Summary

White-Label Payment Gateway in 2026: How to Launch Your Own Branded Fiat-to-Crypto Payment Gateway With USDT and USDC Settlement — Without Building Any Infrastructure

Share Share Share Share Email White-Label Payment Gateway in 2026: How to Launch Your Own Branded Fiat-to-Crypto Payment Gateway With USDT and USDC Settlement — Without Building Any Infrastructure By Sebastian Cole · Independent Payment Infrastructure & SaaS Analyst · April 2026 · 16 min read What if you could launch your own payment gateway — with your brand, your domain, your pricing — and start earning revenue on every transaction, without building a single line of payment infrastructure?

Not a reseller program where you send merchants to someone else’s checkout. Not an affiliate deal where you earn a referral fee. A fully branded payment gateway that operates under your name, on your domain, with your logo, your fee structure, and your merchant relationships — powered on the backend by infrastructure that’s already built, already tested, and already processing real transactions for thousands of merchants worldwide.

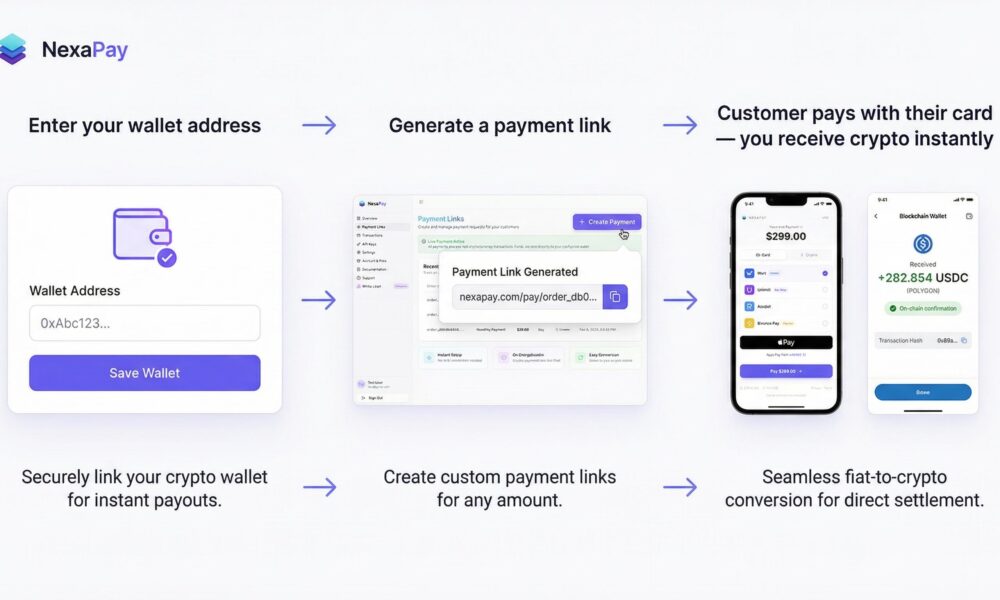

This is what a white-label payment gateway is. And in 2026, the most innovative version of this model is the white-label fiat-to-cryptocurrency gateway — where your merchants accept Visa, Mastercard, Apple Pay, and Google Pay from their customers, and receive settlement in USDC, USDT, Bitcoin, or other cryptocurrencies.

One company has built this model more completely than anyone else: NexaPay.one. And the opportunity it represents — for payment entrepreneurs, fintech startups, PSPs, ISOs, and financial services companies — is unlike anything the industry has seen. What a White-Label Payment Gateway Actually Is A white-label payment gateway is a fully operational payment platform that you license from a provider and rebrand as your own.

The provider handles everything on the backend — card processing, fraud detection, conversion, settlement, compliance, server infrastructure, uptime — and you handle everything on the frontend: your brand name, your domain, your merchant relationships, your pricing, your support. Your merchants never see the underlying provider.

They see your brand. Your checkout page. Your dashboard. Your logo. As far as they’re concerned, you are the payment gateway. The economics work like this: The provider charges a base processing rate (e.g., 1–3%) You set your own merchant-facing rate (e.g., 3–5%) You keep the difference on every transaction The more merchants you onboard and the more volume they process, the more you earn This is how every major payment company started: by building on top of existing infrastructure and layering their own brand, pricing, and distribution on top.

Why the Fiat-to-Crypto White-Label Model Is Different — And Better Traditional white-label payment gateways exist. They’ve been around for over a decade. Payment facilitators, ISOs, and resellers license processing capability from acquiring banks and offer it under their own brand.

But the traditional model comes with traditional problems: Acquiring bank dependency. You need a relationship with an acquiring bank willing to underwrite your merchants. These relationships are hard to get, expensive to maintain, and fragile — the bank can change terms or exit categories at any time.

MCC restrictions. The acquiring bank dictates which merchant categories you can serve. If the bank won’t underwrite gambling, adult content, CBD, or peptides, you can’t serve those merchants — even if the demand is enormous. Rolling reserves and fund freezes. The traditional model requires holding merchant funds, which creates the need for reserves and the risk of freezes.

These become your problem — you’re the one your merchants call when their money is frozen. Heavy compliance burden. KYC/AML, PCI DSS, state-by-state money transmission licensing (in the U.S.), European payment institution registration. The compliance overhead of running a traditional payment gateway costs hundreds of thousands of dollars annually.

Source

Original coverage by TechBullion.

Use the button below to read the article on the publisher website.

Read on TechBullion