TL;DR:

- Payment processors manage message flow between merchants, banks, and networks, enabling real-time authorization. Settlement of funds occurs days after authorization due to batching, clearing, and compliance checks, impacting cash flow. European SMEs must understand PSD2, SCA, and cross-border routing to optimize approval rates and reduce costs effectively.

Every time a customer clicks “pay,” most business owners assume the money is on its way. It isn’t. The role of payment processors is far more layered than routing a number from point A to point B. Payment processing connects issuing banks, acquiring banks, card networks, and payment providers into a single flow, yet authorization and actual fund transfer are separated by hours, sometimes days, and a chain of compliance checks. For European SMEs managing cross-border transactions, that gap between assumption and reality can create cash flow surprises, regulatory exposure, and unnecessary costs.

Table of Contents

- Understanding payment processors and their core function

- The payment lifecycle: authorization, capture, clearing, and settlement

- Navigating compliance: PSD2, strong customer authentication, and security requirements

- Optimizing payment processors for cross-border SME transactions

- Managing fees, cash flow, and reconciliation challenges for SMEs

- Why building payment processing know-how is a strategic advantage for European SMEs

- Explore Demivolt’s business banking solutions for streamlined payment processing

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Payment processors manage transaction flow | They route authorization requests quickly between merchants, card networks, and banks to approve or decline payments. |

| Authorization is not payment | Funds are only transferred after capture, clearing, and settlement, which can take one to three business days. |

| PSD2 enforces strong authentication | European regulations require two-factor authentication to reduce fraud and ensure secure electronic payments. |

| Smart routing improves cross-border payments | Using multi-acquirer and geo-based routing reduces declines, fees, and foreign exchange costs for SMEs. |

| Managing fees and settlement improves cash flow | Understanding fee layers and settlement timing helps SMEs avoid surprises and maintain healthy working capital. |

Understanding payment processors and their core function

Payment processors sit at the center of every card transaction, but their actual job is widely misunderstood. They are not simply pipes that move money. Their function is to manage the message flow between four parties: the merchant, the payment gateway, the card network (Visa, Mastercard), and the issuing bank. Every time a customer pays, the processor routes authorization requests in real time through card networks to the issuing bank, receives an approval or decline, and returns the result to the merchant, typically within two to three seconds.

It’s worth being precise about what a processor is not. A payment gateway is the front-end interface that encrypts and transmits the transaction data. An acquiring bank holds the merchant account. The processor is the engine in between, handling the technical orchestration and compliance messaging. Many SMEs conflate these roles, which leads to poor vendor selection and misplaced blame when transactions fail.

Here’s what payment processors actually handle on your behalf:

- Authorization routing: Sending transaction requests to the correct card network and issuing bank

- Real-time decisioning: Receiving and relaying approval or decline responses within seconds

- Fraud screening: Applying rule-based and machine learning checks before authorization

- Compliance messaging: Embedding PSD2 and 3DS2 authentication signals into transaction flows

- Fee calculation: Computing interchange, scheme fees, and processor markup per transaction

- Data formatting: Translating transaction data into formats each network and bank accepts

“The processor is the translator of the payment ecosystem, converting a merchant’s sale event into a precise, regulated message that banks can act on. Without it, every transaction would require direct negotiation between parties.”

Understanding these functions is the foundation for making informed decisions about your business payment solutions for SMEs. If you don’t know what your processor actually controls, you can’t evaluate whether they’re doing it well.

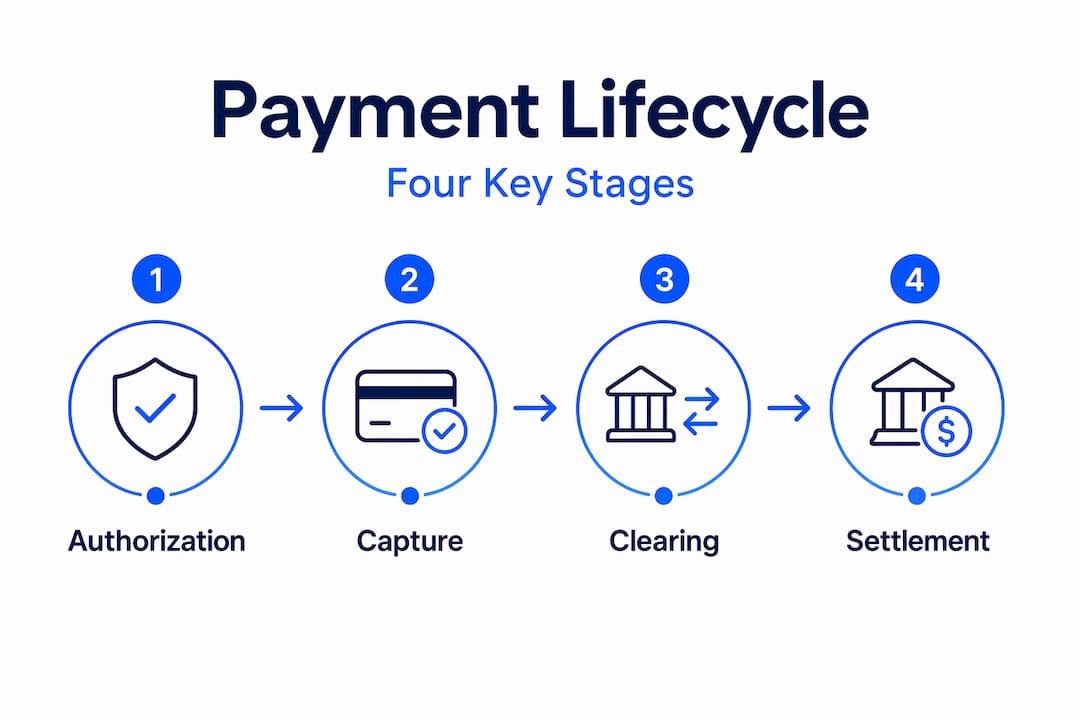

The payment lifecycle: authorization, capture, clearing, and settlement

Authorization is not payment. This is the single most important thing financial managers at European SMEs need to understand. When a customer’s card is authorized, funds are placed on hold on their account. Your merchant account has not received anything yet.

The lifecycle runs through four distinct stages:

- Authorization: The processor confirms the cardholder has sufficient funds or credit. A hold is placed. No money moves.

- Capture: You (or your system) request finalization of the authorized amount. This is usually batched at the end of each business day.

- Clearing: The card networks match transaction records between your acquiring bank and the customer’s issuing bank, validating amounts and merchant details.

- Settlement: Funds actually transfer between financial institutions. Settlement typically occurs 1 to 3 business days after authorization and capture.

The table below maps each stage to its average timing and the responsible party:

| Stage | What happens | Average timing | Responsible party |

|---|---|---|---|

| Authorization | Hold placed on cardholder funds | Seconds | Processor + issuing bank |

| Capture | Merchant finalizes transaction | Same day (batch) | Merchant + processor |

| Clearing | Records matched across networks | Same day or T+1 | Card networks |

| Settlement | Funds transferred to merchant | T+1 to T+3 | Acquiring bank |

One timing detail that catches SMEs off guard: authorization only places a hold, and funds move only after capture and batching. Most processors run a daily batch cutoff, typically before 10 PM local time. Miss that cutoff, and your settlement shifts by a full business day. For a business running thin margins on cross-border sales, that delay compounds across hundreds of transactions.

Pro Tip: Set your payment system’s auto-capture window well before your processor’s daily cutoff time. A buffer of two to three hours prevents end-of-day batch failures and keeps your settlement schedule predictable.

Navigating compliance: PSD2, strong customer authentication, and security requirements

European payment processors don’t just move money. They carry regulatory obligations that directly affect your approval rates, customer experience, and legal standing. The EU’s revised Payment Services Directive, known as PSD2, reshaped how processors authenticate transactions and share financial data.

The most operationally significant part of PSD2 is Strong Customer Authentication, or SCA. PSD2 mandates SCA using at least two of three factors for most electronic payments: something the customer knows (a PIN or password), something they possess (a phone or card reader), and something they are (a biometric like a fingerprint). Processors embed these requirements into their 3DS2 authentication flows automatically, but how well they do it varies significantly.

Key compliance realities for SMEs to understand:

- Exemptions exist but are not guaranteed: Low-value transactions under €30 and low-risk transactions based on fraud rate analysis may skip SCA, but your processor’s fraud tooling determines eligibility.

- Failed SCA flows hurt conversion: Non-optimized authentication flows can reduce approval rates by 10 to 20 percent, costing real revenue on cross-border sales.

- Open banking APIs improve the experience: PSD2 compliance is embedded in processors requiring SCA and open banking APIs, which when properly integrated, allow frictionless authentication without redirecting customers away from checkout.

“SCA is not just a compliance checkbox. It’s a conversion variable. A poorly implemented SCA flow at checkout costs European SMEs actual revenue on every declined or abandoned transaction.”

Pro Tip: Ask your processor for their SCA exemption rate and their 3DS2 fallback success rate by country. These two numbers tell you more about their compliance quality than any marketing material.

For a detailed breakdown of what regulatory compliance means for your payment operations, the compliance and cash flow checklist is worth reviewing before your next processor evaluation.

Optimizing payment processors for cross-border SME transactions

Cross-border payments are where the importance of payment processors becomes most visible, and where most SMEs leave money on the table. Every international transaction adds layers of cost and failure risk that domestic payments don’t carry.

Modern processors improve legacy rails using smart routing based on geography and card type, directing each transaction to the acquiring bank or processing path most likely to approve it. A German card paying on a French e-commerce site should route differently than a UK card doing the same. Processors with smart routing handle that automatically. Legacy processors treat every transaction identically and let failure rates climb.

Cross-border transactions add FX margins of 1 to 4 percent, which a multi-acquirer setup can significantly reduce by routing through local acquiring banks in the customer’s currency region.

Here’s how leading processors compare on the factors that matter most to cross-border SMEs:

| Feature | Modern processors (e.g., Adyen, Stripe) | Legacy processors |

|---|---|---|

| Smart routing | Geography and card type aware | Static routing |

| Multi-acquirer support | Yes, with local acquiring | Limited or single acquirer |

| PSD2/SCA integration | Built-in, auto-updated | Often manual or bolt-on |

| FX margin management | Local acquiring reduces exposure | High fixed FX fees |

| Real-time monitoring | Full transaction analytics | Basic reporting |

| Cost transparency | Itemized per-transaction | Bundled, opaque |

Strategies for reducing cross-border payment costs:

- Use local acquirers: Route transactions through banks in the customer’s country to reduce interchange and FX exposure

- Enable dynamic currency conversion selectively: Only offer DCC when your processor’s rate is genuinely competitive

- Monitor authorization rates by geography: A sudden dip in approvals from a specific country signals a routing or compliance issue, not a customer behavior shift

- Negotiate scheme fee caps: Large-volume SMEs often qualify for volume-based ceilings on Visa and Mastercard assessments

Pro Tip: Review your processor’s authorization rate by country every month. If any market drops below 85 percent approval, investigate routing configuration before assuming the problem is on the customer side.

For more on how fintechs are reshaping cross-border payment efficiency, read about fintech cross-border payment facilitation and how the fintech transformation of payments is creating new options for SMEs.

Managing fees, cash flow, and reconciliation challenges for SMEs

Even when everything works as expected, the fees embedded in payment processor services are layered enough to surprise most SME financial managers. Understanding the full fee stack is not optional if you’re managing margins across multiple European markets.

Settlement deducts interchange fees of 1 to 3 percent, processor markup of 0.2 to 0.5 percent, network assessments, and FX margins of 1 to 4 percent on cross-border transactions. By the time settlement hits your account, the difference between gross and net revenue can be substantial and hard to predict without proper reconciliation tooling.

The core fee components to track:

- Interchange fees: Paid to the issuing bank; vary by card type (consumer vs. commercial, debit vs. credit) and region

- Scheme fees: Paid to Visa or Mastercard for network access; tiered by volume

- Processor markup: Your processor’s margin; negotiable at scale

- FX margins: Applied on cross-currency settlements; can often be reduced via local acquiring

- Chargeback fees: Per-dispute fees that compound if fraud controls are weak

On the timing side, delayed captures and missed cutoff times push settlement to T+2 or beyond, which directly affects working capital. For SMEs running on 30 to 45 day payment terms with suppliers, a two-day settlement delay across high-volume sales periods is not trivial.

Reconciliation is where most SMEs lose visibility. Settlement reports from processors use different reference numbers than the transactions in your accounting system. Without a reconciliation layer, discrepancies pile up, and finding missing funds becomes a manual forensics exercise.

Pro Tip: Use a payment orchestration platform or accounting integration that maps processor settlement reports directly to invoice and order references. The upfront setup cost is recovered within months in reduced reconciliation labor and fewer disputes.

For a full breakdown of how SMEs can improve payment efficiency and cash flow, review the guide on international payments efficiency for SMEs.

Why building payment processing know-how is a strategic advantage for European SMEs

Most SMEs treat payment processing as infrastructure. Set it up once, pay the fees, and move on. That mindset is exactly why so many businesses bleed margin on cross-border sales without knowing where it goes.

The gap between authorization and settlement is not just a technical footnote. It’s a cash flow planning variable. SMEs that confuse the two routinely overestimate their available working capital by several days’ worth of revenue. When payroll or supplier payments fall in that window, the consequences are real.

Multi-processor routing is not a feature reserved for enterprise merchants. Any European SME processing above a modest monthly threshold can negotiate multi-acquirer access, and the approval rate improvements on cross-border transactions more than justify the setup complexity. Ignoring this because it sounds technical is leaving money on the table.

Regulatory compliance through PSD2 and SCA is embedded in processor platforms, but that doesn’t mean SMEs can be passive. Processors update their SCA exemption logic, fraud scoring rules, and routing configurations regularly. An SME that doesn’t periodically review its checkout authentication flow may unknowingly operate on deprecated settings that reduce approval rates or introduce compliance gaps.

Active engagement with your payment processing infrastructure is a business decision, not a technical one. The SMEs that understand their processor’s fee stack, know their settlement schedule, and monitor their authorization rates by market are the ones that forecast revenues accurately and catch problems before they affect liquidity.

For a deeper look at the business payment solutions insights that support this kind of operational clarity, the details are worth the read.

Explore Demivolt’s business banking solutions for streamlined payment processing

Understanding payment processor mechanics is the first step. Having the right financial infrastructure behind your operations is what turns that knowledge into results.

Demivolt’s business banking solutions are built specifically for European SMEs navigating the complexity of cross-border payments. The platform embeds PSD2 compliance, supports multi-account structures with dedicated IBANs, and provides transparent fee reporting so you can reconcile settlements without the guesswork. SEPA and SWIFT payment management, role-based user access, and real-time transaction visibility give your finance team the control they need across markets. If cross-border payment efficiency and regulatory clarity matter to your business, Demivolt is worth a conversation.

Frequently asked questions

What exactly does a payment processor do in a transaction?

A payment processor routes authorization requests in real time between merchants, card networks, and issuing banks, managing the message flow that results in an approval or decline within seconds.

How long does it take for funds to settle after payment authorization?

Settlement typically occurs 1 to 3 business days after authorization and capture, as transactions go through batching and clearing before funds physically transfer between financial institutions.

What is Strong Customer Authentication (SCA) under PSD2?

PSD2 mandates SCA using at least two factors, combining something the customer knows, possesses, or is, to secure most electronic payments across Europe and reduce fraud.

How can SMEs reduce costs on cross-border payments?

Using processors with multi-acquirer routing lets SMEs mitigate FX margins via local acquiring, reducing the 1 to 4 percent foreign exchange cost that cross-border transactions typically carry.

Why do authorization and settlement dates often differ?

Authorization places a hold only, while settlement requires batching, network clearing, and interbank fund transfers, all of which happen after the initial authorization event and on different timelines.