Managing cross-border payments, multi-currency account structures, and team permissions with legacy business banks introduces hidden fees and onboarding friction. Traditional providers either obscure transfer costs or lock required features like dedicated IBANs, role-based controls, and API automation behind slow approvals or unclear pricing. This comparison details three alternatives to match your business needs for transparent fees, rapid onboarding, and scalable international payment solutions.

Table of Contents

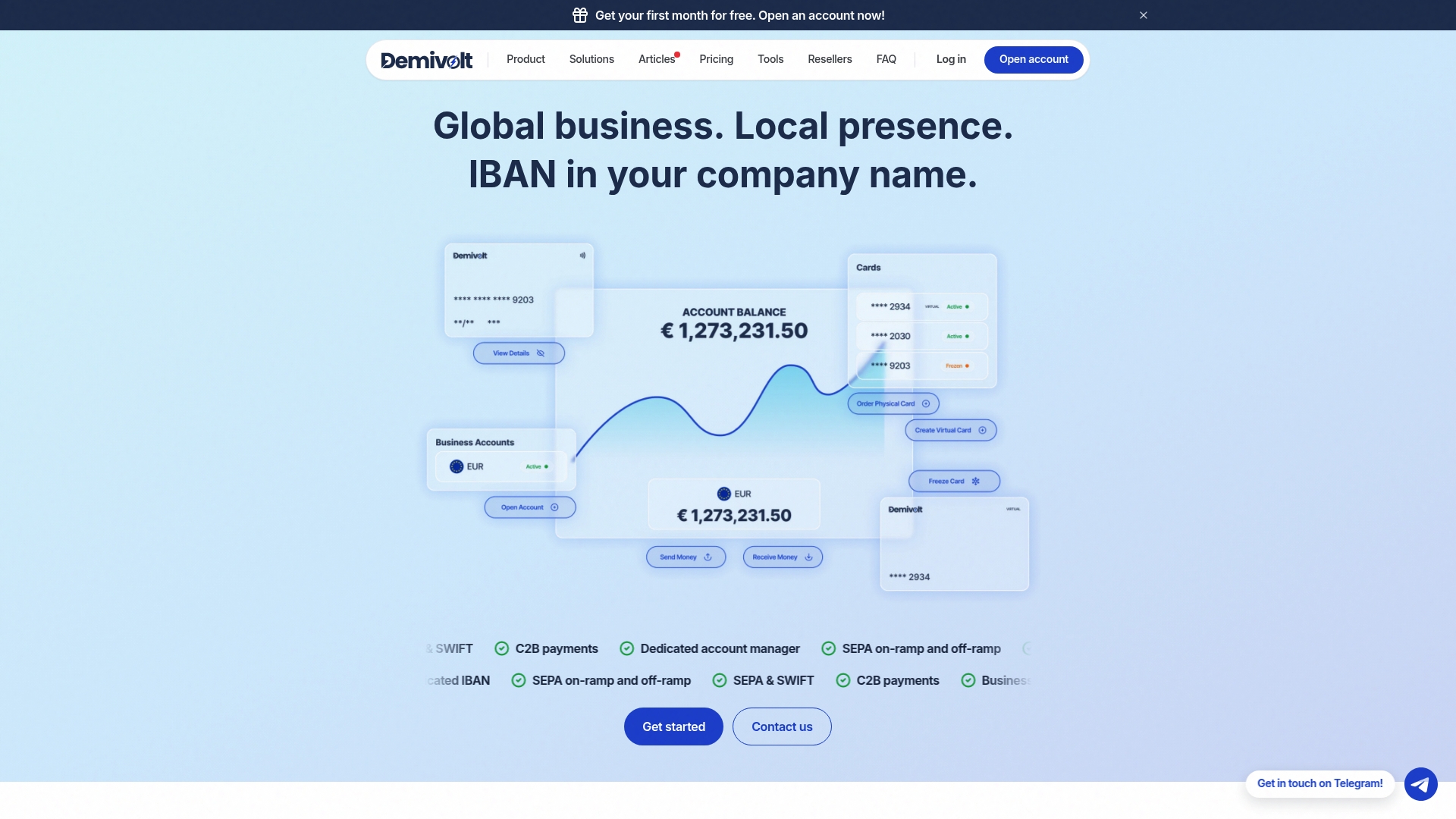

Demivolt

At a Glance

Accounts are free to open and verify. SWIFT outbound transfers are priced at €30 and SEPA outgoing transfers at €0.40 each, which makes transaction costs easy to model for cross border work.

The vendor advertises it is a regulated electronic money institution and reports simplified onboarding with quick approval times; that regulatory claim and the onboarding promise are central to the product pitch.

Core Features

- Dedicated IBANs for business accounts to separate client receipts and reconciliation.

- SEPA and SWIFT transfer support for inbound and outbound international payments.

- Virtual business cards now, with physical cards coming soon according to the roadmap.

- Customer to business payment receiving and multi currency handling for cross border sales.

- Multi user account management with roles and permissions plus multi account structures for teams.

Key Differentiator

That regulatory claim above, combined with an explicit fee schedule and dedicated IBAN accounts, is the single practical differentiator. Demivolt packages a regulated EU payments stack with clear per transfer pricing rather than opaque tariff tables.

Because fees are explicit and accounts can include multiple IBANs and users, finance teams can assign incoming flows, run reconciliations, and forecast cash outflows without guesswork.

Pros

- The account model supports dedicated IBANs, which simplifies client billing and keeps incoming transfers traceable per product line or country.

- Transparent, predictable fees make margin math straightforward. The published €0.40 SEPA and €30 SWIFT figures let you compare transaction costs to legacy bank quotes in minutes.

- The platform supports multiple currencies and international transfers, so treasury teams can consolidate European operations without juggling local banks.

- Role based user controls and multi account structures let finance leaders separate duties and restrict access without creating separate legal entities.

- The vendor states quick, compliance friendly onboarding and segregated custody of client funds, which is useful when auditors ask for proof of separation from the provider’s operating accounts.

Cons

- Physical cards are not yet available; only virtual cards are announced, which limits in person or corporate card replacement use cases for now.

Who It’s For

European small and midsize enterprises, digital first service companies, and regulated entities looking for compliant, low friction business banking inside the EU. It fits teams that need multiple users, dedicated IBANs, and predictable transfer pricing.

Unique Value Proposition

Charging €0.40 for SEPA and publishing a clear SWIFT fee changes vendor conversations. For SMEs that run frequent euro transfers, predictable per transfer costs reduce surprises during monthly reconciliation and simplify pricing comparisons against incumbent banks.

Paired with dedicated IBANs and role based controls, that pricing makes day to day treasury operations easier to model and to defend in procurement or board conversations.

Real World Use Case

A Lithuanian tech startup consolidates all customer receipts to dedicated IBAN accounts and uses role based permissions so product teams can view invoices while the finance team controls payouts. SEPA fees drop line item costs compared with the legacy bank, and multi currency receipts are handled within the same account structure.

Pricing

Free to open and verify accounts. SEPA outgoing transfers cost €0.40 each. SWIFT outbound transfers cost €30. Other fees depend on risk profile, the services you use, and non EU or higher risk jurisdictions.

Website: https://demivolt.com

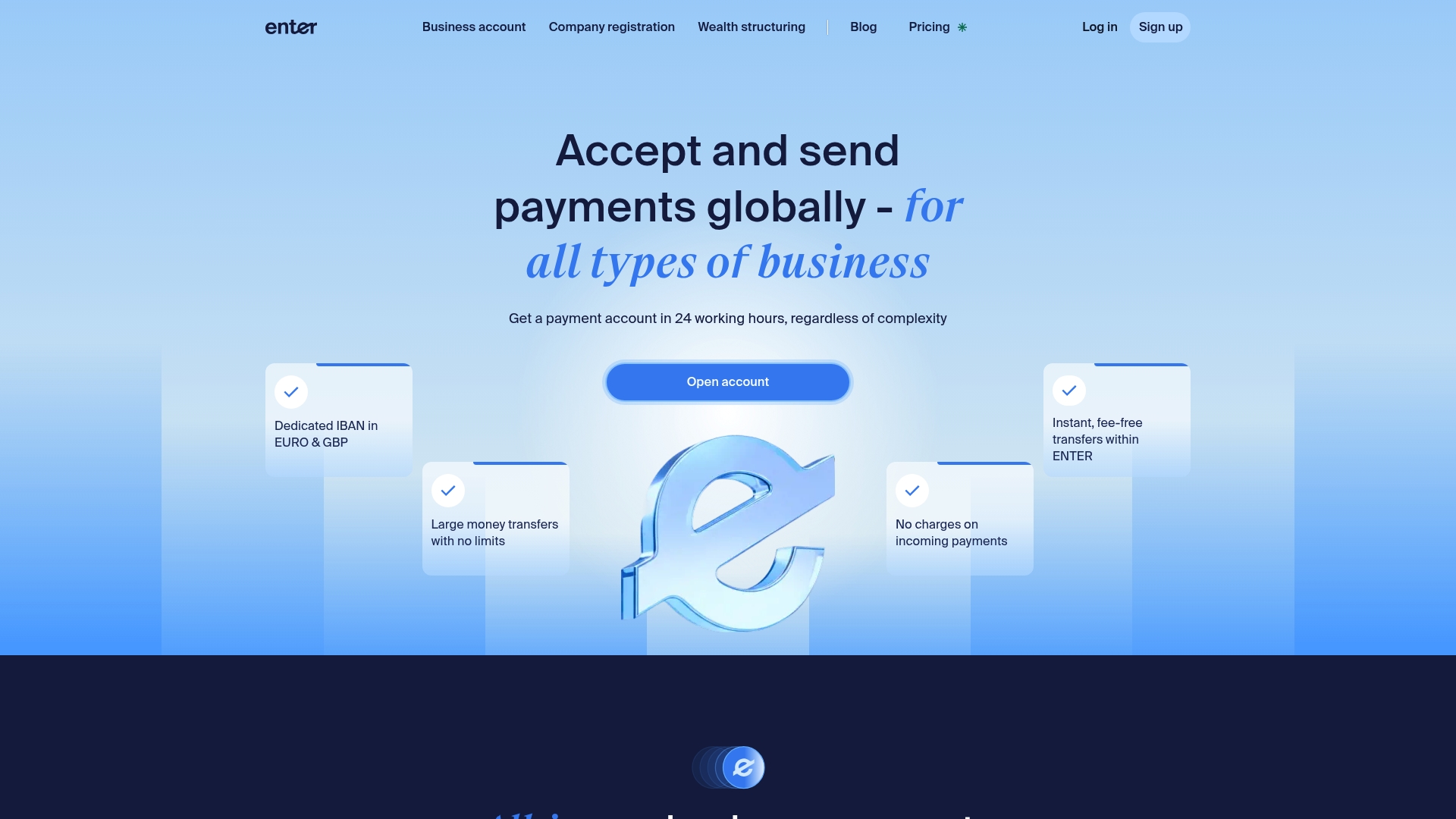

Enter Global

At a Glance

Enter’s marketing materials state a 24-hour account setup for many applicants, paired with dedicated IBANs in EUR and GBP for immediate cross-border operations. That quick onboarding claim shifts the usual wait time for business accounts into an operational advantage for teams hiring or launching sales regions.

Core Features

- Dedicated IBANs in EUR and GBP for incoming collections and payouts.

- Instant transfers via SEPA and SWIFT for supplier and payroll payments.

- Corporate cards with role-based access and spend controls for teams.

- Two-factor authentication and an AML-focused compliance framework that includes risk assessments and client screening.

Key Differentiator

The combination of rapid onboarding and multi-currency dedicated accounts is Enter’s headline. The vendor advertises that 24-hour setup above along with personalized support targeted at complex ownership or multinational structures. That mix positions Enter as a payments partner for organizations that must move quickly across borders.

Pros

- Fast first use. Quick setup reduces the lead time between legal formation and live payments, which helps exporters and service firms start accepting funds sooner.

- Team control and cards. Adding extra corporate cards with role permissions simplifies expense workflows for growing teams.

- No incoming payment charges and support for unlimited large transfers lower friction for high-volume receivables.

- Strong compliance posture. Funds are held in segregated accounts and the platform includes AML procedures aimed at cross-border risk.

- Broad suitability. The feature set covers startups, SMEs, family offices, and mid-sized enterprises with international flows.

Cons

- Reported support delays. Some users say customer responsiveness is inconsistent, which creates friction during urgent issues.

- Onboarding complexity. Detailed compliance checks can be more cumbersome for companies with layered ownership or high-risk activities.

- Price sensitivity. Monthly maintenance and tariff structures may run higher than simple alternatives for businesses with basic banking needs.

- Fee transparency. Specific international transfer fees are not always listed in detail, which can make cost forecasting harder.

When It May Not Fit

If you need a purely commodity account with the lowest possible fees, Enter’s richer feature set and compliance steps may be overkill. Companies in high-risk sectors will face longer verification cycles. Teams that require 24/7 live support should probe service SLAs before committing.

Who It’s For

Organizations that need reliable multi-currency accounts and active cross-border payment tools. Typical profiles include exporters, global e-commerce merchants, investment firms, and family offices that require role-based card management and compliance controls.

Real World Use Case

A mid-sized export-import firm opens an Enter account to collect in EUR and pay suppliers in GBP. They issue corporate cards to purchasing and logistics teams, use instant transfers for urgent supplier payments, and rely on the compliance checks to meet AML requirements when onboarding new overseas partners.

Pricing

Maintenance starts at €50 per month with onboarding fees from €200 depending on classification and risk profile. Multiple tariff plans exist for different company sizes and activities, so negotiate based on volume and entity type.

Website: https://enter.global

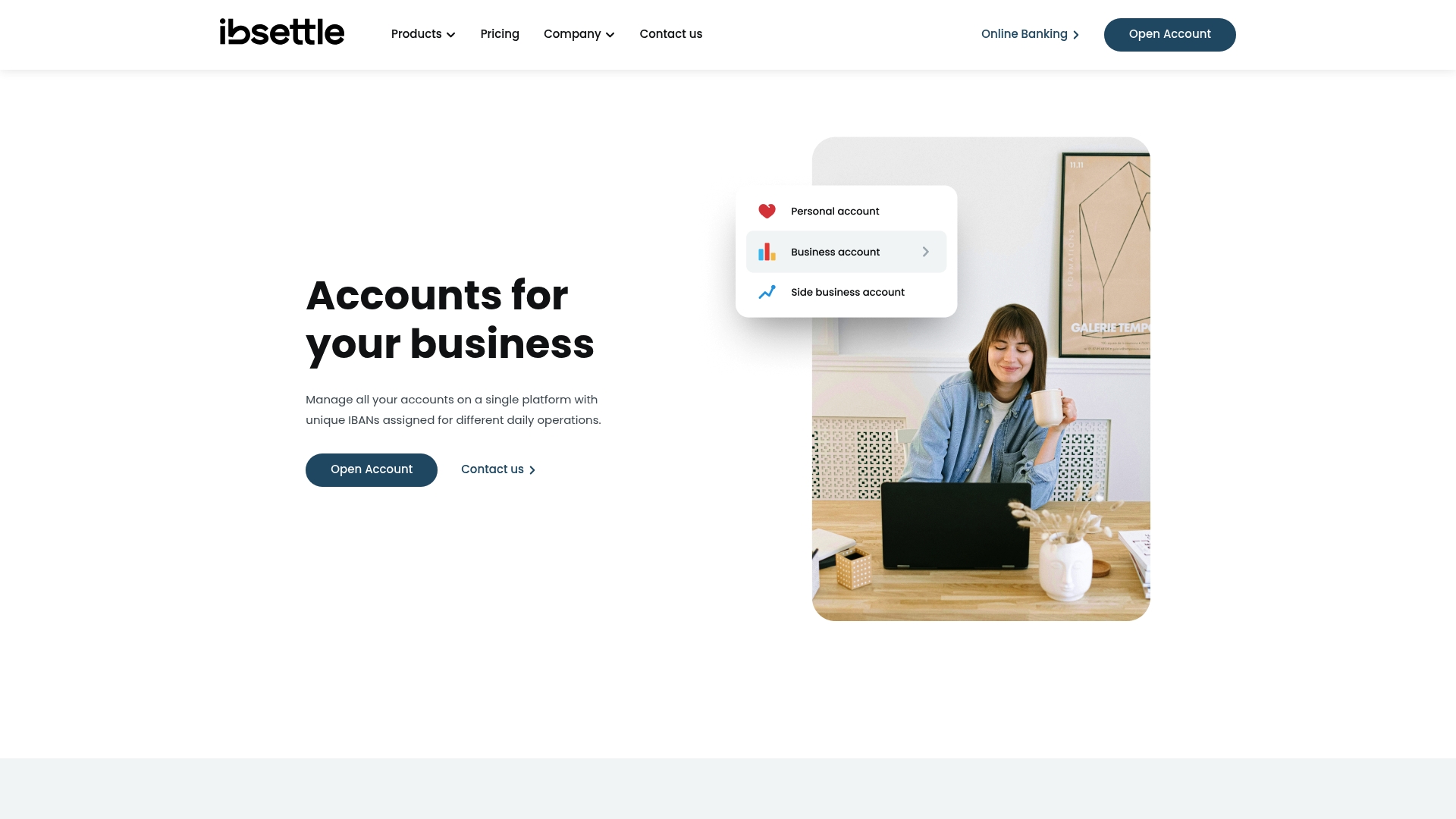

Ibsettle

At a Glance

Offers currency exchange in over 20 currencies and assigns unique IBANs for business and personal accounts, all under a Lithuanian regulated Electronic Money Institution framework. That combination makes international cash flow and FX management possible without a traditional bank relationship.

Core Features

- Multi-currency accounts with dedicated IBANs for business, cumulative, and personal needs.

- SEPA and international payment rails for cross-border transfers plus on-platform currency exchange across the offered currencies.

- B2B API and online banking interface for automated payouts, reconciliation, and account management.

- Remote onboarding and digital account administration aimed at companies that operate across borders.

Key Differentiator

Ibsettle pairs the regulatory status of an EMI with a developer-friendly API and remote onboarding. That matters when you need programmable accounts and automated payouts while keeping client funds inside a regulated framework rather than an unregulated payments layer.

Pros

- Regulated footing. As a regulated EMI, Ibsettle provides the governance and custody separation many fintechs require when moving client funds.

- Good for multi-currency operations. The account model and FX table reduce friction when a company regularly receives and pays in different currencies.

- Automation-first. The vendor’s B2B API and online banking tools let finance teams push payments and pull statements without manual exports.

- Remote onboarding. You can open and manage accounts digitally, which speeds initial setup when physical branch visits are impossible.

- Dedicated support. Clients report access to account managers for escalations and more involved onboarding needs.

Cons

- Onboarding can be slow. Many users report a long and bureaucratic account opening process with repeated documentation requests.

- Support inconsistency. Several reports point to poor responsiveness or conflicting instructions from support staff.

- Requirements vary. Non-resident clients may face shifting or unclear documentation checkpoints that delay approvals.

When It May Not Fit

If you need immediate onboarding inside a 48-hour window, Ibsettle’s reported account opening delays will frustrate you. If your finance team requires a consistently responsive relationship manager for high-volume daily settlements, the inconsistent support experience could introduce operational risk.

Notable Integrations

- B2B API for programmatic payments and reconciliation.

- Online banking system for manual controls and reporting.

- Open Banking PSD2 connectors for account aggregation and payment initiation.

Who It’s For

Small to medium enterprises, fintech startups, and entrepreneurs that need regulated multi-currency accounts, programmable payouts, and remote onboarding across Europe. Best when your priority is API-driven automation rather than instant account provisioning.

Real World Use Case

A Europe-focused startup consolidates receipts from three markets into Ibsettle accounts, uses the API to automate vendor payouts in local currencies, and executes FX conversions on demand. The team eliminates multiple correspondent banks while keeping everything accessible via a single online interface.

Pricing

Pricing follows tiered fees based on client location and service type; the vendor publishes detailed fee tables on its pricing page. Expect additional charges for certain transaction types, unique IBANs, or account services depending on your region and volume.

Website: https://ibsettle.com

Comparative Analysis

Selecting the right business banking solution involves evaluating several dimensions, such as onboarding efficiency, cost transparency, compliance features, and functional scope. Below, we compare Demivolt, Enter Global, and Ibsettle to help identify the best fit for various business scenarios.

Onboarding and Account Setup

Demivolt and Enter Global both emphasize streamlined onboarding processes. While Demivolt promises quick, compliant account activations, Enter claims setup within 24 hours for qualifying clients. This makes Enter exceptionally suited for businesses that prioritize immediate operational readiness. However, Ibsettle’s onboarding process includes documentation checks, which, although potentially time-consuming, may appeal to organizations requiring rigorous compliance oversight.

Costs and Transparency

Demivolt’s clearly defined fee structure, such as a fixed €0.40 SEPA transfer fee, offers significant transparency in transaction costing, aiding financial planning. In contrast, Enter Global’s more variable tariff model caters to a variety of use cases but may hinder straightforward cost forecasting. Similarly, Ibsettle provides tiered fees based on account activity, which can reward high-volume users but may introduce complexity for smaller enterprises.

Feature Richness

For businesses requiring integrated functionalities, such as B2B APIs for payment automation, Ibsettle delivers a compelling solution. Conversely, Demivolt’s focus on multiple currency handling with dedicated IBANs suits entities that manage diverse European operations. Meanwhile, Enter Global’s corporate cards with spend controls provide meaningful value for organizations managing significant team expenditures.

Best Fit

- For enterprises necessitating predictable transaction fees across multiple accounts, Demivolt is well-matched.

- For businesses prioritizing near-immediate account activation to minimize operational delays, Enter Global is advantageous.

- For companies requiring custom API integrations for automated financial flows, Ibsettle offers advanced programmability.

- Demivolt pairs compliance and dedicated account functionality, ideal for SMEs managing international finances.

Our Pick

Demivolt stands out for its blend of transparency, dedicated account features, and user-access management, streamlining financial operations for entities handling cross-border funds. However, organizations needing rapid setup or advanced integration might consider Enter and Ibsettle, respectively, based on their unique advantages.

Business Banking and Payments Platforms Comparison

Selecting the most suitable business banking and payments platform hinges on understanding each option’s core features and pricing models.

| Product Name | Core Feature | Best For | Pricing | Notable Limitation |

|---|---|---|---|---|

| Demivolt | Dedicated IBANs and transparent fees | SMEs and cross-border sales | SEPA transfers: €0.40, SWIFT transfers: €30 | Physical cards not yet available |

| Enter Global | EUR/GBP IBANs and instant transfers | Startups with compliance needs | Maintenance: €50/month | Customer support responsiveness varies |

| Ibsettle | Multi-currency accounts and API | Automated payments in Europe | Tier-based by region and volume | Slow onboarding process reported |

Discover Demivolt as a Leading paynexpay.com Alternative for Your Business Banking Needs

If you are looking for a transparent, regulated European fintech platform that simplifies cross-border payments and offers dedicated IBANs, Demivolt is designed for you. With clear per transfer fees like €0.40 for SEPA and €30 for SWIFT payments, Demivolt removes the guesswork from international transactions. Their fast and compliant onboarding process combined with multi-user account management and role-based access empowers businesses to maintain strong financial control and compliance.

Explore how Demivolt can help you cut costs and gain operational efficiency with digital-first business banking tailored for SMEs and cross-border teams. Visit Demivolt now and open your account to start managing dedicated IBAN accounts and issuing virtual cards in minutes.

Frequently Asked Questions

What are the benefits of using Demivolt for business banking and payments?

Demivolt offers dedicated IBANs, which simplify client billing and ensure traceable incoming transfers per product line or country. This feature enables finance teams to manage client receipts and reconcile accounts more efficiently. Businesses looking for effective international payment solutions should consider opening a Demivolt account.

How does Demivolt’s fee structure compare to that of Enter Global?

Enter Global provides a no incoming payment charge policy, making it an attractive option for high-volume receivables. In contrast, Demivolt charges €0.40 for SEPA and €30 for SWIFT transfers, ensuring transparency in transaction costs. Companies that prioritize predictable fee structures might find Demivolt to be the better fit for their banking needs.

What features make Demivolt suitable for small European enterprises?

Demivolt is specifically designed for small and midsize enterprises by offering features like multi-user account management, roles and permissions, and dedicated IBANs. These capabilities are essential for finance teams needing clear oversight and management of incoming flows. Smaller businesses often benefit from these tools to streamline their financial operations.

Can businesses expect quick onboarding with Demivolt?

Demivolt offers quick compliance-friendly onboarding, which is advantageous for companies needing fast access to banking features. The vendor emphasizes rapid account setup to align with business demands, making it a suitable option if you’re looking to get a business account up and running without the delays typical with traditional banks.

What is the current status of physical cards with Demivolt?

Demivolt currently only offers virtual business cards, and physical cards are coming soon according to their roadmap. This limitation could affect businesses that require in-person transactions or corporate card replacements in the meantime. However, the introduction of physical cards may expand options for users in the future.

Recommended

- Demivolt | Blog – Top 3 2payapp.com Alternatives 2026

- Demivolt | News – NexaPay Review 2026: Is This Crypto Payment Gateway Legit?

- Demivolt | News – Inside NexaPay.one: How an Estonian Crypto Payment Company Built such a Gateway

- Demivolt | News – The Best High-Risk Payment Gateway in 2026: With Crypto Settlement Options