TL;DR:

- SWIFT is a secure messaging network that transmits standardized payment instructions between banks, enabling reliable international transfers without directly moving funds. Businesses use SWIFT for cross-border payments, and recent ISO 20022 migration enhances data quality and automation, while UETR helps track payments in real time. Effective SWIFT use requires precise data entry, disciplined tracking, and understanding costs, ensuring optimal operational and financial outcomes.

SWIFT is a global secure messaging network that transmits standardized payment instructions between banks, enabling businesses to send and receive international payments reliably. This guide to SWIFT payments for businesses covers everything finance professionals need: what SWIFT actually does, how to initiate a transfer correctly, how the ISO 20022 migration changes your workflow, and how to track payments using the UETR system. SWIFT processes over 45 million messages daily, connecting more than 11,000 institutions worldwide. That scale explains why SWIFT remains the backbone of corporate cross-border payments in USD, EUR, and every other major currency.

What does a SWIFT payment guide for businesses actually cover?

SWIFT is not a money transfer service. SWIFT structures payments as secure messages that standardize communication between banks, ensuring reliability without directly moving funds. Your bank reads the instruction, debits your account, and credits the recipient’s bank through a chain of relationships. Understanding this distinction is the first step to managing international payments without surprises.

Businesses use SWIFT for supplier payments, payroll across borders, intercompany transfers, and receiving client funds from overseas. The network supports multiple message types. MT103 handles customer credit transfers, meaning the payments you send to suppliers or partners. MT202 handles interbank liquidity movement behind the scenes. Since november 22, 2025, SWIFT mandates ISO 20022 format for all cross-border payments, replacing the older MT format with richer structured data standards like pacs.008 and pacs.009.

The UETR, or Unique End-to-End Transaction Reference, is a 36-character identifier embedded in every SWIFT gpi payment. It travels with the payment through every correspondent bank in the chain. Finance teams use it to track status in real time rather than waiting days for confirmation.

![]()

What information do you need to initiate a SWIFT payment?

Every SWIFT payment requires a precise set of data fields. Missing or incorrect information causes delays, rejections, or funds landing in the wrong account. Banks run compliance checks, including KYC and AML screening, before releasing any international transfer.

Here are the required data fields and their purpose:

| Data Field | Purpose |

|---|---|

| Beneficiary full legal name | Identifies the recipient for compliance screening |

| Beneficiary bank name and address | Routes the payment to the correct institution |

| Account number or IBAN | Pinpoints the exact account receiving funds |

| SWIFT/BIC code | Identifies the beneficiary’s bank on the SWIFT network |

| Payment amount and currency | Defines the transaction value and FX requirements |

| Payment purpose or reference | Supports AML compliance and reconciliation |

| Correspondent bank details (if required) | Needed when no direct banking relationship exists |

Your bank will also require documentation for larger transfers. This typically includes invoices, contracts, or proof of business relationship. The compliance layer is not optional. Banks that skip KYC and AML checks face regulatory penalties, so expect your payment to be held if documentation is incomplete.

Pro Tip: Verify the beneficiary’s IBAN and BIC code before submitting any payment. A single transposed digit routes funds to the wrong account, and recovery can take weeks.

Payments route through multiple correspondent banks when a direct banking relationship does not exist between the sending and receiving institutions. Treasury teams need to anticipate this multi-step process and build in extra time for high-value transfers.

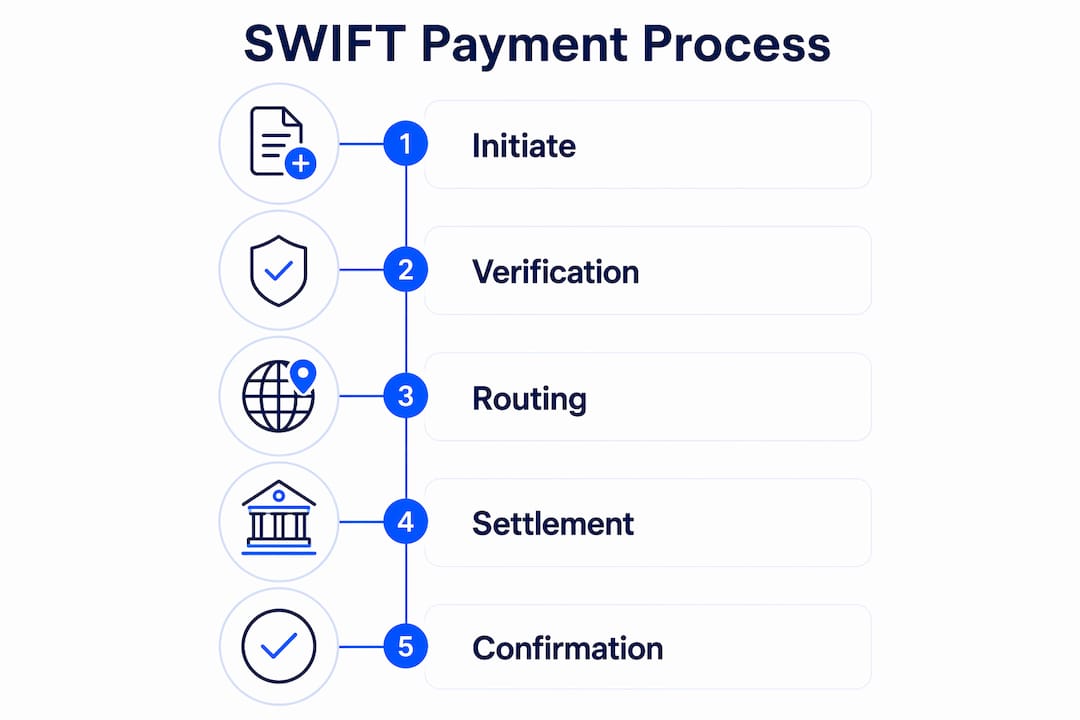

How does the SWIFT payment process work step by step?

The SWIFT payment process follows a defined sequence from initiation to credit. Each step involves specific message types and compliance checkpoints.

- Initiate the payment. You submit payment details through your bank’s portal or a regulated fintech platform. The bank validates the data against its compliance rules before proceeding.

- Message creation. Your bank constructs a structured payment message. Under ISO 20022, this is a pacs.008 message for customer credit transfers, replacing the older MT103 format. The MT103 maps to pacs.008, and MT202 maps to pacs.009 for interbank transfers.

- Routing through correspondent banks. If your bank has no direct relationship with the recipient’s bank, the message routes through one or more correspondent banks. Each correspondent debits and credits its own accounts to move value along the chain.

- Compliance screening at each node. Every bank in the chain runs its own AML and sanctions screening. A flag at any point pauses the payment until resolved.

- Credit to the beneficiary. The receiving bank credits the beneficiary’s account and sends a confirmation back through the network.

- Confirmation to the sender. Your bank receives confirmation and updates your transaction record with the final status.

The ISO 20022 migration matters because the new format carries structured, machine-readable data. Fields like legal entity identifiers, purpose codes, and remittance information travel with the payment rather than being truncated. This reduces manual intervention and speeds up reconciliation on both ends.

Pro Tip: Always include a structured remittance reference in your payment instruction. Structured messages reduce the chance of a correspondent bank requesting additional information mid-route, which is one of the most common causes of delays.

For a deeper look at how SWIFT flows work for European businesses, the SWIFT payment guide for SMEs at Demivolt covers routing specifics and timing benchmarks worth reviewing.

How can you track and troubleshoot a SWIFT payment?

Tracking a SWIFT payment starts with the MT103 confirmation or its ISO 20022 equivalent. Efficient tracking begins with the MT103 and the UETR embedded in Field 121. That reference number is your master key for every status inquiry.

Here is what to do at each stage:

- Request the MT103 copy immediately after sending. This document contains the UETR, the sending bank’s reference, and the full payment chain details.

- Use the UETR to query status. Banks with SWIFT gpi access can look up the payment in the gpi Tracker. The UETR remains constant even if internal bank references change during processing.

- Check your bank’s tracking portal. Most major banks expose gpi status data through their corporate banking portals. Status codes tell you whether the payment is pending, in transit, or credited.

- Initiate a formal investigation if the payment is delayed beyond the expected settlement window. Your bank files a gpi inquiry, and SWIFT gpi requires every bank in the chain to update tracking at each step. This creates a clear audit trail rather than a dead end.

- Escalate with documentation. Provide the UETR, MT103 copy, and beneficiary details together. Incomplete inquiry requests slow resolution significantly.

The UETR remains constant throughout the entire payment journey, even as internal bank references change at each correspondent node. That consistency is what makes it the single most useful tool for finance teams managing exceptions.

Pro Tip: Keep a transaction log with the UETR, sending date, amount, beneficiary bank, and expected settlement date for every outgoing SWIFT payment. When a payment goes missing, this log cuts investigation time from days to hours.

What are the benefits and limitations of SWIFT payments?

SWIFT payments offer global reach that no regional payment rail can match. The network connects 11,000+ institutions across more than 200 countries. Security, standardization, and traceability through gpi make SWIFT the default choice for high-value corporate transfers.

The cost structure deserves attention. SWIFT payment costs include sending bank fees, correspondent transit fees of $10–$30 each, foreign exchange spreads typically between 1.5% and 3%, and receiving bank fees. Multiple correspondents in the chain compound these costs. A payment routed through three correspondent banks can lose $60–$90 in transit fees alone before FX spread is applied.

| Factor | SWIFT Payments | Alternative Rails (SEPA, Fintech Platforms) |

|---|---|---|

| Geographic reach | 200+ countries, 11,000+ banks | Regional or limited corridors |

| Speed | 1–5 business days typical | Same-day to 24 hours for SEPA |

| Cost per transaction | $15–$50+ depending on routing | Often lower or flat fee |

| Traceability | Full gpi tracking with UETR | Varies by provider |

| Best use case | High-value, cross-currency transfers | Intra-EU or high-frequency low-value payments |

SWIFT is the right tool for large, cross-currency transfers where traceability and global reach matter more than speed or cost. For intra-EU euro payments, SEPA is faster and cheaper. For high-frequency low-value transfers, fintech platforms often provide better economics. Understanding how international money transfers work across different rails helps you choose the right method for each payment type.

Key takeaways

SWIFT payments work because they combine standardized messaging, global bank connectivity, and end-to-end tracking through UETR to give businesses a reliable, auditable path for cross-border transfers.

| Point | Details |

|---|---|

| SWIFT is a messaging network | It transmits payment instructions; your bank moves the actual funds. |

| ISO 20022 is now mandatory | Since november 2025, all cross-border SWIFT payments use pacs.008 and pacs.009 formats. |

| UETR is your tracking anchor | Extract it from every MT103 or pacs.008 confirmation and log it immediately. |

| Costs compound with correspondents | Each correspondent bank adds $10–$30 in fees; minimize hops where possible. |

| SWIFT suits high-value transfers | For intra-EU or low-value payments, SEPA or fintech rails offer better speed and cost. |

Why most finance teams underuse the tools SWIFT already gives them

After years of working with cross-border payment flows, the pattern I see most often is this: finance teams treat SWIFT as a black box. They send the payment, wait, and only act when something goes wrong. That is the wrong posture.

The UETR system exists precisely to give you visibility at every step. Yet most finance teams do not extract and log the UETR at the moment of payment confirmation. They scramble for it later when a payment goes missing. Building a simple transaction log, even a spreadsheet, with the UETR, beneficiary bank, and expected settlement date changes your exception management from reactive to proactive.

The ISO 20022 migration is another area where businesses are leaving value on the table. The new format carries structured remittance data that older MT messages truncated. If your ERP or accounting system can consume ISO 20022 data, you can automate reconciliation instead of matching payments manually. That is a real operational gain, not a theoretical one.

My honest advice: treat SWIFT payment setup as a compliance and data quality problem first, and a speed problem second. Errors in beneficiary data cause far more delays than correspondent bank routing. Validate every IBAN and BIC before submission. Use the SWIFT transfers guide for global businesses at Demivolt to cross-reference your process against current best practices.

The businesses that manage SWIFT payments well are not the ones with the fastest banks. They are the ones with the cleanest data and the most disciplined tracking habits.

— dd

How Demivolt supports your cross-border payment operations

Errors in beneficiary account data are the leading cause of SWIFT payment delays. Demivolt’s free IBAN validation tool checks account numbers against ISO 13616 standards before you submit a payment, catching formatting errors before they reach the banking network.

Demivolt’s business banking platform supports both SEPA and SWIFT payments from a single dedicated IBAN account, with role-based user access and full transaction records for compliance purposes. For finance teams managing cross-border payments across multiple currencies, Demivolt’s free payment tools cover validation, compliance checks, and account management in one place. If you are setting up or reviewing your international payment infrastructure, Demivolt is built for exactly that operational context.

FAQ

What is SWIFT and how does it work for businesses?

SWIFT is a global messaging network that transmits standardized payment instructions between banks. It does not move money directly; your bank executes the transfer based on the SWIFT message it receives.

What is a UETR and why does it matter?

A UETR is a 36-character Unique End-to-End Transaction Reference embedded in every SWIFT gpi payment. It stays constant across the entire payment chain, making it the primary tool for tracking and investigating cross-border transfers.

What changed with the ISO 20022 migration in 2025?

Since november 22, 2025, SWIFT requires ISO 20022 format for all cross-border payments, replacing MT103 and MT202 with pacs.008 and pacs.009. The new format carries richer structured data, which improves automation and reconciliation for businesses.

How much does a SWIFT payment cost?

A typical SWIFT payment includes sending bank fees, correspondent transit fees of $10–$30 per bank, FX spreads of 1.5%–3%, and receiving bank fees. Payments routed through multiple correspondents accumulate these charges at each step.

When should a business use SWIFT instead of SEPA?

SWIFT is the right choice for cross-currency transfers or payments outside the EU where SEPA is not available. For euro-denominated payments within the EU, SEPA is faster and significantly cheaper.

Recommended

- Demivolt | Blog – SEPA vs SWIFT: Choosing the right payment rails for SMEs

- Demivolt | Blog – Business payments checklist: compliance & cash flow 2026

- Demivolt | Blog – SWIFT transfers explained: a complete guide for global businesses

- Demivolt | Blog – SWIFT payment guide: faster transfers for European SMEs