TL;DR:

- Most businesses treat banking as a utility, overlooking its layered, modular infrastructure and real-time capabilities. Understanding these components enables smarter vendor choices, enhances compliance, and improves operational agility. Modern banking relies on interconnected microservices, embedded governance, and real-time payment systems like FedNow to optimize cash flow and security.

Most business professionals treat banking like a utility: you plug in, money moves, and you don’t think about what’s behind the wall. That mental model costs you. Explaining modern banking infrastructure isn’t about satisfying curiosity. It’s about making smarter vendor choices, reducing compliance exposure, and knowing why your cross-border payment settled in two hours instead of two days. The reality is that core banking isn’t a single application but a layered ecosystem of interconnected services, each one a potential point of failure or competitive advantage depending on how well you understand it.

Table of Contents

- Key takeaways

- The core components of modern banking infrastructure

- Payment infrastructure and real-time processing

- Cybersecurity and operational risks in banking networks

- Data infrastructure and governance in banking operations

- Practical implications for businesses and entrepreneurs

- My take on what most businesses get wrong

- How Demivolt puts these principles into practice

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Banking is modular, not monolithic | Modern banking infrastructure consists of specialized, interconnected components, not one central system. |

| Real-time payments change cash flow | Instant payment rails like FedNow enable 24/7 settlements that directly improve working capital cycles. |

| API visibility gaps create real risk | Most financial IT teams overestimate their API oversight, leaving sensitive data exposed without knowing it. |

| Data governance powers compliance | Embedding governance into banking workflows protects against regulatory risk and enables AI-driven decisions. |

| Infrastructure knowledge drives vendor decisions | Understanding how banking systems are built helps you choose fintech partners that won’t create operational bottlenecks. |

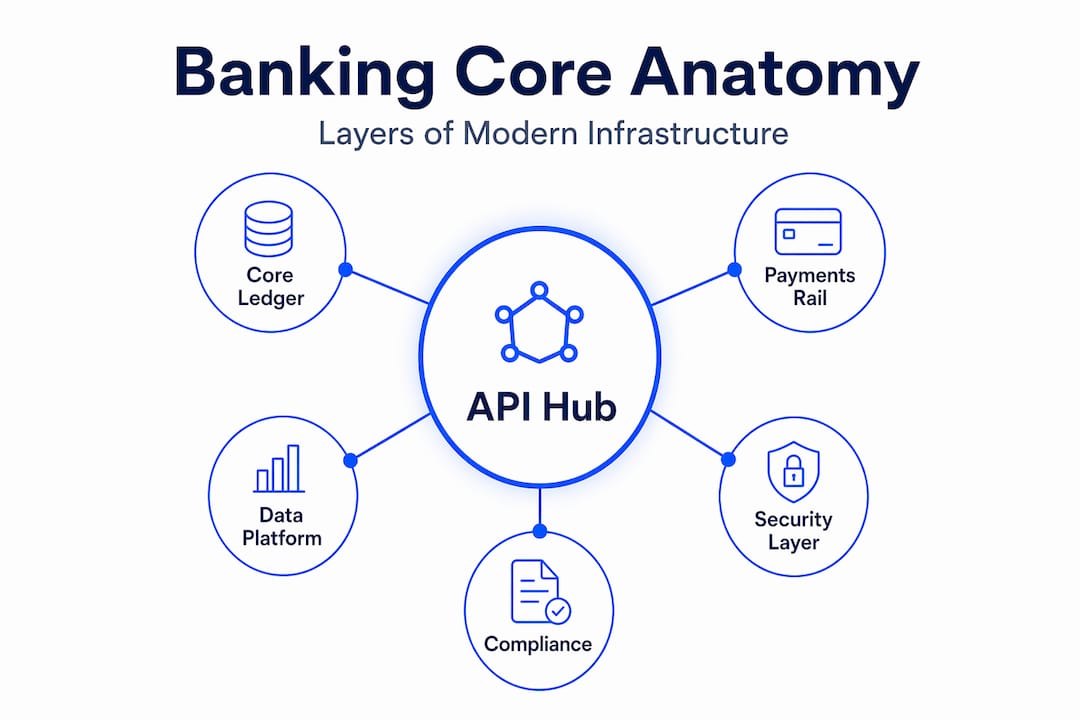

The core components of modern banking infrastructure

Think of modern banking infrastructure the way you’d think about a city’s transit network. There’s no single machine making everything work. There are roads, rail lines, traffic signals, dispatch systems, and maintenance crews, all running in parallel, all dependent on each other. Banking works the same way.

Modern banking systems use modular, API-first architectures that function like a central operating system for the institution, coordinating transactions, customer identity, product definitions, compliance checks, and channel delivery simultaneously. When you initiate a wire transfer, at least half a dozen discrete systems touch that transaction before it settles.

What a core banking system actually manages

The core banking layer handles four primary functions:

- Transaction processing: The engine that posts debits and credits in real time, maintains ledger accuracy, and reconciles balances across accounts and entities.

- Account and product management: The module that defines what products exist, what rules govern them, and how they behave across customer segments.

- Customer data management: The layer that stores identity records, KYC status, relationship history, and behavioral data, often integrated with external verification providers.

- Integration layer: The API gateway that connects core functions to external channels, third-party services, payment rails, and regulatory reporting systems.

What makes modern architecture different from systems built in the 1980s is the philosophy behind connectivity. Legacy systems were built as single, tightly coupled applications. Modern designs use microservices, where each function operates independently and communicates through APIs. This means a payment processing upgrade doesn’t require touching the customer data module. It also means failures stay contained rather than cascading.

Cloud-native infrastructure reinforces this. Modular architectures embed governance and compliance into workflows rather than treating them as separate checkboxes added at the end of development. For you as a business operator, this means that a well-architected banking partner can adapt to regulatory changes faster and with less disruption to your operations.

Pro Tip: When evaluating a fintech or banking partner, ask directly whether their platform is built on microservices or a monolithic core. The answer tells you a great deal about how quickly they can respond to regulatory changes and how stable their service will be under load.

Payment infrastructure and real-time processing

Payment infrastructure is the circulatory system of modern financial infrastructure. Without reliable money movement, every other banking service loses practical value. And the infrastructure behind payments has shifted more dramatically in the past five years than in the previous three decades.

The historic model was batch processing: payments collected throughout the day, settled in windows, cleared overnight. The shift to real-time rails has fundamentally changed how businesses manage cash flow. The Federal Reserve’s FedNow system, launched in 2023, supports 24/7/365 settlement with built-in fraud management and low error rates. The Fed itself processes over $5 trillion daily across roughly 9,000 connected institutions.

For a business operator, this matters in concrete ways:

- Same-day payroll becomes achievable without premium wire fees or manual intervention.

- Vendor payments settle the moment they’re sent, removing the guesswork from supplier relationship management.

- Cash visibility becomes accurate in real time instead of reflecting a position that’s 24 hours stale.

- Cross-border transactions can be routed through faster networks rather than defaulting to correspondent banking chains that add days and fees.

Stablecoins are emerging as a parallel layer on top of traditional rails. With the stablecoin market exceeding $300 billion as of mid-2026, treasury teams at forward-looking companies are using them for vendor payments and liquidity management, particularly where traditional SWIFT transfers carry excessive latency. Platforms tracking this trend, like Demivolt’s stablecoin infrastructure coverage, illustrate how this layer is quietly becoming standard for global operations rather than experimental.

Cybersecurity and operational risks in banking networks

Understanding how banking networks work is only half the picture. The other half is understanding where they break, and why the risks are growing.

Banking institutions accounted for 44% of Layer 7 DDoS attacks in APAC in 2025. Layer 7 attacks are particularly destructive because they target the application layer, the same layer where APIs communicate, rather than trying to overwhelm network bandwidth. This means they can disrupt specific services, like payment processing or customer authentication, while leaving other parts of a system running normally and looking healthy on surface-level monitoring.

The API visibility problem compounds this. 77% of IT leaders believe they have full API visibility, but only 27% can actually identify which APIs expose sensitive customer information. That gap represents a massive blind spot. Your banking partner may have hundreds of API connections to third-party processors, identity services, fraud tools, and reporting platforms. If their security team doesn’t know exactly what each connection touches, neither does their incident response plan.

The coexistence of legacy and modern systems creates additional friction. Most established banks still run core functions on mainframe systems built in the 1970s and 1980s, with modern APIs bolted on top. Keeping legacy systems while adding modern APIs through a hybrid model helps banks migrate without operational disruption, but it also creates seams where security controls don’t align. Microsegmentation addresses this directly. Financial institutions that implemented microsegmentation saw 33% faster incident response times in recent studies.

Pro Tip: Ask any banking or fintech partner for a summary of their API inventory management practice and how often they audit third-party connections. Institutions that can answer this clearly are operating with mature security programs. Those that cannot are carrying risks they haven’t quantified. You can also review AML compliance standards as a baseline for what rigorous financial risk management looks like.

Best practices for the businesses relying on these systems include:

- Requiring your banking providers to maintain behavioral analytics for anomaly detection across API traffic.

- Asking about their incident containment time and whether they use microsegmentation to isolate compromised components.

- Reviewing their cross-border payment security protocols if your operations span multiple jurisdictions.

Data infrastructure and governance in banking operations

Banking technology explained without covering data governance is like explaining a car without mentioning the fuel system. Data is what makes every other component actually function.

Modern banking data infrastructure is built around five connected layers:

| Layer | Primary function |

|---|---|

| Master Data Management (MDM) | Creates authoritative records across customer, product, and transaction domains |

| Governance framework | Defines ownership, quality standards, and access controls for every data asset |

| Cloud analytics platform | Processes structured and unstructured data for reporting, risk, and AI applications |

| Security and privacy controls | Enforces data residency, encryption, and access logging in line with regulatory requirements |

| AI and decision layer | Applies machine learning to governed data for credit, fraud, and operational decisions |

MDM creates authoritative records across critical data domains, which sounds abstract until you experience a compliance audit where two systems disagree on a customer’s KYC status. Governance embedded in workflows means that every data record entering the system is tagged, classified, and routed according to policy from the moment it arrives, not cleaned up manually before a regulatory review.

Modern financial data platforms embed compliance and governance within workflows using modular architectures, which supports AI-driven credit decisions, fraud detection, and treasury forecasting without the risks that come from feeding unverified data into machine learning models. For entrepreneurs evaluating whether a banking partner’s infrastructure is AI-ready, the question to ask is simple: where does your data governance live? If the answer is “we have a compliance team that reviews things,” that’s not governance by design. That’s governance by reaction.

Pro Tip: When selecting a business banking or treasury management platform, ask specifically whether their data architecture uses modular or monolithic design. Modular platforms allow you to add capabilities, such as analytics or AI tools, without rebuilding foundational systems. This matters when your business scales.

Practical implications for businesses and entrepreneurs

The components of banking infrastructure are not just technical details for IT departments. They have direct operational consequences for how you run your business.

Understanding how banking systems work at the architecture level changes how you evaluate financial partners. An institution running a modern API-first core can integrate with your accounting software, ERP, or treasury platform in days rather than months. One running a legacy mainframe with a modern facade may promise integration but deliver months of custom development and fragile point-to-point connections.

There are four areas where this knowledge pays off immediately:

- Vendor selection: Ask potential banking partners whether they support open banking APIs, what their uptime SLA looks like on payment processing specifically, and how they handle incidents affecting API-connected services.

- Compliance positioning: Banks with governance-by-design architectures will share cleaner audit trails, faster documentation on demand, and more consistent KYC data, all of which reduce your compliance burden during due diligence or regulatory reviews.

- Payment strategy: If your business processes vendor payments internationally, understanding whether your bank routes through SWIFT, SEPA, or real-time local rails lets you optimize for cost and speed rather than defaulting to whatever the bank recommends.

- Fintech integration: The fintech ecosystem reshaping business banking moves fast. Knowing which banking infrastructure standards your providers use helps you spot integration risks before they become operational problems.

The businesses that get this right don’t just avoid problems. They operate faster, with better cash visibility, cleaner compliance records, and more leverage in conversations with banking partners.

My take on what most businesses get wrong

I’ve spent years watching companies make avoidable banking infrastructure decisions. The pattern is consistent: a business grows into international operations, then discovers that its banking setup, built for domestic simplicity, creates compounding friction at every edge of the business.

The assumption I see most often is that a bank’s digital interface reflects its underlying infrastructure quality. It doesn’t. A bank can have a polished mobile app built on top of a 40-year-old core system. Conversely, some less visually impressive platforms run on genuinely modern, resilient infrastructure. You have to look past the interface and ask harder questions about what’s underneath.

What I find genuinely underappreciated is how much the data governance layer matters to day-to-day operations. Most entrepreneurs focus on payment speed and fees. Few ask about data architecture until they’re stuck in an audit trying to reconcile records across three systems that don’t agree. Getting that right from the start is not a technical luxury. It’s operational hygiene.

My honest view is that banking trends around efficiency and compliance are converging in a way that rewards businesses who’ve taken the time to understand infrastructure. The ones who haven’t are going to face increasingly painful vendor migrations, compliance gaps, and integration failures as their needs outgrow their banking setup.

— dd

How Demivolt puts these principles into practice

If the infrastructure picture above sounds complex, the practical answer for most businesses is choosing a platform where that complexity is already resolved.

Demivolt is built on the architecture concepts described in this article: API-first design, segregated IBAN accounts, real-time SEPA and SWIFT payment processing, and compliance embedded into onboarding rather than added as an afterthought. For businesses managing cross-border payments, multi-entity structures, or high-frequency transactions, the platform delivers business banking infrastructure designed to match how modern operations actually work. Role-based user management, virtual and physical card issuance, and full transaction visibility come standard. If you’re evaluating whether your current banking setup can support where your business is going, Demivolt is built for that specific question.

FAQ

What makes modern banking infrastructure different from older systems?

Modern banking infrastructure uses modular, microservices-based architectures where each function operates independently and communicates through APIs, unlike legacy systems built as single, tightly coupled applications. This design allows faster updates, better fault isolation, and easier integration with third-party tools.

How does real-time payment infrastructure affect business operations?

Real-time payment rails like FedNow enable 24/7 settlement, same-day payroll, and instant vendor payments, giving businesses accurate cash visibility instead of a position that’s always 24 hours behind. The Federal Reserve processes over $5 trillion daily across approximately 9,000 institutions using this infrastructure.

What is the biggest cybersecurity risk in modern banking infrastructure?

The API visibility gap is one of the most significant risks: 77% of IT leaders believe they have full API visibility, but only 27% can identify which APIs expose sensitive data. This blind spot creates exploitable attack surfaces, particularly for Layer 7 DDoS attacks targeting banking application layers.

Why does data governance matter for businesses using banking services?

Data governance determines whether your banking partner can produce clean, consistent records for compliance audits, KYC reviews, and regulatory reporting. Platforms that embed governance into workflows from the start reduce the risk of data conflicts that create compliance liability for the businesses relying on them.

How can entrepreneurs use infrastructure knowledge to choose better banking partners?

Ask potential partners whether they use microservices or monolithic core architecture, what their API inventory management practice looks like, and how they handle incidents affecting connected services. These questions reveal operational maturity that a product brochure never will.