Managing international payments, multi-currency accounts, and team expense controls through legacy business banking providers often creates delays and manual work for finance teams. Traditional banks and payment platforms either impose slow onboarding, opaque fee structures, or limited integration options with accounting tools and global rails. This comparison outlines the pricing, account features, and automation capabilities of five business banking and payments services so you can select the platform that best matches your cross-border workflows and growth plans.

Table of Contents

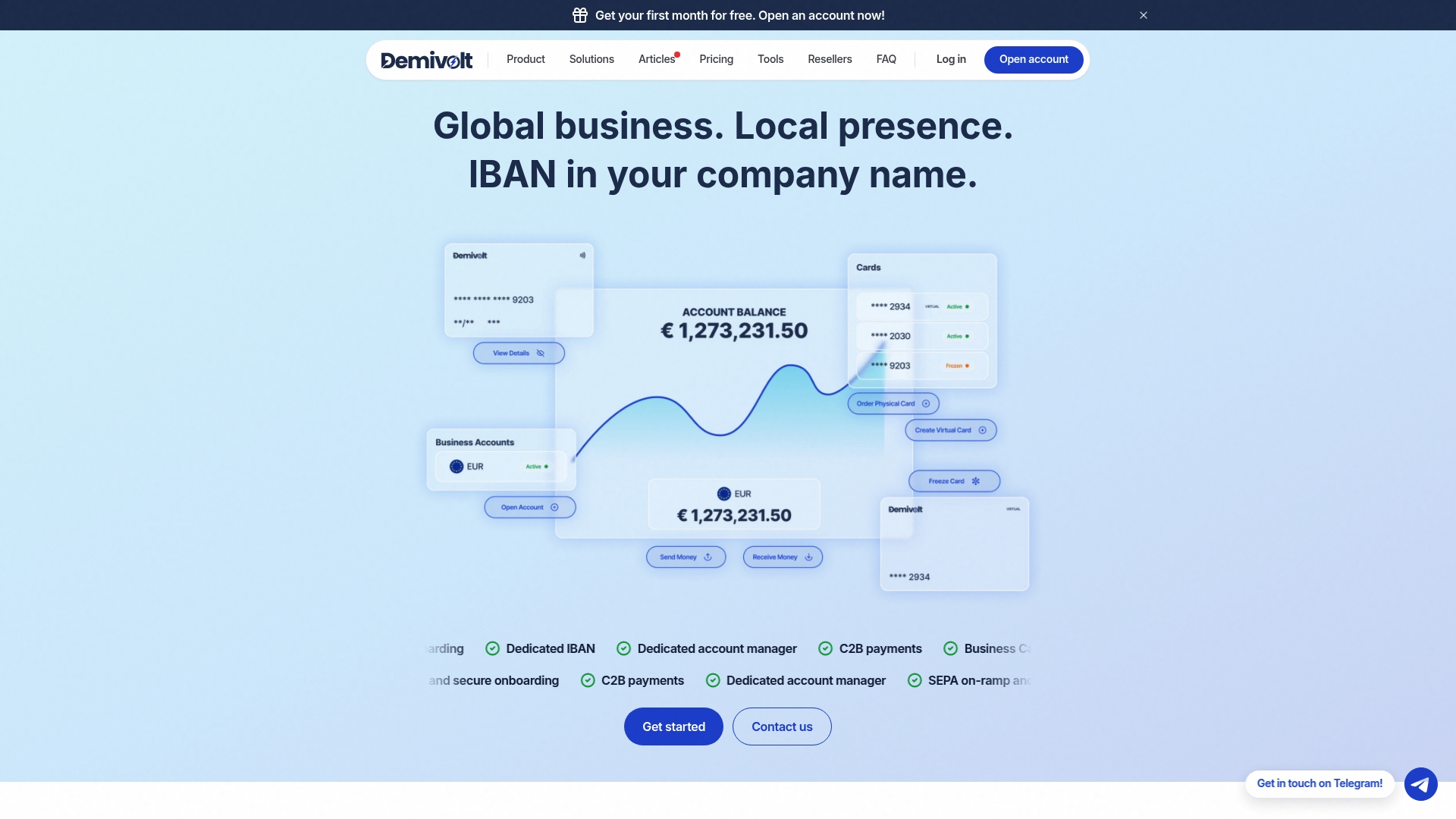

Demivolt

At a Glance

According to the company, Demivolt operates as a licensed electronic money institution under EU regulations, which positions it to offer regulated business banking services across Europe. The platform advertises dedicated IBANs, SEPA and SWIFT transfers, and both virtual and forthcoming physical business cards.

Core Features

Demivolt issues dedicated IBANs and supports inbound and outbound payments using SEPA and SWIFT rails. The dashboard handles multi user account and permission management and supports C2B customer payments for automated collections.

The platform keeps client funds in segregated accounts and offers multi account structures plus role based user controls. Onboarding is presented as fast, compliant, and transparent to meet EU regulatory standards.

Key Differentiator

The single defining edge is the regulated EU license combined with a clearly published per transaction fee model tailored to cross border and digital businesses. That mix makes compliance a visible part of the product rather than an added service layer.

Pros

- Quick account setup and verification reduces time before you can accept payments and issue IBANs. The onboarding claim above is reflected in the vendor materials.

- Transparent fee structure helps finance teams forecast costs for SEPA and SWIFT flows instead of guessing opaque interchange layers.

- Support for both SEPA and SWIFT means you can receive and send EUR and non EUR payments without stitching multiple providers together.

- Multi account structures and role based user management let you separate business units, assign approvers, and limit access for controllers and accountants.

- The platform integrates with partner financial institutions and service providers to extend payment capabilities and custody options for cross border operations.

Cons

- Fees vary by risk assessment and jurisdiction, which can complicate precise monthly cost forecasting for companies with customers in multiple regions.

Who It’s For

Companies that must operate inside EU regulatory frameworks, including regulated aware startups, SMEs, and international digital businesses. Firms that need dedicated IBANs, clear per transaction pricing, and role based access controls will find the product relevant.

Unique Value Proposition

Dedicated IBANs combined with segregated client funds let treasury teams separate revenue streams and reconcile faster. Pairing that structure with per transaction fees means you pay for each movement rather than a blended monthly package, which simplifies margin math for service providers and marketplaces.

Real World Use Case

A Lithuanian startup centralizes receipts and payouts under dedicated IBANs, uses SEPA for most EU vendor payments, and routes occasional SWIFT remittances without introducing an extra provider. Virtual cards handle contractor expenses while the finance team restricts access by role.

Pricing

Per transaction fees are explicit: SEPA outgoing €0.40, SWIFT incoming €25 and SWIFT outgoing €30. Core features and initial account setup are advertised as free and monthly internal transfers are free, while some fees vary by jurisdiction and risk profile.

Website: https://demivolt.com

Adyen

At a Glance

Adyen’s marketing materials state it processes €1.4 trillion annually, a scale that supports its single API approach. That processing claim underpins a platform that spans online and in-person payments, card issuing, payouts, and embedded finance across many markets.

Core Features

- One API for cards, wallets, local methods, card issuing, and payouts so engineering teams avoid juggling separate endpoints.

- Unified commerce that ties online and in-store data for consistent authorizations, reporting, and conversions.

- Built-in fraud management, authentication tools, and compliance controls to manage global risk and regulatory requirements.

Key Differentiator

Adyen centers on a single API supporting payments and financial products at enterprise scale. That architecture reduces integration friction when you add a new country, a local method, or card issuing. For large platforms, fewer bespoke integrations mean faster rollouts and consistent reconciliation.

Pros

- The vendor advertises 99.999% uptime and support for 150+ currencies and 200+ local payment methods, which matters for global merchants with high availability needs.

- Multi-product capability lets you accept payments and run card issuing and payouts from one ledger, reducing settlement fragmentation.

- Flexible SDKs and ready plugins speed time to market while preserving control for in-house engineering teams.

- Advanced role and access management plus PCI-grade controls help meet corporate security requirements and audit timelines.

- Designed to scale; the product suits high-volume flows and complex routing rules without frequent architecture changes.

Cons

- The interface and configuration surfaces can feel complex for smaller teams without dedicated payments engineers.

- Initial setup and bespoke routing require technical resources and may lengthen implementation compared with SMB-focused providers.

- Regional support quality can vary, which means large accounts should plan for local escalation paths.

- Reporting is deep but may miss niche accounting views that some finance teams ask for out of the box.

When It May Not Fit

If your business is a small merchant or early stage startup with limited engineering bandwidth, Adyen’s enterprise focus will add overhead. If you need out of the box accounting mappings for a small finance team, expect to build custom exports or use a third-party connector.

Who It’s For

Large global enterprises and platforms that need one payment stack to cover many geographies, currencies, and product lines. Best when you have payments engineers or an integration partner who can manage routing, issuing, and reconciliation logic.

Real World Use Case

A global retailer unifies checkout and POS reconciliation with Adyen, reducing payment reconciliation discrepancies across markets. Luxury brands and digital subscription vendors cited in Adyen materials used the platform to centralize authorization rules and expand local payment options quickly.

Pricing

Adyen uses enterprise pricing with negotiated rates and custom contracts rather than published per-transaction tiers. Budgets should include integration effort, settlement timing options, and potential interchange pass through when you request a proposal.

Website: https://adyen.com

Stripe

At a Glance

Stripe’s marketing materials state 99.999% uptime, a reliability claim it uses to justify enterprise-grade payment pipelines and SLAs. The vendor also advertises acceptance across 135+ currencies and 195+ countries, which underpins its cross-border payments pitch.

Stripe targets teams that need a payments stack developers can extend while handling global regulatory and currency complexity.

Core Features

- Global payment acceptance across cards, wallets, and local methods with currency conversion and settlements in many markets.

- Flexible billing support for subscriptions, usage-based pricing, and hybrid models that pair invoices with metered reporting.

- Radar fraud prevention and Adaptive Acceptance for routing and approval optimization to reduce declines and chargebacks.

- Embedded finance tools for card issuing, programmable payouts, and hosted accounts plus prebuilt checkout and no-code payment links for quick rollout.

Key Differentiator

Stripe blends a full-suite payments engine with machine learning driven acceptance and routing. That mix gives you both raw payment rails and active payment optimization, which reduces failed payments and shortens time to revenue for global sellers.

Pros

- Developer-friendly APIs make custom flows possible without four-month integration projects. Good docs speed experiments and iterate cycles.

- High reliability and wide payment method coverage reduce regional headaches when you expand into new markets.

- Scalable solutions work from single-developer startups to enterprise deployments, so you can keep one provider as volume grows.

- Rich documentation and support channels shorten implementation time and debugging when problems arise.

- Global fraud and optimization layers help recover revenue that would otherwise be lost to declines.

Cons

- Complex billing setups are daunting for non-technical teams. Advanced pricing models often require engineering time to implement and maintain.

- Native expense management features are limited. You will need a separate expense tool if you want card reconciliation, receipt capture, and policy enforcement in one product.

- Support responsiveness and depth vary by plan level. Smaller merchants get less direct access to technical account management.

When It May Not Fit

If your team lacks engineering resources and wants plug-and-play subscription billing without custom development, Stripe’s flexibility becomes a disadvantage. Also, if you need integrated expense management and corporate card controls, built-in options are thin and you will be juggling additional vendors.

Who It’s For

Developers, startups, and growing enterprises that need a programmable payments stack with global reach and advanced fraud controls. Ideal when you plan to iterate on pricing models, support multiple currencies, or embed cards and payouts into your product.

Real World Use Case

A SaaS company implements usage-based billing using Stripe’s metered billing and automated invoicing, pairs Radar to cut chargebacks, and deploys payment links for self-serve signup in new countries. That combo lets them launch in multiple markets within weeks rather than months.

Pricing

Pay-as-you-go transaction pricing with no fixed monthly fee for basic processing. In the EU, examples in the product data list card fees generally around 1.5% + €0.25 for domestic cards and 2.5% + €0.25 for international cards. Enterprise pricing and professional services are available for large volumes.

Website: https://stripe.com

Worldline

At a Glance

Worldline’s marketing materials report serving merchants and banks across more than 170 countries and being used by over 1.2 million merchants. That scale reflects a vendor that focuses on enterprise breadth and regional customization rather than low-cost, out-of-the-box merchant accounts.

Core Features

- Global payment processing for merchants and financial institutions, including card issuing and acquiring for large platforms.

- In-store and online gateways that cover web, mobile, and point of sale terminals for unified acceptance.

- Omnichannel payments so retailers can route transactions across channels and reconcile sales centrally.

- Cross-border and platform-specific payment routing with local payment method support and authentication tools.

- Digital banking and open banking integrations plus mobile payment options and certified payment terminals.

Key Differentiator

Worldline is built around an established European payment ecosystem that emphasizes local rules and regional partners. That orientation lets large merchants adopt tailored flows and regional payment methods without rebuilding core compliance engines.

Pros

- Reliable core transaction processing and banking links. The vendor claims the merchant footprint above and that scale supports regional acquiring relationships.

- Broad local payment method support lets multinational retailers accept the methods customers actually use in each market.

- Strong compatibility with traditional banking rails and modern open banking APIs, which helps banks and platforms migrate specific services without wholesale replacement.

- A full stack from terminals to gateways and issuer services, useful for chains that prefer one vendor for the entire acceptance stack.

Cons

- Customer support responsiveness is frequently reported as poor during critical incidents, which raises operational risk for high-volume merchants.

- Account lockouts and freezes are noted complaints and can interrupt business flows when they occur.

- Dispute handling and compliance reviews are perceived as slow and opaque, creating delays for funds release and reconciliations.

- Onboarding and verification processes can be lengthy and require more touch points than smaller providers demand.

When It May Not Fit

If you run a small startup or need a low-friction, low-cost acquirer, Worldline’s enterprise orientation will likely feel heavy. Organizations focused on the lowest possible fees or minimal onboarding support should look at providers built for high-speed self-service.

Who It’s For

Large enterprises, banks, and retail chains that require scalable, customizable payment infrastructure with regional compliance built in. Suitable for merchants that prioritize local acquiring relationships and a single vendor for terminals, gateways, and issuer services.

Real World Use Case

A European retail chain implements Worldline’s omnichannel platform to unify card acceptance across stores, web checkout, and mobile apps. The integration reduces reconciliation errors and lets the chain offer country-specific payment options while keeping one compliance workflow.

Pricing

Pricing varies by service, region, and contract size. Worldline typically negotiates fees and models directly with enterprise clients so expect custom pricing tied to transaction volumes, terminal deployments, and value added services.

Website: https://worldline.com

Revolut Business

At a Glance

From £10 per month for basic plans, Revolut Business combines multi-currency accounts, instant payment notifications, and virtual card management inside a mobile-first app. Its onboarding tends to be fast, getting teams from signup to first transfers within hours rather than days.

Core Features

- Multi-currency accounts: Hold, exchange, and send money in dozens of currencies with in-app rates and visible conversion costs.

- Global payments: SEPA and SWIFT transfers plus support for many international rails for vendor and payroll payments.

- Expense management: Manual workflows with AI-assisted categorization to speed reconciliation.

- Virtual and physical card issuance: Create team cards with per-card controls and spend limits.

- Account integrations with Xero, Sage, QuickBooks and a public Revolut API for automation and bookkeeping.

Key Differentiator

The offering centers on a modern, consumer-style interface that brings multi-currency treasury to small teams. Instant alerts and clear in-app FX tools make daily FX decisions and supplier payments feel immediate, which reduces the friction common to legacy corporate banking apps.

Pros

- The app experience is intuitive, so finance staff and nonfinance teammates learn card issuance and transfers quickly.

- Excellent for handling multiple currencies; the in-app FX flow is transparent and often cheaper than native bank transfer markup.

- Fast setup and instant payment notifications reduce reconciliation lag and improve cash visibility for remote teams.

- Card controls let you limit spend by merchant category, amount, or expiry, which trims fraud risk and reduces administrative overhead.

- Integrations with Xero, Sage, and QuickBooks simplify bookkeeping and cut manual CSV imports.

Cons

- Some accounts face restrictions without a clear public explanation, which can interrupt cash flow for affected businesses.

- The expense management featureset can feel limited as transaction volume and team size grow, requiring third-party expense tools for scale.

- Customer support can be slow to reach during critical issues, leaving high-touch customers frustrated when problems need immediate resolution.

- Revolut lacks native credit or loan products in certain regions, so businesses expecting a full bank-like product suite may need separate lenders.

When It May Not Fit

If your company requires advanced AP workflows, enterprise-grade reconciliation, or in-region lending, Revolut Business can feel short. Organizations that must guarantee uninterrupted access with dedicated relationship managers will find the self-service support model constraining.

Notable Integrations

- Xero

- Sage

- QuickBooks

- Revolut API for payment automation and ledger syncing

Who It’s For

Small and medium businesses, freelancers, and startups that move money across borders frequently and prefer fast digital onboarding. Ideal when you need clear FX visibility, card controls for teams, and straightforward accounting syncs.

Real World Use Case

A UK e-commerce merchant collects payments in euros and dollars, holds balances in multiple currencies, and issues virtual cards to contractors. Revolut Business shortens FX steps, posts transactions into Xero, and limits card exposure during promotional spikes.

Pricing

Plans start at £10 per month for basic business accounts, with higher tiers adding more cards, bulk payments, and expense features. Enterprise customers negotiate custom pricing and service bundles for higher volume needs.

Website: https://revolut.com/business

Comparative Analysis of Business Banking Platforms

Navigating the various offerings within the realm of business banking platforms requires a nuanced understanding of how each alternative aligns with specific business needs. Below, we evaluate the platforms under consideration in this context.

Pricing Transparency and Structure

Demivolt excels in providing a straightforward and transparent per-transaction fee structure, aiding businesses in anticipating expenses without the uncertainty of bundled or hidden charges. Conversely, Adyen and Stripe utilize customized enterprise pricing models, which, although tailored, may introduce complexities for businesses preferring predictable cost schedules. Revolut Business, by offering fixed monthly pricing tiers, targets startups and SMEs that value such clarity.

Scalability and Enterprise Suitability

While Adyen and Worldline cater to enterprise-level businesses with layered product needs and expansive geographic operations, smaller teams might find their features excessive. On the other hand, Demivolt combines essential functionalities like dedicated IBANs and regulatory compliance within a more accessible framework, balancing functionality with manageability for mid-sized firms.

Best Fit Recommendations

- Demivolt suits EU-regulated companies requiring dedicated IBANs and clear, predictable transaction pricing.

- Revolut Business addresses the needs of startups and SMEs emphasizing quick onboarding and multi-currency management.

- Adyen benefits enterprises with expansive global operations managed by dedicated integration teams.

- Worldline proves effective for international merchants necessitating tailored local payment methods.

Our Pick for Mid-Sized European Businesses

Demivolt stands as the recommended option for businesses seeking transparent fees and built-in compliance, enhanced by dedicated IBANs and SEPA/SWIFT compatibility. However, businesses without a need for EU regulatory adherence or those aiming for advanced technical integrations might explore alternatives like Stripe or Worldline for a better alignment.

Business Banking and Payment Platforms Compared

Choosing the ideal business banking and payment platform depends on features like regulatory compliance, cost transparency, and the ability to facilitate international transactions efficiently.

| Platform | Core Feature | Key Differentiator | Best For | Pricing | Notable Limitation |

|---|---|---|---|---|---|

| Demivolt | Dedicated IBANs and SEPA/SWIFT support | Regulated under EU frameworks with transparent fees | Digital businesses in Europe | SEPA €0.40 SWIFT €25/30 | Fees varying based on risk or jurisdiction add cost forecasting complexity |

| Adyen | Unified commerce supporting 150+ currencies | Single API for payments and financial products | Large global enterprises | Not disclosed | Requires significant engineering resources for setup and customization |

| Stripe | Global payment acceptance and flexible billing | Machine learning for payment optimization | Startups and enterprises needing flexibility | 1.5% + €0.25 domestic | Complex billing setups challenge non-technical teams |

| Worldline | Global payment processing with local methods | Entrenched in European cross-border ecosystems | Enterprises needing comprehensive solutions | Not disclosed | Customer support responsiveness and account issues frequently criticized |

| Revolut Business | Multi-currency accounts with expense management | Consumer-style interface for treasury operations | SMEs engaging in global transactions | From £10/month | Limited scalability for growing transaction volumes |

Looking for Reliable intergiro.com Alternatives That Prioritize Compliance and Control

If your business faces hurdles in cross-border payments or complex onboarding with intergiro.com, Demivolt could be the solution tailored just for you. Designed to meet stringent European regulatory standards, Demivolt offers dedicated IBANs, transparent per-transaction fees, and role-based user management that give your finance team clarity and control. Companies managing EU and international transactions benefit from fast account setup and secure segregated funds that protect your money.

Explore how Demivolt simplifies SEPA and SWIFT payments while providing virtual and physical business cards to streamline expense management. Visit Demivolt now to open a compliant digital banking account with speed and transparency. Take action to stabilize your international cash flows and generate clearer financial insights with every transaction.

Frequently Asked Questions

What are the main features of Demivolt that make it an appealing alternative to intergiro.com?

Demivolt offers dedicated IBANs and supports both SEPA and SWIFT transfers, which makes it a strong choice for businesses that require efficient cross-border payment solutions. The platform’s ability to handle multi-user account management and segregated accounts adds to its appeal for compliance-focused firms. Companies seeking a streamlined way to manage payments should consider using Demivolt.

How does the pricing of Demivolt compare with Adyen?

Adyen is known for its enterprise pricing model, which is typically negotiated and varies by transaction volume, while Demivolt has a clearly published per transaction fee structure like €0.40 for SEPA outgoing transfers. While Adyen excels in supporting multiple currencies and local payment methods, Demivolt’s transparent pricing makes it easier for businesses to forecast costs. Businesses focused on predictable expenses might prefer Demivolt for its straightforward fee structure.

Which platform is better for small businesses needing fast onboarding: Revolut Business or Demivolt?

Revolut Business is designed for quick setup, allowing users to start transferring within hours, making it ideal for small and medium businesses. Demivolt also claims a fast onboarding process, but it may require more compliance checks. Open-minded businesses looking for rapid access to banking features should find Revolut Business a suitable solution.

Does Demivolt support cross-border payments effectively compared to Stripe?

Demivolt supports both SEPA and SWIFT transfers, focusing primarily on European regions while Stripe is designed to accept payments across 135+ currencies worldwide. If your business needs broad global coverage beyond Europe, Stripe offers a more extensive array of options. For businesses operating primarily within the EU, Demivolt’s tailored services can provide the necessary cost efficiency.

What specific compliance features does Demivolt offer that cater to regulated businesses compared to Worldline?

Demivolt operates as a licensed electronic money institution under EU regulations, ensuring compliance in its payment services, which is a key advantage for regulated businesses. Worldline, while also serving a range of payment needs, may not focus specifically on the same compliance visibility that Demivolt provides. Regulated startups or international businesses might find Demivolt’s compliance approach more aligned with their requirements.