TL;DR:

- Business expense cards enforce real-time spending limits and merchant restrictions to prevent budget violations. They reduce administrative workload, enhance fraud prevention, and streamline expense tracking by integrating directly with accounting systems. Implementing these cards fosters proactive financial management, especially beneficial for small and medium-sized enterprises.

Most business owners discover a spending problem the same way: a month-end bank statement that doesn’t match expectations. Someone bought software on a personal card, someone else exceeded their travel budget, and now your finance team is chasing receipts at 11 PM. Understanding why use business expense cards matters because they fix this problem at the source, before the spend happens, not after. This article breaks down how they work, what they cost you in admin time if you skip them, and how to roll them out without making common implementation mistakes.

Table of Contents

- Key takeaways

- Why use business expense cards: what they are and how they work

- Benefits of business expense cards for SMEs

- Technology features that make expense cards powerful

- How to implement expense cards in your SME

- My take on what expense cards actually change

- Take control of company spending with Demivolt

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Real-time spend control | Expense cards enforce spending limits and merchant restrictions at the moment of purchase, not at month-end. |

| Reduced admin workload | Automating receipt capture and transaction categorization can cut manual administrative work by up to 80%. |

| Fraud prevention built in | Virtual card credentials and instant alerts significantly reduce the risk of unauthorized or fraudulent charges. |

| No more employee reimbursements | Tying cards directly to company funds eliminates the cash flow hit employees take when fronting personal money. |

| Integration is everything | Cards connected to your accounting software prevent reconciliation gaps and keep your books audit-ready. |

Why use business expense cards: what they are and how they work

Business expense cards are payment cards issued directly by a company to its employees for work-related spending. They are not traditional corporate credit cards. The distinction matters more than most people realize.

A corporate credit card gives employees access to a credit line with relatively broad spending freedom and kicks most policy enforcement to month-end review. A business expense card, by contrast, is configured with controls that operate before a transaction clears. Think of it as spending policy written into the card itself.

Here are the main types you will encounter:

- Prepaid expense cards. Loaded with a set amount of company funds. When the balance is gone, the card declines. No credit risk, no overspending beyond what was loaded.

- Virtual cards. Digital card numbers generated for single use or specific vendors. Ideal for online subscriptions, vendor payments, and any situation where physical card exposure creates risk.

- Physical debit-linked cards. Connected to a business bank account with configurable controls, typically used by employees with recurring travel or operational spend.

What separates expense cards from the old reimbursement model is the flow of money. With reimbursement, the employee fronts cash on a personal card, submits a report, and waits. Cards tied to company funds remove that friction entirely. The company’s money moves at the moment of purchase, and the controls ensure it moves within policy. Modern platforms also connect directly to accounting systems, tagging each transaction with the right general ledger code and project reference at the time of purchase.

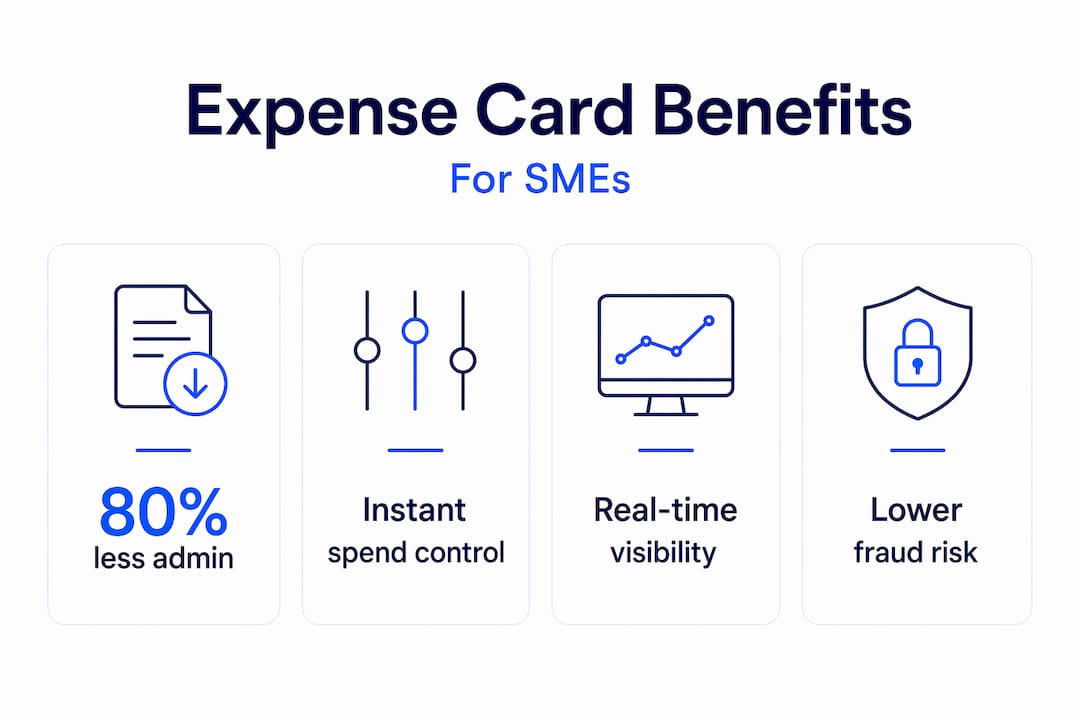

Benefits of business expense cards for SMEs

The advantages of using expense cards are clearest when you measure what the alternative actually costs. Manual expense management is not just inefficient. It is expensive in finance team hours, late payments, and the policy violations that slip through because nobody caught them in time.

Real-time visibility replaces month-end surprises. Spending limits and merchant restrictions enforce policy continuously, not in retrospect. Your finance manager sees every transaction as it happens through a live dashboard, broken down by employee, department, or project.

Automatic policy enforcement. If a card is configured to block purchases outside approved merchant categories, that block happens at the point of sale. There is no gray area, no awkward conversation after the fact, and no expense report submitted with a policy exception buried in the notes.

Reduced administrative overhead. AI-powered receipt automation can reduce manual administrative workload by up to 80% for SMEs. That is not a rounding error. For a small finance team handling dozens of expense reports per month, this is the difference between a two-day close and a two-week close.

No more expense reimbursements. Expense cards capture receipts and block violations before they become documentation gaps. Employees stop fronting personal money, and the company stops losing track of who is owed what.

Fraud risk reduction. This one is underrated. Static card credentials shared across a team are a liability. Non-reusable virtual card credentials combined with instant alerts dramatically cut exposure to unauthorized charges.

Pro Tip: Configure separate cards by role or spend category rather than issuing one card per employee with broad permissions. A travel card for road warriors should look very different from an office supply card for your operations team.

Technology features that make expense cards powerful

The benefits above only materialize if the card program is backed by the right technology. The card itself is just plastic or a 16-digit number. What does the work is the platform behind it.

Configurable controls at the point of sale

Smart card platforms deliver spending limits by employee, category, and time period, with limits that renew daily, weekly, or monthly. A sales rep’s entertainment budget resets every week automatically. A contractor’s card is locked to a single merchant. These controls replace the policy document nobody reads with rules the card enforces on its own.

AI-driven receipt capture and categorization

Modern expense card platforms use optical character recognition and machine learning to read receipts the moment a photo is uploaded. The system matches the receipt to the transaction, assigns the correct expense category, and flags anything that looks off. Your team stops doing data entry and starts reviewing exceptions instead.

Accounting system integration

This is where the real time savings stack up. Cards connected to your ERP or accounting software push transactions directly into the right ledger accounts. Without pre-coded GL codes and linked approvals, businesses risk reconciliation gaps even when cards are working correctly. The integration is not optional if you want the full benefit.

Here is a quick comparison of what modern expense card platforms typically offer versus a basic corporate card:

| Feature | Basic corporate card | Modern expense card platform |

|---|---|---|

| Spending limits per employee | No | Yes, configurable by role |

| Merchant category restrictions | No | Yes, enforced at purchase |

| Real-time dashboard | No | Yes, per transaction |

| Accounting software sync | Manual export | Automated integration |

| Virtual card issuance | Rare | Standard |

| Receipt capture and matching | Manual | AI-powered |

Pro Tip: When evaluating platforms, ask specifically about the accounting integration depth. A card that syncs transaction amounts but not GL codes or project codes will still leave your team doing manual work at month-end.

The shift this technology enables is strategic. Finance teams move from reactive month-end policing to proactive management. They spend time analyzing spend patterns and advising budget holders, not reconciling spreadsheets.

How to implement expense cards in your SME

Rolling out a card program without preparation creates more problems than it solves. A few specific decisions upfront determine whether your team adopts it enthusiastically or works around it.

- Audit your current spend patterns first. Before choosing a provider, map out who spends what, on what categories, and how often. This tells you which controls matter most and which integrations are non-negotiable.

- Match the card type to the use case. Not every employee needs a physical card. Recurring SaaS subscriptions are better handled with dedicated virtual cards. Field teams need physical cards with travel merchant categories enabled.

- Define policies before configuring controls. The card enforces policy, so the policy needs to exist first. Document spending limits by role, approved merchant categories, and the approval process for exceptions.

- Train employees on receipt capture. The biggest compliance gap in most programs is not fraud. It is employees who forget to photograph receipts or submit them late. A 10-minute onboarding session on the mobile app eliminates most of this.

- Start narrow and expand. Launch with your highest-spend employees or departments, work out process kinks, then roll out to the rest of the organization. Do not flip the whole company on day one.

Comparison: reimbursement model vs. expense card program

| Factor | Reimbursement model | Expense card program |

|---|---|---|

| Policy enforcement | After the fact | Before purchase |

| Employee cash flow impact | Employee fronts money | No personal outlay |

| Finance close speed | Slow (receipt chasing) | Fast (auto-capture) |

| Fraud exposure | Higher (late detection) | Lower (real-time controls) |

| Admin time per transaction | High | Low |

P-cards eliminate purchase orders for routine small purchases by enforcing controls at the transaction level, which also speeds up procurement for operational teams. This is worth factoring into your cost-benefit analysis because the time savings extend beyond finance.

The most common pitfall is skipping the accounting integration. Teams that run cards without connecting them to their books still end up doing manual reconciliation. The card solved the spending control problem but created a new data entry problem. Check out how to issue business cards for SMEs for a practical walkthrough of the setup process.

My take on what expense cards actually change

I’ve seen businesses treat expense card adoption as a pure finance efficiency project, and I think that framing undersells what actually changes. Yes, your close cycle gets faster. Yes, you stop chasing receipts. But the more significant shift is what happens to the relationship between finance and the rest of the business.

When finance teams are no longer policing expenses after the fact, they stop being the department that sends uncomfortable emails asking for missing receipts. The card handles enforcement. Finance gets to spend that time on analysis: which departments are trending over budget, where procurement costs can be consolidated, which vendor contracts are worth renegotiating. That is a genuinely different job description, and it changes how the rest of the company perceives the finance function.

I have also watched businesses fall into the trap of setting up controls once and never revisiting them. A spending limit that made sense for a three-person sales team becomes a bottleneck when the team grows to fifteen. Policies need to be reviewed at least quarterly. The card is not a fire-and-forget tool.

The other thing I would push back on is the assumption that expense cards are a tool for large companies. An SME with ten employees and a mix of travel, software, and operational spend has more to gain proportionally than an enterprise with a dedicated AP team. The administrative burden hits smaller teams harder. Automating business payments at the SME level produces outsized returns precisely because every hour of finance time saved represents a higher percentage of total capacity.

Finally, do not underestimate the employee experience angle. Nobody enjoys fronting personal money for a business trip and waiting 30 days for reimbursement. Removing that friction is a small but real improvement to how people feel about working at your company.

— dd

Take control of company spending with Demivolt

If you are ready to move beyond spreadsheets and reimbursement chasing, Demivolt makes it straightforward. As a regulated European fintech platform, Demivolt lets SMEs issue virtual and physical business expense cards with configurable spending limits, merchant restrictions, and real-time dashboards. Every transaction is visible the moment it happens, and the platform integrates directly with your accounting setup to keep reconciliation clean.

You can open a dedicated IBAN account, manage SEPA and SWIFT payments, and configure role-based controls for every team member, all from one place. Demivolt is built for businesses that operate across borders and need financial infrastructure that keeps up. If your current setup still involves receipt folders and end-of-month surprises, explore Demivolt’s business banking to see what a modern expense management setup looks like.

FAQ

What is a business expense card?

A business expense card is a payment card issued to employees for work-related spending, with controls like spending limits and merchant restrictions configured by the company. Unlike corporate credit cards, these cards enforce policy at the point of purchase rather than after the fact.

How do expense cards differ from credit cards?

An expense card is typically linked directly to company funds with pre-set controls, while a corporate credit card extends a credit line with broader spending freedom and relies on month-end review for policy enforcement. Expense cards prevent unauthorized spending before it happens rather than flagging it afterward.

Are business expense cards suitable for small businesses?

Yes. An expense card for small business use is particularly valuable because small finance teams carry a disproportionate administrative burden. Automating receipt capture and enforcing spend limits frees up hours that smaller organizations simply cannot afford to waste.

Can expense cards reduce fraud risk?

Significantly. Virtual cards and real-time alerts reduce fraud exposure by eliminating reusable card credentials and flagging unusual transactions immediately. Merchant category restrictions also prevent cards from being used outside approved spending categories.

How does business expense tracking improve with expense cards?

Cards connected to accounting software push every transaction directly into the correct ledger account with the right categorization. Integration with accounting approval workflows prevents the reconciliation gaps that plague manual processes, making month-end close faster and audit records cleaner.