TL;DR:

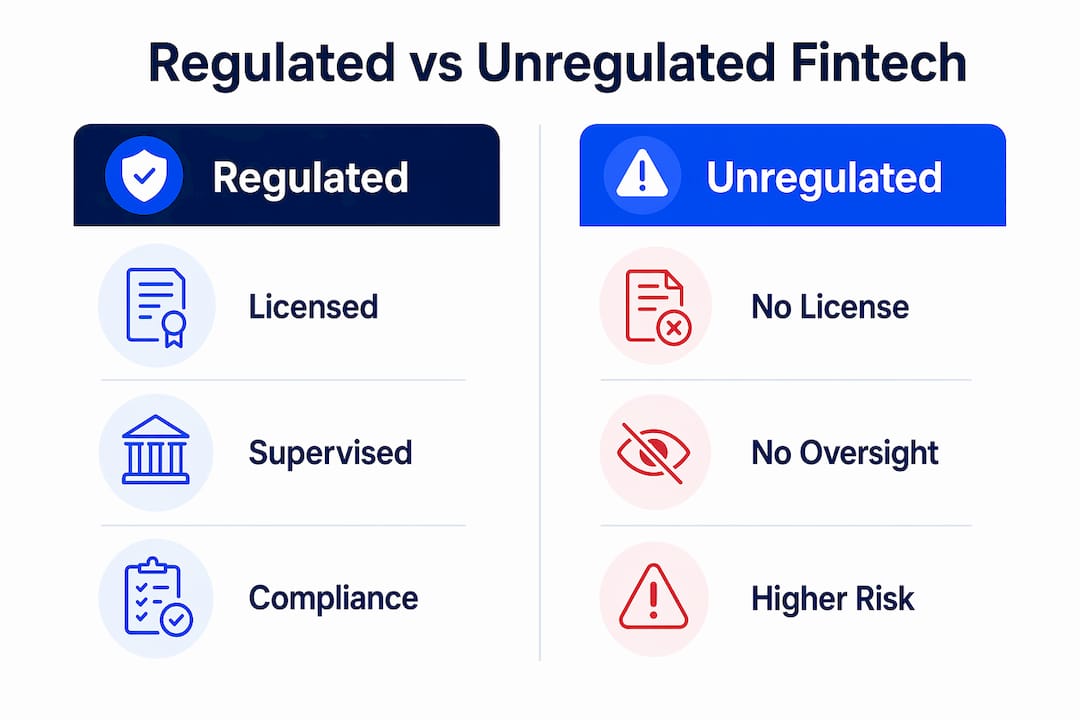

- Regulated fintech firms operate under formal licenses and supervisory oversight, reducing legal and operational risks for businesses.

- Understanding compliance obligations, including KYC, AML, and transaction monitoring, is essential for maintaining regulatory standards and resilience.

Most business owners assume that if a company looks like a bank, it operates like a bank under the law. Regulated fintech, or more precisely what the industry calls a licensed financial technology firm, proves that assumption dangerously incomplete. What is regulated fintech, exactly? It’s a fintech company that provides or supports financial products and services under formal regulatory oversight, including licensing, compliance obligations, and supervisory scrutiny. Understanding this distinction matters for your business because the fintech partner you choose determines your exposure to fraud, legal liability, and operational risk.

Key takeaways

| Point | Details |

|---|---|

| Regulated fintech is licensed | These firms operate under formal financial licenses and supervisory oversight, not just tech permits. |

| Compliance covers multiple layers | KYC, AML, sanctions screening, and transaction monitoring are required, not optional. |

| EU and U.S. frameworks differ significantly | DORA, PSD3, and eIDAS 2.0 shape EU obligations, while the U.S. has a fragmented multi-agency structure. |

| Choosing regulated fintech reduces risk | Unregulated fintech exposes your business to fraud, fund loss, and legal liability. |

| Technology drives modern compliance | Modular compliance engines and RegTech automation handle the volume that manual processes cannot. |

What is regulated fintech and how it works

The clearest working definition comes directly from U.S. federal policy. The White House defines a fintech firm as a non-bank company providing or supporting financial products such as payment processing, lending, digital banking, custodial services, and blockchain-based services. Regulated fintech firms sit within that definition while also operating under formal licensing and supervisory oversight from financial authorities.

The critical distinction is between the technology layer and the financial activity layer. A software company building a payments interface is not automatically regulated. The moment that company accepts funds, holds deposits, issues credit, or executes transactions on behalf of customers, it crosses into regulated territory. That line is where regulatory classification gets product-specific and jurisdiction-dependent, making regulatory mapping one of the more complex exercises a fintech business undertakes.

The core compliance obligations that apply to regulated fintech firms include:

- Identity verification (KYC): Confirming who your customers are before they access financial services, including document checks and biometric matching

- Transaction monitoring: Ongoing surveillance of payment activity to detect anomalies and suspicious patterns in real time

- Sanctions screening: Checking customers and counterparties against government-issued sanctions lists before processing any transaction

- AML controls: Anti-money laundering programs that assess risk, investigate alerts, and file reports with financial intelligence units

- Regulatory reporting: Structured disclosures to supervisory bodies covering transaction volumes, suspicious activity, and capital adequacy

RegTech automates these functions to handle the data volumes that manual compliance processes simply cannot keep pace with. For a company processing tens of thousands of transactions per day, automated compliance is not a luxury. It’s the only viable approach.

Pro Tip: When evaluating a fintech partner, ask specifically which regulatory license they hold and who supervises them. “We comply with regulations” is not the same as “we are licensed by [authority] and subject to their ongoing supervision.”

The regulatory landscape: U.S. and EU frameworks

No single global standard governs regulated fintech. Your compliance obligations depend heavily on where you operate, where your customers are located, and what financial activities you conduct. The two most consequential regulatory environments are the United States and the European Union, and they work very differently.

The U.S. regulatory structure

The U.S. approach is fragmented by design. Multiple federal agencies share oversight of fintech activity, and state-level money transmitter licenses add another layer. The key agencies include the Consumer Financial Protection Bureau (CFPB) for consumer-facing financial products, the SEC for securities and investment activities, the FDIC and OCC for banking activities, and the CFTC for derivatives and commodities. The 2026 White House executive order on fintech regulatory integration is pushing agencies toward clearer frameworks, but the multi-agency structure still means a single fintech company may need licenses from several authorities simultaneously.

EU compliance for fintech in 2026

The EU has moved decisively toward harmonization. Several major frameworks now define what EU compliance for fintech looks like in practice:

| Framework | Scope | Key Requirement |

|---|---|---|

| DORA | ICT risk and operational resilience | Harmonized digital resilience standards for all financial entities |

| PSD3 / PSR | Payments and open banking | Stronger fraud prevention, consent dashboards, and open access rules |

| eIDAS 2.0 | Digital identity | Unified EU digital identity wallet for customer verification |

| FiDA | Open finance data sharing | Regulated access to financial data beyond payment accounts |

The EU’s DORA regulation became fully applicable in January 2025, covering payment institutions, e-money institutions, and critically, their third-party ICT providers. This means DORA compliance is not just an internal exercise. It extends to every cloud provider, software vendor, and data processor in your fintech partner’s supply chain. Gaps in third-party tracking can expose fintechs to regulatory risk under the EU framework, which means that risk flows downstream to you as their client.

PSD3 and FiDA are reshaping open finance with stronger fraud controls and consent management, while eIDAS 2.0 provides a unified digital identity layer across EU member states. For companies operating across borders within Europe, this convergence is significant. It means a single, standardized way to verify customers and share financial data with their consent, rather than navigating 27 different national systems. You can read more about how these regulations interact in the EU fintech regulatory landscape.

Technology and operations inside regulated fintech

Understanding what regulatory compliance in fintech demands operationally changes how you evaluate fintech partners. Compliance inside a regulated firm is not a department that reviews transactions after the fact. It is a continuously running, auditable system embedded into every layer of the technology stack.

Think of it as systems engineering rather than policy enforcement. Modern compliance expects continuous monitoring and evidence trails rather than static policy documents. U.S. fintech firms in highly supervised environments embed supervisory-grade evidence capture directly into automated deployment pipelines so that regulators can reconstruct any decision at any point in time.

Here is how that translates into practice for a regulated fintech firm’s technology architecture:

- Modular compliance engines: Many firms architect compliance as modular microservices orchestrating KYC, AML, and sanctions screening subsystems. Each module ingests event streams, applies rules or machine learning models, logs every decision, and retains the evidence chain end to end.

- Continuous compliance testing: Compliance becomes a living infrastructure embedded in delivery processes, not a one-time checklist. Obligations link to test cases, and test cases link to evidence. When regulations change, the system updates and re-verifies.

- Third-party ICT governance: Under DORA, every vendor relationship requires a documented inventory, contract review, and oversight plan. A regulated firm that cannot show you its vendor risk register is not operating at the expected standard.

- Deployment controls and audit trails: Code changes in regulated fintech environments go through multi-step approval gates. Every deployment is logged with timestamps, approver identities, and rollback procedures in case a regulator asks what changed and when.

Pro Tip: When a fintech vendor talks about their “compliance system,” ask whether it is continuous and automated or a periodic manual review. The answer tells you a great deal about their actual regulatory maturity.

Compliance checklist and why regulated fintech matters for your business

Choosing a fintech partner is a compliance decision, not just a product decision. The role of compliance in fintech is not to slow things down. It is to protect your business, your customers’ funds, and your reputation. When a fintech partner fails a regulatory audit or loses its license, clients face frozen accounts, delayed payments, and potential legal exposure.

Here is a practical compliance checklist for fintechs and for businesses evaluating them:

- Confirmed financial license from a recognized supervisory authority (FCA, BaFin, De Nederlandsche Bank, or equivalent)

- Published AML policy and evidence of ongoing transaction monitoring programs

- Active KYC process covering customer onboarding and periodic review

- Sanctions screening against current OFAC, EU, and UN consolidated lists

- Segregated client accounts so customer funds are legally separate from operating capital

- Documented ICT risk and vendor management program

- Clear regulatory reporting procedures with named compliance officer

The benefits of choosing a regulated fintech partner extend beyond legal protection. Regulated firms carry professional indemnity insurance, maintain capital adequacy requirements, and must meet audit standards that keep their operations at a documented level of reliability. You can explore how AI is transforming one critical compliance area in this sanctions compliance guide from Demivolt.

Unregulated fintech alternatives may offer lower fees or faster onboarding, but the trade-off is real. Without supervisory oversight, there is no independent check on whether your funds are segregated, whether your counterparties are screened, or whether the company maintains adequate capital to return your money if something goes wrong. For cross-border payment operations in particular, that risk compounds quickly. A solid payments compliance checklist will help you identify these gaps before they become problems.

My take on regulated fintech’s real complexity

I’ve watched too many businesses treat regulated fintech as a binary category. Either a company is compliant or it isn’t. The reality I’ve seen is far more granular, and far more consequential.

What I’ve learned from working through these frameworks is that the regulatory perimeter shifts based on the specific product, the customer type, and the jurisdiction. A fintech firm can be fully licensed for e-money services and completely unlicensed for securities custody. Those are different regulated activities, and using one to vouch for the other is how businesses get burned.

The businesses that handle this best treat regulatory status as an ongoing due diligence question, not a one-time check at onboarding. They ask about license scope, they read the regulatory filings, and they understand what supervisory body has actual enforcement power over their fintech partner. That approach requires some effort, but it is far less expensive than the alternative.

What I find genuinely promising about the current direction is that continuous compliance technology is making it easier to maintain that standard without a large internal compliance team. The firms building compliance as living infrastructure embedded in delivery are creating a structural advantage over those treating it as a reporting exercise. Over time, that gap will separate the durable fintech platforms from the ones that get caught short when regulators update expectations.

— dd

How Demivolt supports your compliance needs

Demivolt is a regulated European fintech platform built specifically for businesses that need financial infrastructure they can depend on. Every account comes with a dedicated IBAN, full SEPA and SWIFT payment coverage, and client funds held in segregated accounts under EU regulatory standards. Onboarding is built on a compliance-first model covering KYC and AML from day one, so your business is protected before the first transaction clears.

If you work with cross-border payments, start with Demivolt’s free IBAN validator tool to catch account errors before they delay payments. For a full picture of Demivolt’s SEPA-compliant payment tools and regulated banking services, visit the platform directly at Demivolt.

FAQ

What is regulated fintech in simple terms?

A regulated fintech firm is a non-bank technology company that provides financial services under a formal license and ongoing supervision from a financial authority. This means it must meet compliance standards for KYC, AML, and fund segregation.

What does regulatory compliance in fintech require?

Regulatory compliance in fintech requires identity verification, transaction monitoring, sanctions screening, AML controls, and regular reporting to supervisory bodies. Many firms use automated RegTech systems to meet these requirements at scale.

Why does EU compliance for fintech matter to my business?

EU compliance frameworks like DORA, PSD3, and eIDAS 2.0 set mandatory standards for operational resilience, digital identity, and data sharing. If your fintech partner operates in the EU, these rules directly affect how your payments are processed and how your data is protected.

What is the role of compliance in fintech operations?

Compliance in fintech is not a back-office function. It is a continuously running system of controls embedded in the technology stack, covering everything from customer onboarding to real-time payment monitoring and third-party vendor oversight.

What happens if I use an unregulated fintech service?

Without regulatory oversight, there is no independent guarantee that your funds are segregated, your transactions are monitored for fraud, or the company holds adequate capital. Your business assumes all of the risk that regulated supervision would otherwise manage.

Recommended

- Demivolt | Blog – EU Fintech Landscape Explained for Investors and Professionals

- Demivolt | News – How Fintech Innovation Is Transforming the Global Financial System

- Demivolt | News – How Fintech Is Reshaping the $300 Trillion Global Financial Services Industry

- Demivolt | News – The Rise of Fintech Platforms and the New Digital Financial Ecosystem