Summary

The Best High-Risk Payment Gateway in 2026: Why Merchants in Restricted Industries Are Switching to Crypto Settlement

Share Share Share Share Email The Best High-Risk Payment Gateway in 2026: Why Merchants in Restricted Industries Are Switching to Crypto Settlement By Connor Reid · Independent Payments & Risk Infrastructure Analyst · March 2026 If you operate in a high-risk industry, you already know the drill.

You apply for a payment processor. You fill out extensive paperwork — business registration, processing history, bank statements, a “narrative” explaining your business model. You wait days or weeks. Then one of three things happens: you’re rejected outright, you’re approved with a 10% rolling reserve and fees north of 5%, or you’re approved at reasonable terms that get yanked six months later when the processor’s risk department “re-evaluates” your category.

High-risk merchants — peptide suppliers, nutraceutical brands, online casinos, adult platforms, CBD companies, SaaS tools for crypto, sports betting operators, dating sites, e-cigarette retailers, supplement companies, nootropic vendors, and dozens of other legitimate businesses — have been treated as second-class citizens by the payment processing industry for over a decade.

The standard high-risk payment gateway model works like this: a specialized processor agrees to work with you (because mainstream processors won’t), charges you 4–8% per transaction (because they can), holds 5–10% of your revenue in a rolling reserve for 6–12 months (because they’re “managing risk”), and reserves the right to freeze your account at any time if chargeback rates exceed an arbitrary threshold.

This model is extractive. And in 2026, it’s no longer the only option. Why High-Risk Merchants Get Punished The payment processing industry classifies businesses as “high risk” based on factors that often have nothing to do with the individual merchant’s actual risk profile: Industry category.

If your business falls into a Merchant Category Code (MCC) that Visa or Mastercard flags as elevated risk — which includes supplements, nutraceuticals, peptides, adult content, gambling, CBD, vaping, travel, telehealth, debt consolidation, firearms, and dozens more — you’re automatically high-risk regardless of your actual chargeback history.

Chargeback potential. Some industries have historically higher chargeback rates. But “historically higher” means the industry average might be 1.5% instead of 0.5% — which is enough for mainstream processors to refuse the entire category, punishing the 95% of merchants with low chargebacks because of the 5% who don’t manage their businesses well.

Regulatory ambiguity. Peptides, CBD, kratom, and certain supplements occupy legal grey zones in some jurisdictions. Processors don’t want to adjudicate legality, so they refuse the entire category. Reputational risk. Banks and processors worry about being associated with industries that attract public scrutiny — even when those industries are perfectly legal.

Adult content, gambling, and cannabis-adjacent businesses suffer from this regardless of their compliance record. The result: legitimate, law-abiding businesses with clean chargeback histories pay 2–3x the transaction fees, surrender 5–10% of revenue to rolling reserves, and live under constant threat of account termination.

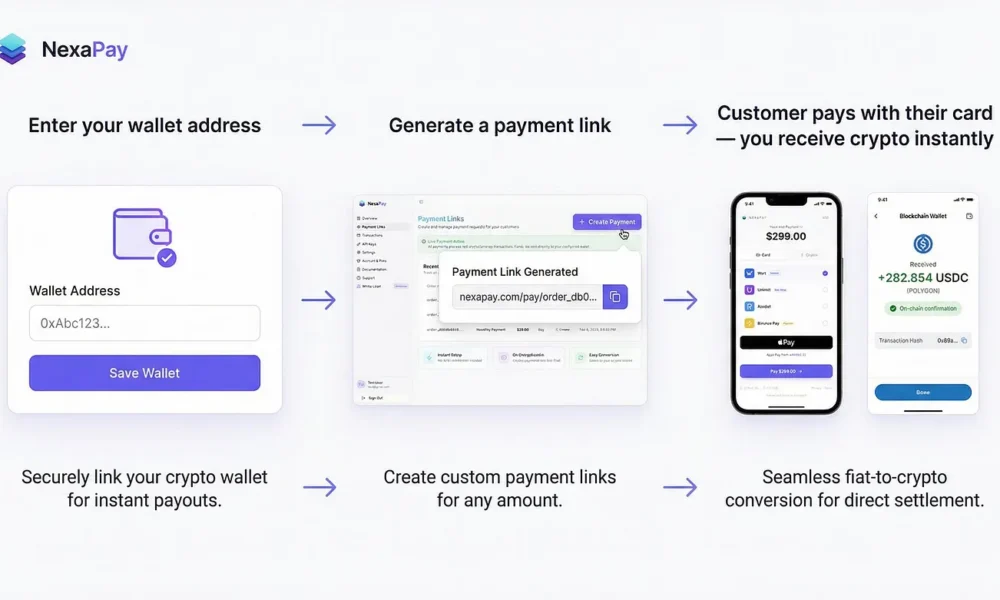

The Crypto Settlement Alternative Here’s what changes when a high-risk merchant switches from traditional processing to a fiat-to-crypto payment gateway: No rolling reserves. The payment settles directly to the merchant’s crypto wallet. There is no intermediary holding a percentage of your revenue for 6–12 months.

Source

Original coverage by TechBullion.

Use the button below to read the article on the publisher website.

Read on TechBullionRelated to this article