers to new counterparties or new jurisdictions. Compliance screening is more thorough on unfamiliar payment patterns, and that first transfer is most likely to attract additional scrutiny.

Review how ISO 20022 and IBAN standards interact to understand which account formats your platform needs to support. And if your business is scaling across borders, international payment compliance for SMEs is worth a close read for operational best practices.

A fresh perspective: what most businesses miss about SWIFT transfers

Here is what most SWIFT guides do not tell you: the system has improved dramatically, but the gap between what the network can theoretically do and what your specific payment corridor will actually experience remains wider than most businesses expect.

SWIFT gpi and ISO 20022 are genuine advances. But they do not eliminate the last-mile problem. Once the SWIFT message reaches the recipient bank, your payment enters that bank’s internal processing queue, which is fully outside SWIFT’s control. You can see the message was delivered via gpi tracking. What happens next is opaque.

The same applies to compliance delays. AML and sanctions screening are applied by each institution in the chain independently. A payment flagged at the correspondent bank level may sit for days without your bank even knowing why. You file an investigation request. The investigation takes time. Meanwhile, your supplier is waiting.

Many SMEs pivot to fintech solutions for cross-border payments to sidestep some of these pain points, and for many use cases that is a smart move. Lower FX markups, faster settlement on major corridors, and better user interfaces are real advantages. But those platforms are not universally suited to every payment type, jurisdiction, or compliance requirement. Use them where they are strongest, and know which corridors still require traditional SWIFT infrastructure.

The businesses that handle international payments best in 2026 are not chasing the fastest or cheapest option every time. They build a structured payment stack: the right tool for each corridor, with documented fallback procedures when exceptions hit. SWIFT is still the backbone for many of those corridors, even if it is no longer the only option.

Supercharge your cross-border payments with Demivolt

Navigating SWIFT fees, compliance holds, and ISO 20022 formatting requirements is complex enough without fighting your banking infrastructure on top of it.

Business banking with Demivolt gives SMEs a regulated, digital-first platform purpose-built for exactly this kind of operational complexity. You can open dedicated IBAN accounts, manage both SEPA and SWIFT payments from a single dashboard, and maintain full visibility over your cross-border payment flows without manual workarounds. Demivolt’s segregated account structure keeps your funds protected, while role-based user management lets your finance team operate with the right level of access at every step. If you are scaling across borders and need a banking partner that keeps up, Demivolt is built for that.

Frequently asked questions

What details do I need to make a SWIFT transfer?

You will need the recipient’s BIC/SWIFT code, IBAN or local account number, full recipient name and address, and the transfer amount with currency. Providing complete payment details upfront reduces the chance of compliance holds or routing errors.

How do SWIFT transfer costs compare to fintech solutions?

SWIFT transfers offer unmatched global reach but carry higher fixed and FX fees than most fintech alternatives. Per industry analysis of SWIFT gpi, SWIFT remains reliable for global coverage while fintech options can deliver lower costs on major corridors but may not serve all regions or meet every compliance requirement.

Can I track my SWIFT payment in real time?

Yes, if both banks in your transaction are SWIFT gpi members. SWIFT gpi provides real-time tracking and full transparency from initiation to credit, though coverage depends on your bank and the recipient bank both supporting the gpi standard.

What happens if a SWIFT transfer is delayed or rejected?

Delays most commonly result from AML screening, incorrect beneficiary details, intermediary bank holds, or local bank holidays. Investigations via MT199 or camt.110 can take 10 to 30 days to resolve, so build buffer time into any time-sensitive payment.

How has ISO 20022 impacted SWIFT transfers?

ISO 20022 enables richer structured data in payment messages, improving reconciliation and compliance screening across the network. The mandatory transition to MX messages from November 2025 means incomplete or legacy-formatted payment data is more likely to generate processing exceptions at modern banking institutions.

Recommended

- Demivolt | Blog – SWIFT payment guide: faster transfers for European SMEs

- Demivolt | Blog – What is SWIFT payment? How it works for SMEs

- Demivolt | Blog – IBAN Accounts Explained: Guide for SMEs Managing Cross-Border Payments

- Demivolt | Blog – SEPA payments explained: efficient euro transfers for EU businesses