TL;DR:

- Digital-first finance emphasizes digital technologies and platforms to optimize all financial operations in modern businesses. It enhances operational efficiency, expands financial inclusion, and strengthens compliance through automation and real-time data analytics. Successful adoption depends on trust, literacy, and effective leadership, with CFOs now leading digital transformation and strategy.

Digital-first finance is the practice of prioritizing digital technologies and platforms to conduct, manage, and optimize all financial operations in modern business environments. This approach, also called digital financial services in regulatory and academic contexts, integrates mobile banking, fintech platforms, cloud infrastructure, and real-time analytics into a single operating model. The role of digital-first finance extends well beyond payment processing. It reshapes how CFOs lead, how SMEs access capital, and how organizations build compliance into daily workflows rather than treating it as an afterthought. For entrepreneurs and business leaders, understanding this shift is the difference between reacting to change and directing it.

What are the main benefits of digital-first finance for businesses?

Digital-first finance delivers three measurable advantages: operational efficiency, broader accessibility, and tighter compliance. Each one compounds the others, which is why leaders who adopt all three together outperform those who treat them as separate initiatives.

Operational efficiency through automation and real-time data

Digital finance systems generate large volumes of real-time data that improve financial planning, forecasting, and risk management when combined with analytics. That means your finance team stops working from last month’s spreadsheet and starts making decisions on what happened this morning. Automated reconciliation, instant payment confirmation, and cloud-based ledgers cut the manual labor that traditionally consumed 30 to 40 percent of a finance team’s week. The practical result is faster close cycles, fewer errors, and more time spent on analysis rather than data entry.

Accessibility and financial inclusion

Digital financial services enable higher financial inclusion, though outcomes depend on supportive policy, suitable design, and collaboration between providers and regulators. For business leaders, this matters because it expands your customer base and supplier network. SMEs that previously lacked access to trade finance, cross-border payments, or credit scoring now participate in global commerce through fintech platforms. Demivolt’s approach of offering dedicated IBAN accounts and SEPA payment infrastructure to European businesses is a direct example of how digital financial infrastructure removes barriers that once required a full-service bank relationship.

Compliance and risk management

Integrated digital tools embed compliance checks at the transaction level rather than at the audit level. Know Your Customer (KYC) verification, anti-money laundering (AML) screening, and regulatory reporting become automated outputs of normal operations rather than separate compliance projects. This reduces both the cost and the risk of regulatory failure.

- Real-time data analytics cuts forecasting cycle times and improves accuracy

- Automated KYC and AML tools reduce compliance overhead

- Digital payment rails expand market reach for SMEs and cross-border operators

- Cloud-based financial infrastructure scales without proportional cost increases

- Integrated risk dashboards give leadership earlier warning of exposure

Pro Tip: Link your analytics cadence directly to decision points. Collecting more data without redesigning when and how decisions get made produces reports, not results.

What drives digital finance adoption and what challenges do leaders face?

Adoption of digital financial services does not happen automatically when technology becomes available. Research consistently identifies behavioral and structural factors that determine whether a business or its customers actually use what is deployed.

The evidence is specific. Trust and financial literacy strongly predict adoption and improve digital inclusion and economic growth outcomes. A study of 444 respondents found that trust mediates the relationship between digital finance adoption and sustainable development indicators. That finding has a direct implication for business leaders: if your team or your customers do not trust the platform, adoption stalls regardless of how good the technology is.

Performance expectancy and facilitating conditions positively affect user adoption intention for digital financial channels, while social influence can reduce it. A study of 674 users confirmed these factors shape behavioral intention. In practice, this means users adopt digital finance when they believe it will make their work easier and when the supporting infrastructure (training, IT support, clear processes) is in place.

The barriers are equally well documented. Access alone does not guarantee benefits. Digital financial illiteracy, regulatory constraints, and socio-economic disparities require policy alignment and active user enablement. For leaders running cross-border operations, this is not an abstract concern. It shows up as low adoption rates in new markets, compliance gaps in jurisdictions with different regulatory frameworks, and customer drop-off during onboarding.

Here is a practical sequence for managing adoption in your organization:

- Audit current financial literacy levels across your team before deploying new platforms. Identify who needs structured training versus who needs documentation.

- Communicate performance benefits explicitly. Show users how the new system reduces their specific workload, not just the organization’s costs.

- Build facilitating conditions first. Deploy IT support, clear escalation paths, and user guides before go-live, not after.

- Invest in trust-building through transparency. Publish your data handling practices, explain how funds are safeguarded, and make error resolution fast and visible.

- Monitor adoption metrics weekly for the first 90 days. Low adoption in week two is a solvable problem. Low adoption in month six is a cultural one.

Pro Tip: Successful digital finance rollout requires evidence-based engagement strategies focused on trust-building and clear benefits messaging. Frame the change in terms of what the user gains, not what the organization saves.

How does digital-first finance reshape leadership roles?

The CFO role has changed more in the past five years than in the previous two decades. Digital transformation is the primary driver, and the data is unambiguous. 53% of CFOs now lead digital transformation at their organizations, 40% oversee risk management, and 87% report expanded expectations tied to AI integration. CFOs have become orchestrators of strategy, technology, and compliance simultaneously.

This shift changes the operating model, not just the job description. Fixed annual budgets give way to rolling forecasts updated with real-time payment and revenue data. Finance chiefs at companies like those tracked in Demivolt’s payments data analysis now use transaction-level data to track consumer behavior faster than traditional employment or GDP metrics allow. That is a structural advantage in volatile markets.

The table below summarizes how CFO responsibilities have expanded under digital-first finance models.

| Traditional CFO responsibility | Expanded digital-first responsibility |

|---|---|

| Financial reporting and compliance | Real-time risk monitoring and regulatory automation |

| Annual budget management | Agile, data-driven rolling forecasts |

| Cost control and audit oversight | Digital transformation ownership and AI integration |

| Treasury and cash management | Cross-border payment infrastructure and IBAN management |

| Investor relations | Strategic technology partnership and fintech ecosystem governance |

Digital-first finance is as much an operating model change as a technology upgrade, and leaders who treat it as purely an IT project consistently underdeliver. The CFO who owns the vision, the data architecture, and the compliance framework is the one who creates durable competitive advantage.

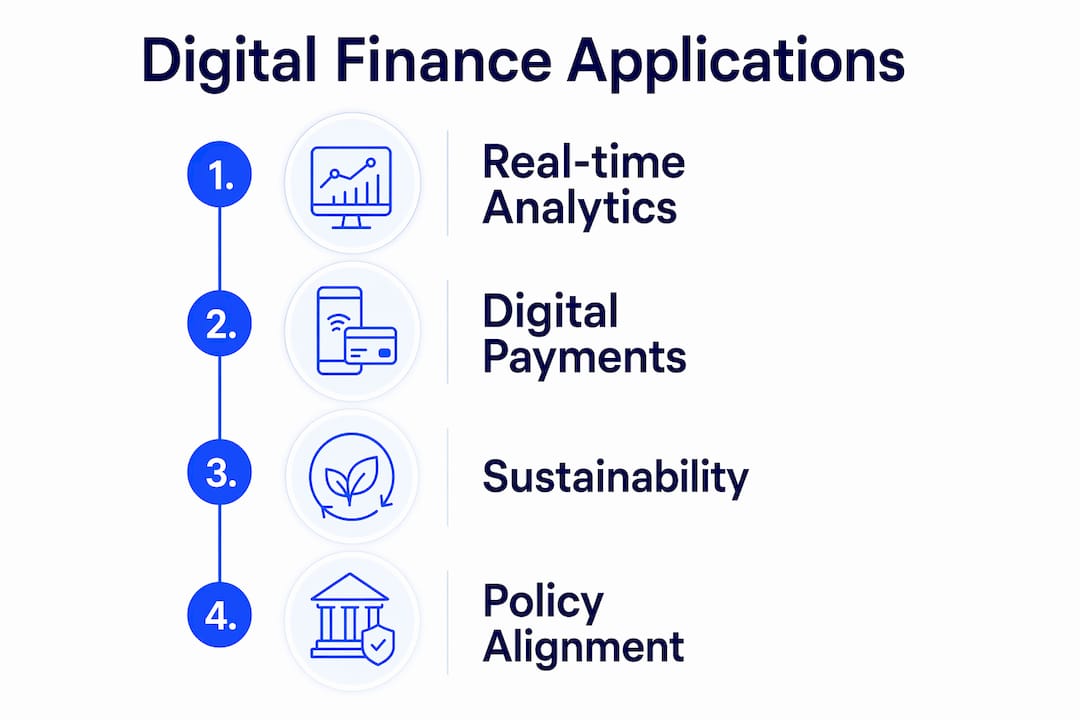

What are the practical applications and future directions?

The impact of digital finance on business operations is measurable across four distinct application areas. Each one offers a concrete entry point for leaders who want to move from strategy to execution.

Real-time analytics for forecasting. Finance teams using cloud-based platforms can close books in days rather than weeks, run scenario models against live data, and adjust capital allocation mid-quarter. The fintech influence on digital commerce shows how real-time data converts from a reporting tool into a planning engine.

Digital payment systems expanding reach. Cross-border payment infrastructure, including SEPA and SWIFT rails, allows SMEs to operate internationally without the overhead of multiple banking relationships. Demivolt’s multi-account IBAN structure is built specifically for this use case.

Sustainability trade-offs. High utilization of digital payments correlates with reduced income inequality and increased consumption but also associates with higher CO2 emissions across 25 Asian countries studied. This finding matters for leaders building ESG reporting frameworks. Digital finance improves inclusion metrics but requires explicit carbon accounting to avoid greenwashing.

Policy alignment as a growth lever. The future of digital finance depends on regulatory environments that support innovation without sacrificing consumer protection. Leaders who engage with regulatory developments in the EU, including PSD3 and open banking mandates, position their organizations ahead of compliance requirements rather than behind them.

| Application area | Primary business benefit |

|---|---|

| Real-time analytics | Faster, more accurate forecasting and capital allocation |

| Digital payment rails | Cross-border reach without multi-bank overhead |

| Automated compliance tools | Lower regulatory risk and reduced audit costs |

| Financial inclusion infrastructure | Expanded customer and supplier networks |

| ESG-linked digital finance | Measurable inclusion impact with carbon accountability |

Key takeaways

Digital-first finance transforms business operations by integrating real-time data, automated compliance, and digital payment infrastructure into a single operating model that CFOs must own and lead.

| Point | Details |

|---|---|

| Real-time data drives decisions | Analytics must connect directly to decision points, not just reporting cycles. |

| Trust determines adoption | Financial literacy and transparent service behavior are prerequisites for successful rollout. |

| CFO role has expanded | 53% of CFOs now lead digital transformation, owning strategy, risk, and technology together. |

| Inclusion requires active enablement | Access to digital finance does not automatically produce benefits without literacy and policy support. |

| Sustainability needs measurement | Digital payments improve inclusion but can increase carbon emissions, requiring explicit ESG accounting. |

Why digital finance is a leadership test, not a technology project

Most articles on digital finance focus on the tools. I want to focus on the decision that precedes every tool selection: whether your leadership team actually owns the outcome or just sponsors the project.

I have watched organizations deploy sophisticated fintech platforms and see adoption rates below 30% at the six-month mark. The technology worked. The change management did not. The CFO signed off on the budget but handed execution to IT. The result was a capable system that nobody trusted and few people used correctly.

The research on trust and literacy as adoption drivers confirms what experienced operators already know: digital finance is a people problem wearing a technology costume. You can have the best IBAN infrastructure, the cleanest compliance automation, and the fastest payment rails in your industry. If your team does not understand why the system works the way it does, or if they do not trust that their data is handled responsibly, they will find workarounds.

The leaders who get this right treat digital finance as a continuous investment in literacy and trust, not a one-time implementation. They redesign decision cadences so that real-time data actually changes what gets decided and when. They measure adoption as rigorously as they measure cost savings. And they stay personally involved in the compliance and risk dimensions rather than delegating them entirely.

Financial discipline is not the opposite of digital innovation. It is the condition that makes innovation sustainable. The organizations building durable advantage in digital finance are the ones where the CFO and the CEO share a single, clear answer to the question: what does this platform allow us to decide faster and better than we could before?

— dd

How Demivolt supports your digital finance operations

Demivolt is a regulated European fintech platform built for businesses that need compliant, digital-first financial infrastructure without the complexity of traditional banking. The platform provides dedicated IBAN accounts, SEPA and SWIFT payment management, virtual and physical business cards, and role-based user controls designed for cross-border and SME operations. For leaders focused on compliance accuracy, Demivolt’s free IBAN validation tool checks account numbers against ISO 13616 standards before payments are processed, eliminating a common source of costly errors. You can also explore the full SEPA tools suite to support payment compliance across EU markets. If you are building or refining your digital banking workflow, Demivolt’s infrastructure is designed to grow with your operational requirements.

FAQ

What is digital-first finance?

Digital-first finance is the practice of using digital technologies, including mobile banking, fintech platforms, and cloud services, as the primary infrastructure for managing all financial operations. It prioritizes real-time data, automation, and integrated compliance over legacy paper-based or branch-dependent processes.

What are the main benefits of digital-first finance for SMEs?

The core benefits are operational efficiency through automation, broader market access via digital payment rails, and lower compliance costs through integrated KYC and AML tools. SMEs using digital financial services can access cross-border payment infrastructure and credit tools that previously required full-service banking relationships.

Why do some businesses struggle with digital finance adoption?

Digital financial illiteracy, regulatory barriers, and socio-economic disparities are the primary obstacles. Access to the technology is necessary but not sufficient. Trust in the platform and financial literacy among users are the factors that most reliably predict whether adoption translates into actual business impact.

How has the CFO role changed under digital-first finance models?

CFOs now function as orchestrators of digital transformation, risk management, and compliance strategy. 87% of CFOs report expanded expectations tied to AI integration, and more than half lead digital transformation directly rather than delegating it to technology teams.

Does digital finance have sustainability implications?

Yes. Research across 25 Asian countries found that high digital payment utilization reduces income inequality but also associates with higher CO2 emissions. Leaders building ESG frameworks need to account for the carbon footprint of digital payment infrastructure alongside its inclusion benefits.

Recommended

- Demivolt | News – How Fintech Is Influencing the Future of Digital Commerce

- Demivolt | Blog – Why digital banking empowers SMEs for smarter cross-border finance

- Demivolt | News – The Rise of Fintech Platforms and the New Digital Financial Ecosystem

- Demivolt | News – Ecuador’s Fintech Sector Gains Momentum Amid Digital Transformation Push