TL;DR:

- Europe’s fintech sector, with approximately 10,000 companies, is the world’s second-largest ecosystem behind North America, driven by significant market value and growth. The regulatory environment, including the upcoming enforcement of the Single Rulebook starting in 2026, acts as a competitive filter and moat, favoring well-compliant firms. Despite strong early-stage funding, Europe faces a structural funding gap at scale, heavily relying on US investors for late-stage growth.

Europe’s fintech sector is far larger than most business professionals realize. The eu fintech landscape explained in concrete terms looks like this: approximately 10,000 companies operating across the continent, making Europe the world’s second-largest fintech ecosystem behind North America. That scale demands serious attention from investors and operators alike. This article breaks down the market size, regulatory architecture, emerging business models, and funding dynamics shaping European financial technology today — giving you a clear map of where the opportunities and risks actually sit.

Table of Contents

- Key Takeaways

- Current size and structure of the EU fintech market

- The regulatory framework shaping EU fintech

- Emerging business models and technology trends

- Investment dynamics and the funding gap

- My read on where European fintech is actually headed

- How Demivolt supports businesses in the EU fintech environment

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Market scale is significant | The EU fintech market is valued at $85.52 billion in 2025, on track to nearly double by 2031. |

| Regulations are tightening | The Single Rulebook (MiCA, DORA, PSD3, AI Act) shifts from guidance to strict enforcement starting 2026. |

| Funding is geographically concentrated | The UK captures over 50% of EU fintech funding; Germany and France follow at a distance. |

| Embedded finance leads innovation | Fintechs are moving beyond banking apps to become financial operating systems for SMEs. |

| Domestic capital remains scarce | European pension funds invest less than 0.02% in venture capital, creating reliance on US investors. |

Current size and structure of the EU fintech market

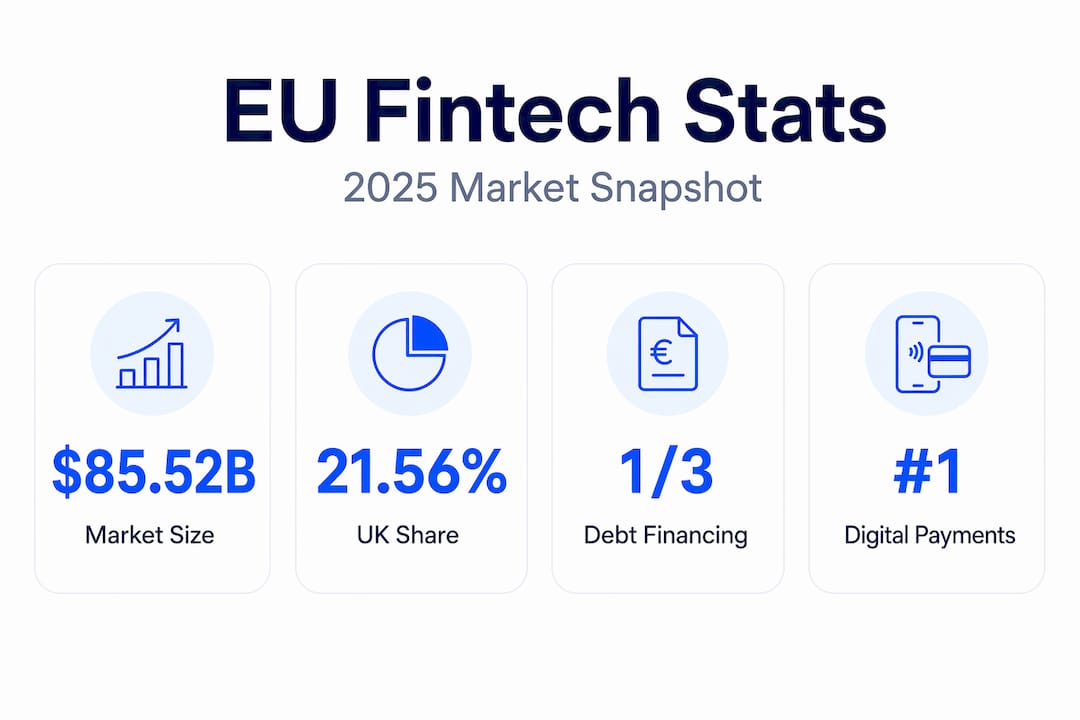

The numbers tell a story that outpaces most investor expectations. The European fintech market was valued at $85.52 billion in 2025 and is projected to reach $195.35 billion by 2031, growing at a CAGR of 14.76%. That growth rate is not driven by hype. It reflects genuine adoption across digital payments, lending infrastructure, and compliance technology.

Digital payments remain the dominant segment, accounting for the largest share of transaction volume across the continent. Insurtech has emerged as a high-growth vertical, with established carriers partnering with tech-native startups to modernize underwriting and claims processing. Neobanking, once the poster child of European fintech, has matured into a more competitive and margin-conscious space where differentiation now requires more than a well-designed mobile app.

Regionally, the picture is uneven. The UK holds 21.56% market share and continues to lead on open banking adoption. The Nordics are the fastest-growing region, projected at 16.17% CAGR, driven by high digital infrastructure penetration and strong government support for cashless payments. Southern Europe is earlier in its adoption curve but growing steadily, particularly in Spain and Portugal where digital payment infrastructure has expanded rapidly.

| Country/Region | 2025 Funding | Market Share / CAGR | Key Segment |

|---|---|---|---|

| UK | €6.1B+ | 21.56% market share | Open banking, neobanking |

| Germany | ~€1.5B | Significant | B2B payments, compliance tech |

| France | ~€1B | Growing | Insurtech, digital lending |

| Nordics | N/A | 16.17% CAGR | Payments, embedded finance |

| Southern Europe | Emerging | Accelerating | Digital payments |

Market fragmentation remains a defining feature of the European fintech ecosystem. Unlike the US, where a single regulatory framework and currency create a unified home market, EU fintechs must navigate 27 member states with differing consumer behaviors, languages, and legacy banking relationships. Consolidation is accelerating, but the majority of Europe’s 10,000 fintech companies still operate within one or two national markets.

The regulatory framework shaping EU fintech

If there is one thing that defines the fintech ecosystem in Europe relative to every other major market, it is the depth and coordination of its regulatory architecture. The EU has assembled what analysts are now calling the Single Rulebook. This is not a single piece of legislation but a coordinated stack of regulations that collectively govern how fintech companies must operate.

The five pillars are:

- MiCA (Markets in Crypto-Assets Regulation): Governs the issuance and trading of crypto assets, creating a licensing regime that applies across all EU member states.

- DORA (Digital Operational Resilience Act): Mandates specific cybersecurity and IT risk standards for financial entities, including fintechs.

- AI Act: Sets rules on how artificial intelligence can be deployed in regulated financial services contexts.

- PSD3 (Payment Services Directive 3): Extends and tightens the open banking framework, adding stronger consumer protections and clearer licensing requirements.

- AMLA (Anti-Money Laundering Authority): A new EU-level body that centralizes AML supervision, replacing the patchwork of national enforcement that allowed regulatory arbitrage.

The Single Rulebook’s enforcement phase begins in 2026, marking a clear shift from a period of regulatory guidance to one of strict supervision. Companies that treated compliance as a backlog item are now facing real deadline pressure. MiCA alone has already prompted dozens of crypto firms to seek EU licenses or exit the market.

This approach is deliberately different from the deregulatory posture the US has taken in recent cycles. EU regulators prioritize harmonization and competitiveness rather than reducing barriers. The result is a high-entry-cost environment that rewards well-capitalized, operationally mature businesses and penalizes underprepared entrants.

Pro Tip: If you are evaluating a European fintech for investment, treat regulatory compliance readiness as a primary due diligence criterion. A company that has already achieved MiCA or DORA compliance holds a structural advantage over competitors that have not. That lead is expensive and slow for a competitor to replicate, which makes it a genuine moat.

For a detailed breakdown of the compliance requirements relevant to financial professionals, the EU banking regulations guide from Demivolt covers the key obligations in practical terms.

Emerging business models and technology trends

The second wave of European fintech is defined by a shift in ambition. The first wave was about building better consumer interfaces on top of legacy banking rails. The current wave is about replacing the rails. Fintech is transitioning into a financial operating system embedded directly into SME business workflows, connecting cashflow management, accounts payable, invoicing, and credit in a single environment.

This matters for investors because the business model economics are fundamentally different. Embedded finance layers generate revenue through transaction volume, interchange, and lending margins rather than subscription fees or interchange alone. The monetization paths are more durable, and the switching costs are higher once a business integrates its financial operations into a single platform.

Several specific trends are reshaping the European financial technology landscape:

- AI for credit and risk: Lenders are deploying machine learning models for underwriting that outperform traditional credit scoring, particularly for SMEs with limited credit history but rich transactional data.

- Fintech-bank partnerships: Legacy banks need over €100 million budgets to build modern technology stacks from scratch. Most cannot or will not. Instead, they are partnering with fintechs to deliver capabilities they cannot build internally, which creates significant B2B revenue opportunities for well-positioned fintech platforms.

- Compliance technology: DORA and AMLA have created direct demand for RegTech tools. This is one of the few fintech verticals where European providers have a home-field advantage because they understand the specific regulatory requirements in ways that US or Asian tools do not.

- Cross-border payment infrastructure: SEPA Instant and the expansion of international payment corridors are creating new opportunities for platforms that can handle multi-currency, multi-jurisdiction transactions efficiently.

Understanding how these models serve SMEs specifically is worth studying closely. Fintech benefits for European SMEs are increasingly tied to operational integration rather than cost savings alone.

Pro Tip: When analyzing fintech business models in Europe, look for platforms that have moved beyond single-product positioning. A company that connects banking, invoicing, and payables in a unified workflow has fundamentally higher retention than one that only offers a digital account. That integration density is what separates the next generation of winners from the first.

Investment dynamics and the funding gap

The funding picture for European fintech in 2025 contains both encouraging and structurally concerning data. Total investment remained strong, but its distribution reveals a concentration problem that affects long-term market development.

The UK raised over €6.1 billion in fintech funding in 2025, representing more than half of all European fintech capital. Germany attracted approximately €1.5 billion, and France approximately €1 billion. Everything else, including the high-growth Nordic markets and the emerging Southern European sector, shared the remainder. For context on the UK’s sustained position, the UK fintech market dynamics reflect structural advantages that are difficult for other European markets to replicate quickly.

Debt financing accounted for nearly one-third of total fintech funding in 2025. That figure signals real maturity. Companies in lending and embedded finance are accessing debt capital to fund loan books rather than issuing equity, which is exactly what you would expect from a scaling financial business rather than a growth-stage tech startup.

The structural problem sits at the growth-stage level. European fintechs consistently perform well in seed and Series A rounds, where domestic angel networks and early-stage VCs are active. The capital gap opens at Series B and beyond, where large rounds require institutional investors with deep pockets. European pension funds invest less than 0.02% of assets into venture and growth capital. In the US, that figure is 1.9%. That is not a marginal difference. It is a structural deficit that pushes European fintech companies to rely on US investors for late-stage financing.

| Metric | Europe | United States |

|---|---|---|

| Pension fund VC allocation | Less than 0.02% | ~1.9% |

| Top fintech funding city | London (€6.1B+) | New York / San Francisco |

| Regulatory environment | Harmonized, strict | Fragmented, deregulating |

| Embedded finance maturity | Accelerating | More advanced |

| Debt financing share (2025) | ~33% of total funding | Comparable at scale |

Policy initiatives are emerging to address this. The EU’s Capital Markets Union agenda and individual member state programs are pushing pension funds and sovereign wealth vehicles to allocate more capital to domestic growth companies. Progress is slow, but the direction is clear. For investors, this gap also represents an opportunity. European fintechs excel at early-stage rounds but struggle at scale, meaning growth-stage capital commands favorable terms relative to equivalent deals in the US.

My read on where European fintech is actually headed

I’ve spent considerable time analyzing where the fintech ecosystem in Europe creates real, durable value versus where it produces noise. My honest take is that the regulatory tightening everyone is worried about is also the single biggest competitive filter the market has ever seen.

The companies that navigate the Single Rulebook successfully will not just survive. They will own defensible positions that late entrants cannot easily attack. Compliance as a moat is underappreciated in standard investment frameworks because it does not show up in the typical metrics investors track.

What I find structurally undervalued is the partnership layer between fintechs and incumbent banks. Most investors still analyze these as competing categories. They are not. The future of European financial infrastructure is collaborative, with fintechs providing the technology backbone and banks providing balance sheet, distribution, and licensing credibility. The companies building in that intersection are the ones I watch most closely.

The domestic funding gap is real and worth being honest about. Europe’s dependence on US capital for late-stage rounds creates a sovereignty paradox: the continent with the most carefully constructed regulatory framework for financial innovation is partially owned by investors operating under a different regulatory philosophy entirely. That tension will define the next decade.

— dd

How Demivolt supports businesses in the EU fintech environment

Operating within the European financial technology environment requires more than understanding the trends. It requires infrastructure that keeps up with them. Demivolt provides regulated business banking built specifically for companies operating in or expanding across Europe. From dedicated IBAN accounts and SEPA and SWIFT payment management to virtual and physical business cards, Demivolt gives businesses the financial control and compliance readiness the EU regulatory environment now demands. Multi-account structures, role-based access, and segregated client funds mean you are not just banking. You are operating with the kind of financial discipline that regulators and investors expect. Explore business banking solutions that are built for how modern companies actually work.

FAQ

What is the EU fintech market worth in 2025?

The European fintech market is valued at $85.52 billion in 2025 and is projected to reach $195.35 billion by 2031, growing at a CAGR of 14.76%.

Which country leads EU fintech funding?

The UK leads significantly, raising over €6.1 billion in 2025. That represents more than 50% of total EU fintech funding, with Germany and France as the next largest recipients.

What is the EU Single Rulebook for fintech?

The Single Rulebook is a coordinated set of regulations including MiCA, DORA, the AI Act, PSD3, and AMLA. It creates a unified compliance framework across EU member states, with enforcement intensifying from 2026 onward.

Why is embedded finance important for EU fintech investors?

Embedded finance integrates banking, payments, and credit directly into SME business workflows, creating higher customer retention and more durable revenue streams than standalone banking apps. It represents the primary growth vector for next-generation European fintech platforms.

What is the main funding challenge for European fintechs?

European fintechs struggle to raise large growth-stage rounds domestically. European pension funds invest less than 0.02% of assets in venture capital compared to 1.9% in the US, creating a structural reliance on US investors for late-stage financing.