Finding a regulated European business banking provider with transparent fees and flexible account structures is harder than it should be for companies expanding or operating cross-border. Many solutions either hide pricing behind sales calls or limit multi-currency features to high-volume clients, making it difficult to plan banking costs and operations. This comparison covers five business banking alternatives so you can match pricing, compliance, and feature sets to your company’s regional and operational needs.

Table of contents

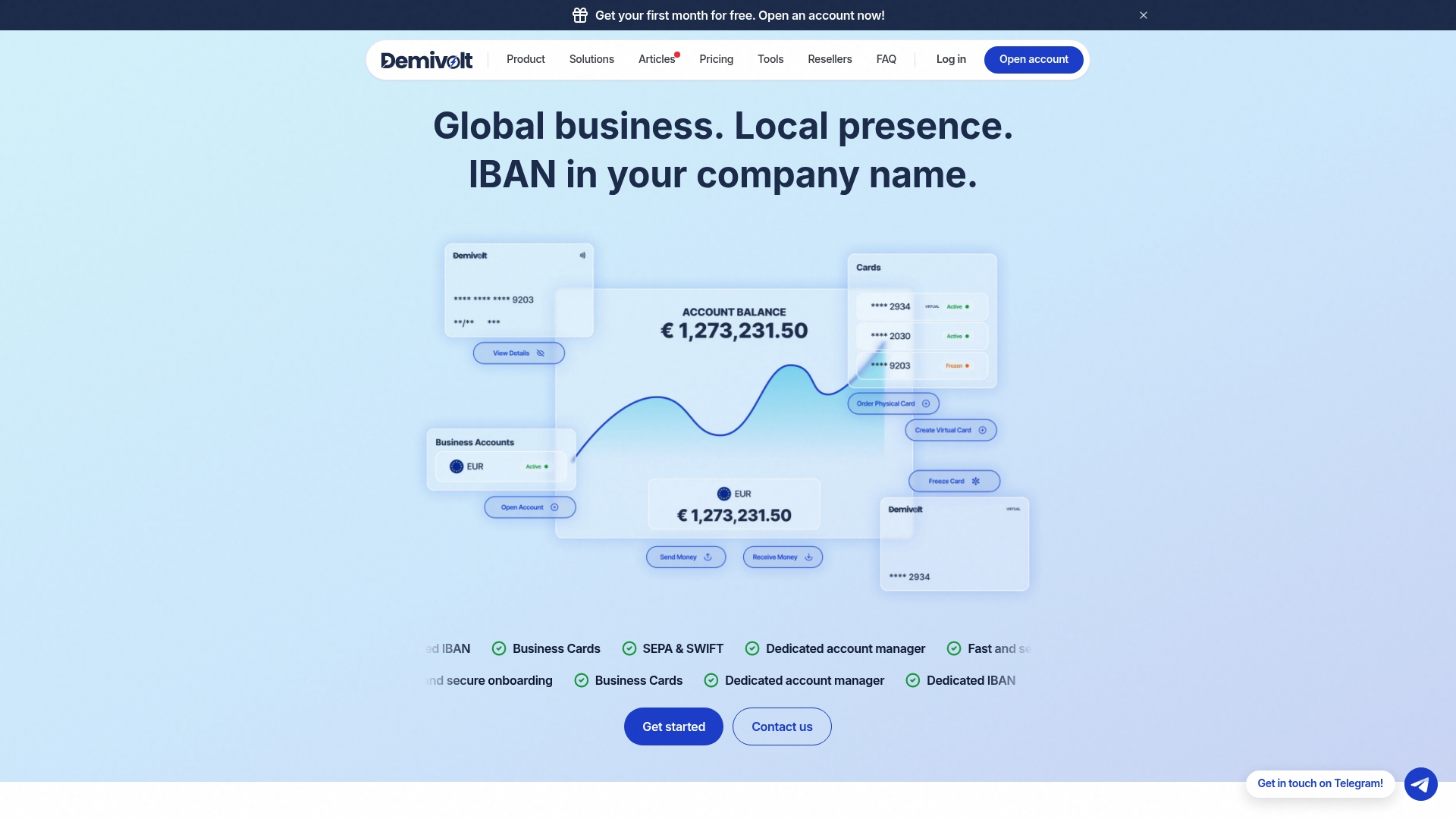

Demivolt

At a glance

No account opening, verification, or monthly maintenance fees appear in Demivolt’s published fee schedule for standard accounts. According to the company, Demivolt operates as a licensed electronic money institution under EU regulations. The product offers dedicated IBANs, SEPA and SWIFT transfers, multi-account structures, and upcoming virtual and physical business cards.

Core features

Demivolt issues dedicated business IBANs so companies can separate operational funds and client money. The platform supports SEPA transfers for euro payments and SWIFT for cross-currency transactions. It includes multi-user account management with roles and permissions to control who can view and move funds. The stack also handles C2B client payments and plans to add virtual and physical business cards for expense management.

Key differentiator

Demivolt centers on regulated banking infrastructure combined with transparent per-transfer pricing specifically for SMEs and international businesses. That combination reduces billing surprises for teams that move money across borders. The platform bundles account controls, role management, and multi-account setups to match operational structures common in digital businesses. This focus positions the product for companies that need clear fee signals and EU-compliant account rails.

Pros

-

Regulated operations give a compliance baseline that most finance teams expect from a business banking provider. This helps when you must demonstrate custody and separation of client funds.

-

Transparent fees remove several common billing surprises. Outgoing SEPA transfers list at €0.40 and SWIFT transfers at €25 to €30 in the published schedule.

-

Built for cross-border use with both SEPA and SWIFT capabilities. That supports suppliers, contractors, and clients across multiple countries.

-

Role based user controls and multi-account structures fit teams that need separate ledgers for product lines or subsidiaries. You can restrict who authorizes outgoing payments.

-

Onboarding is reported as fast and straightforward, which reduces the time your finance team spends on account setup.

Cons

- Card support is not yet live, so companies that need immediate physical or virtual business cards must wait for the upcoming rollout.

Who it’s for

This product fits SMEs, digital first businesses, and international companies that require EU compliant bank rails and clear pricing. Choose Demivolt if you need dedicated IBANs, role based access, and predictable per-transfer fees. It also suits operations that plan to add card based expense programs once card features launch.

Unique value proposition

No monthly maintenance fee plus published per-transfer charges lets finance teams forecast cash outflows with greater accuracy. That predictable fee structure matters when you reconcile margins on international payments. Demivolt also pairs this pricing posture with account controls and multi-account layouts so you can mirror your internal ledger in the platform. The vendor additionally advertises a reseller program that can turn advisors and partners into recurring revenue sources for referral-based firms.

Real world use case

A Lithuanian SaaS company uses Demivolt to centralize international receipts and pay contractors across Europe. The finance lead opened dedicated IBANs for operational revenue and assigned roles to accounting and operations staff. The team preordered virtual cards for employee expenses and tested SEPA and SWIFT flows while tracking fees per transfer.

Pricing

The published schedule shows no account opening, verification, or monthly maintenance fees for basic accounts. Outgoing SEPA transfers are €0.40 per transfer. SWIFT transfers are listed at €25 to €30 depending on corridor. Expect fees to vary by risk assessment and jurisdiction when your application undergoes review.

Website: https://demivolt.com

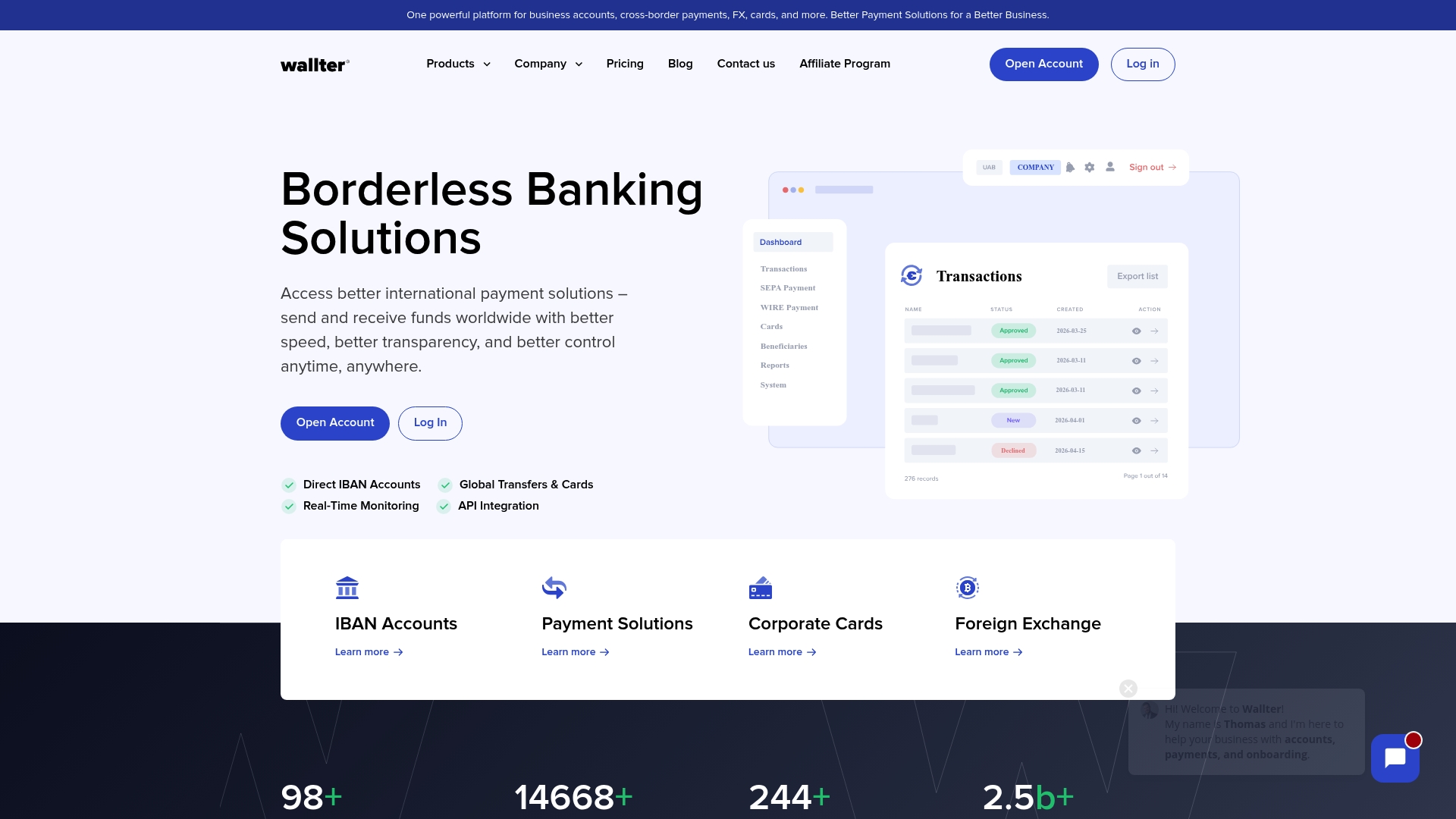

Wallter

At a glance

Wallter’s marketing materials state it supports payments in over 40 currencies. The platform bundles direct IBAN accounts, SEPA and SWIFT transfers, and corporate card options for business clients. Real-time transaction monitoring and API access are central to its online banking interface.

Core features

Wallter offers Direct IBAN accounts for businesses with multi-currency balances. It supports global transfers, mass payments, and both virtual and physical corporate prepaid cards. The platform provides API integration for automating payments, reconciliation, and balance checks. Real-time transaction monitoring and foreign exchange with transparent rates complete the core feature set.

Key differentiator

Wallter’s marketing materials state it is regulated by the Bank of Lithuania within the European Central Bank framework. That regulatory positioning pairs with live transaction monitoring and APIs to give teams finer operational control over cross-border flows. The combination targets businesses that need programmatic banking and visible payment trails.

Pros

- The vendor advertises onboarding in as little as 2 business days, which speeds time to first payment. Quick setup helps teams start paying suppliers and employees faster.

- Strong multi-currency support lets companies hold and move funds across many currencies. That reduces repeated conversions and gives clearer FX control.

- Pricing is described as transparent and competitive for international payments. The stated model separates setup, IBANs, and transaction fees.

- Regulation and compliance are emphasized in the product data, which can reassure finance and compliance teams. The platform also offers multiple user access for team management.

- The web console and APIs provide 24/7 access and real-time visibility into transactions. That helps treasury teams reconcile and respond faster.

Cons

- Pricing is complex with multiple tiers and extra fees for IBANs, transfers, and FX. Small-volume users may find the cost structure hard to predict.

- The product data notes limits on individual transfer amounts for some services such as SEPA Instant. That can disrupt high-value payments.

- Physical card issuance is limited to EUR according to the vendor information. That restricts on-card spending for teams operating outside the eurozone.

- The data mentions potentially high setup fees for premium tiers. That creates an upfront cost barrier for smaller organizations.

When it may not fit

If your company needs physical cards in multiple currencies, Wallter may not meet that requirement. High-volume but low-value users could find the tiered pricing unfavorable. Teams that need unlimited instant transfer size should verify the vendor limits before committing.

Who it’s for

Wallter targets mid-sized to large businesses that run cross-border operations and need multi-currency accounts. It fits companies that want API-driven payment automation and real-time transaction oversight. Treasury teams managing payroll, supplier payouts, or multiple legal entities will find the feature mix relevant.

Real world use case

A tech startup expanding into several European countries uses Wallter to centralize payroll and supplier payments. The team holds funds in local currencies, executes instant SEPA transfers, and issues virtual cards for regional teams. Multi-user access and transaction logs simplify bookkeeping and approvals.

Pricing

Pricing is tier-based with a reported starting setup fee of €500 for the Alpha tier. The vendor states additional charges apply for IBANs, transfers, and currency exchange. Full rate tables and volume discounts are available from Wallter on request.

Website: https://wallter.com

Bebawa

At a glance

Bebawa’s marketing materials state it is regulated and supervised by the Bank of Lithuania. The platform focuses on cross currency operations with multi currency IBAN accounts, SEPA and SWIFT transfers, and FX applied inside transfers. That combination positions it for businesses that must keep operations inside European regulatory frameworks.

Core features

Bebawa offers multi currency IBAN accounts for holding, sending, and receiving funds in several currencies. It supports SEPA and SWIFT transfers with real time tracking and clear fee visibility. Permissions management uses role based controls and audit trails to separate duties and record activity. FX currency conversion uses mid market rates and applies automatically during transfers. The vendor states the infrastructure is built to meet European regulatory and security standards.

Key differentiator

The vendor touts regulatory readiness tailored to European markets as Bebawa’s main strength. That regulatory claim above matters for businesses that must prove supervision and segregation of client funds. The platform packages account flexibility with compliance controls so teams handling payouts, marketplace settlements, or treasury operations can map processes to regulatory requirements. This makes the product narrower in focus than general purpose fintech rails.

Pros

-

Regulated oversight. The vendor reports supervision by the Bank of Lithuania, which matters for firms that require a European regulatory footprint.

-

Flexible account structures. The product supports multiple currencies and account grouping useful for marketplaces and multi entity setups.

-

Built in FX and cross border flows. Currency conversion at mid market rates reduces friction when moving funds across corridors.

-

Permissions and audit trails. Role based controls and transaction logs help you enforce segregation of duties and speed reconciliations.

-

Upcoming card support. The roadmap lists physical and virtual payment cards which will extend spending controls and card payouts.

Cons

-

Pricing clarity is limited. Public pricing is not available and the offering appears tailored to larger or enterprise engagements.

-

Mobile functionality still maturing. Mobile app features are listed as coming soon which limits on the go management today.

-

No listed third party connectors. The product data includes no specific integrations with accounting or ERP systems which may require custom work.

When it may not fit

If your company needs transparent self service pricing, Bebawa may not match your procurement cycle. Companies that rely on mature mobile apps for finance operations will find current mobile capabilities limited. Businesses requiring out of the box accounting or platform integrations should plan for additional integration work or a separate connectivity layer.

Who it’s for

Bebawa targets European businesses that need compliant, multi currency payment infrastructure and can engage with a tailored onboarding process. Ideal buyers run cross border commerce, marketplaces, or fintech services that must show regulatory supervision and manage multiple IBANs. Smaller startups seeking plug and play pricing may prefer alternatives.

Real world use case

A European e commerce marketplace can use Bebawa to collect buyer payments in several currencies and pay sellers across borders. The platform centralizes FX conversion and records permissioned payouts, which simplifies compliance reviews during audits. Adding cards when available will let the marketplace issue spending options to vendors or local teams.

Pricing

Not applicable for public listing. The vendor describes pricing as informational only and appears to use custom quotes for clients. Expect enterprise style commercial terms rather than fixed retail plans.

Website: https://bebawa.com

Ibsettle

At a glance

ibsettle’s marketing materials state it has been regulated and supervised by the Bank of Lithuania since 2016. That supervision positions the company as a licensed European electronic money institution. The product targets businesses that need remote, compliant banking plus API automation.

Core features

ibsettle supports multiple account types including business, personal, and cumulative accounts. The platform handles SEPA and international cross border payments for business flows. It offers currency exchange across more than 20 currencies for operational FX needs. The online banking portal provides account management and transaction controls. A B2B API enables automation of payment and reconciliation workflows.

Key differentiator

The vendor highlights a regulated European EMI status paired with an emphasis on API driven automation. That combination aims to serve companies that embed banking into product workflows. Pricing tiers are tailored by client profile to match differing transaction volumes and jurisdictions.

Pros

-

Regulated supervision. The company states it is overseen by the Bank of Lithuania, which helps meet EU regulatory expectations for European accounts.

-

Multi currency accounts. Having more than 20 currencies simplifies treasury for regional businesses.

-

Remote onboarding. You can open and manage accounts without visiting a branch, which speeds international expansion.

-

API integration. The B2B API and online banking API let engineering teams automate payouts, FX, and reporting.

-

Transparent tiering. The vendor advertises tiered pricing that aims to match different client profiles and volumes.

Cons

-

Pricing complexity. The tiered model can be hard to evaluate without a consultation or reviewing the vendor PDF. New clients may need time to model fees.

-

Limited physical card services. The product data lists mostly digital account capabilities and does not mention physical business cards.

-

Sparse UX details. The materials provide limited information about the user interface or mobile app experience.

When it may not fit

If you require physical card issuance for expense programs, this solution may not meet your needs. Companies that want simple, flat fee pricing may find the tiered model cumbersome. Organizations needing extensive product UX details before evaluation will face an information gap.

Notable integrations

- B2B API for payments and reconciliation.

- Online Banking API for account operations and reporting.

Who it’s for

ibsettle targets mid sized enterprises, fintechs, and startups that need regulated, multi currency digital banking. It suits engineering teams that want programmatic control over payments. It also fits companies expanding into European markets that need compliant account rails.

Real world use case

A Lithuanian startup uses ibsettle to manage euro collections and currency exchange while expanding into neighboring markets. Engineers call the B2B API to automate vendor payouts and reconciliation. The startup avoids local banking paperwork by keeping accounts and controls online.

Pricing

Pricing varies depending on client jurisdiction, account type, and transaction volume. The vendor publishes detailed pricing in a PDF and on the website, so you must request the relevant client tier to model costs.

Website: https://ibsettle.com

Monzo bank

At a glance

According to the company, Monzo’s Call Status feature has helped prevent around 1,000 scam attempts monthly. The app pairs a UK current account with real time spending alerts and organized savings tools. That mix makes it easy for individuals and small businesses to manage cash from a phone without visiting a branch.

Core features

Monzo combines account management with built in money organization and security tools.

- Pots for organizing funds into project or goal accounts, useful for tax or payroll separation.

- Fee free UK current account with instant notifications and spending insights that show category level spend.

- Savings options including instant access and ISAs with competitive interest rates that can change over time.

- Money management tools such as round ups, virtual cards, and cashback deals at selected retailers.

- Security features including card freeze, biometric login, and fraud prevention measures like Call Status to reduce scam risk.

Key differentiator

Monzo emphasizes fraud prevention through Call Status. The figure above shows the volume of scam attempts it claims to block each month. That focus matters for businesses and freelancers who receive many incoming calls and need extra protections against impersonation and social engineering.

Pros

- According to the company, Monzo reports a 4.6 star Trustpilot rating. This reflects strong reported customer satisfaction and high marks in independent awards.

- The app delivers immediate transaction notifications and categorized spending insights. That helps you spot unexpected charges the moment they occur.

- Security tooling is extensive for a mobile bank. Card freeze and Call Status aim to reduce fraud exposure for everyday users.

- Business friendly features support simple bookkeeping workflows. Pots and virtual cards make it easier to separate client funds and control team spending.

Cons

- Some customers report delays during account switching or setup at peak times. That can slow onboarding for new hires or new company accounts.

- Savings interest rates are variable and can drop below fixed rate alternatives. If you need guaranteed returns, Monzo may not be the best choice.

- Premium plans like Max and Perks can be pricey for users who do not use the extra features regularly. That adds recurring cost pressure for lean operations.

- No physical branches exist for in person banking needs. Clients who want face to face service will need a traditional bank.

When it may not fit

If your operation requires in person branch support, Monzo will not meet that need. If you need fixed rate savings or guaranteed returns, look elsewhere for dedicated savings products. Businesses outside the UK will find account availability limited because Monzo targets UK residents and companies.

Who it’s for

Monzo suits tech savvy UK residents and small business owners who prefer mobile first banking. It fits freelancers who want simple bookkeeping controls and instant alerts. It also fits SMEs that use virtual cards to control employee spending.

Real world use case

A freelance designer separates client deposits into Pots for each project. She uses instant alerts to track spending and virtual cards for vendor subscriptions. Cashback deals and easy transfers save time compared with manual tracking.

Pricing

Standard accounts are Free. Premium plans start from £3 a month for added features. The Max plan begins at £17 a month for a fuller package including extra protections and perks.

Website: https://monzo.com

Comparison of alternatives

When selecting a business banking platform, evaluating options for transparency, multi-currency capabilities, and digital banking functionality is essential. Here, we compare Demivolt, Wallter, Bebawa, ibsettle, and Monzo Bank to highlight their respective strengths and ideal usage scenarios.

Pricing transparency and predictability

Demivolt stands out with its clearly published per-transfer fees, allowing businesses to accurately budget financial outflows. Bebawa, by contrast, does not provide public pricing, requiring potential clients to discuss terms individually. While Wallter offers competitive pricing for international payments, its tiered structure may feel opaque to smaller enterprises.

Onboarding and currency handling

Wallter provides an expedited onboarding process, advertised as complete within two business days, supporting over 40 currencies for global operations. Demivolt and ibsettle offer straightforward account setup procedures but cover fewer currencies in their standard packages. Bebawa emphasizes customized onboarding but lacks the speed of Wallter.

Best fit

-

Choose Demivolt if transparent per-transfer costs and compliance with EU regulations are priorities for your business operations.

-

Select Wallter when rapid onboarding and multi-currency accounts are essential needs.

-

Consider Bebawa if your company handles high-value transactions within strict European compliance frameworks.

-

Choose Monzo Bank for UK-specific small business banking with a user-friendly mobile-centric design.

Our pick

Demivolt emerges as the leading choice for international SMEs seeking transparent pricing aligned with regulatory compliance and digital banking essentials. Its dedication to clarity in financial operations and commitment to supporting modern multi-regional businesses make it a valuable solution. Businesses with more specific needs, like a UK presence or multi-currency support, may find better matches among the alternatives, highlighting the tailored fit Demivolt provides in its specialization.

Selecting the most suitable European business banking solution emphasizes identifying the platform that addresses your organization’s key operational needs.

| Platform | Core Features | Best For | Pricing | Notable Limitation |

|---|---|---|---|---|

| Demivolt | Dedicated IBANs, SEPA/SWIFT, Role controls | SMEs needing EU compliance | No maintenance fees; SEPA €0.40, SWIFT €25-30 | Card functionality pending launch |

| Wallter | Multi-currency IBANs, API integration, corporate cards | Mid-large businesses with international payments | €500 setup; tier-based fees | Complex pricing structure |

| Bebawa | Multi-currency IBANs, mid-market FX within transfers | European marketplaces needing compliant operations | Not disclosed | Limited mobile app functionality |

| ibsettle | Multi-currency, B2B API for automation | Fintechs embedding payments in workflows | Tiered by client profile and volume | Limited physical card options |

| Monzo Bank | Real-time alerts, savings tools, virtual cards | UK-based freelancers and SMEs | Standard: Free; Max: £17/month | No physical branch support |

Discover a smooth alternative to MisterTango.com with Demivolt

Finding reliable financial infrastructure that offers clear pricing, dedicated IBAN accounts, and role-based access can be challenging when exploring mistertango.com alternatives. Demivolt meets these needs by delivering transparent, EU-regulated business banking designed for international and digital-first companies. With no monthly maintenance fees and straightforward per-transfer charges, Demivolt helps businesses reduce surprises and control cash flow across borders.

Experience faster onboarding and gain financial control with Demivolt’s multi-account structures and upcoming virtual and physical cards. Visit Demivolt to open dedicated IBANs tailored to your operations and take control of your payments today.

FAQ

What are the key features that make Demivolt a strong alternative to MisterTango.com?

Demivolt provides dedicated business IBANs, SEPA and SWIFT transfer capabilities, and role-based account management. This aligns with the requirements of SMEs and international businesses looking for clear fee structures and operational control.

How does Demivolt compare to wallter in terms of pricing and onboarding?

Wallter offers quick onboarding in as little as 2 business days and emphasizes competitive pricing for international payments. Conversely, Demivolt has no account opening or monthly maintenance fees, making it ideal for businesses focused on predictable per-transfer charges.

Which platform is better for multi-currency support, Demivolt or bebawa?

Bebawa excels with its multi-currency IBAN accounts designed specifically for cross-currency operations. Meanwhile, Demivolt also supports currency exchanges but is best suited for businesses needing EU-compliant banking without complex pricing structures.

Can i expect fast account setup with Demivolt?

Yes, Demivolt’s onboarding is described as fast and straightforward, which helps reduce the time needed for account setup for finance teams.

How does Demivolt handle monitoring of fees compared to ibsettle?

Demivolt offers transparent pricing with clearly published fees, such as outgoing SEPA transfers at €0.40. In contrast, ibsettle uses tiered pricing which can complicate cost evaluation for new customers.