TL;DR:

- Payment onboarding involves verifying business identity, legal status, and banking details to enable smooth payment processing.

- Poor preparation and manual workflows can cause delays, silent payout blocks, and increased rejection risks for businesses.

Payment onboarding is the formal process a business goes through to get set up with a payment provider so it can accept, process, and receive funds. Most business owners treat it like paperwork. That mindset causes costly delays. Done poorly, payment onboarding can freeze your revenue, trigger account holds, or silently block payouts while you continue taking orders. Understanding what the payment onboarding process actually involves, where it breaks down, and how to get it right, gives you a real operational advantage.

Table of Contents

- Key takeaways

- What payment onboarding actually involves

- Common pitfalls in the onboarding process

- How automation improves onboarding outcomes

- Best practices for managing your onboarding

- The real-world impact on your business

- My take on why onboarding deserves serious attention

- How Demivolt simplifies payment onboarding for SMEs

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Onboarding is more than compliance | Payment onboarding shapes your risk profile, pricing, and payout terms for the life of your account. |

| Payout verification is critical | Mismatched bank details are among the most common causes of delayed or failed first payouts. |

| Automation drastically cuts time | Automated systems can reduce onboarding time from over 30 minutes to under 5 minutes. |

| Silent failures are a real risk | You can be approved to transact while payouts are withheld due to unresolved verification flags. |

| Preparation prevents most problems | Consistent, accurate documentation across identity, business, and bank details removes the majority of rejection triggers. |

What payment onboarding actually involves

Payment onboarding is the structured process payment providers use to verify who you are, confirm your business is legitimate, and set up the infrastructure to move money in and out of your account. It is not a single form. It is a multi-layer vetting process with real consequences for how your account is configured.

At the core of every payment onboarding process are four verification categories:

- Identity verification. The provider confirms the identity of business owners and key controllers, typically using government-issued ID and cross-referencing public databases.

- Business verification. Know Your Business (KYB) checks confirm that your company legally exists, is registered in the correct jurisdiction, and matches the information you have provided. Risk teams analyze 100+ data points including business history, financial documents, and ownership structure during this phase.

- AML screening. Anti-Money Laundering checks flag any connections to sanctioned individuals, suspicious transaction patterns, or high-risk industries before approval is granted.

- Payout account verification. Your bank account is verified to confirm it belongs to the same entity being onboarded. Payout setup is one of the most failure-prone stages of the entire process due to name mismatches and delayed verification.

Beyond these checks, the provider assigns your business a Merchant Category Code (MCC). This four-digit code classifies your industry and directly affects your chargeback thresholds, transaction fees, and how card issuers evaluate your business. Getting the wrong MCC, or having it assigned based on incomplete information, can create problems that follow your account indefinitely.

To understand how identity verification processes connect to broader compliance requirements, it helps to view onboarding as a negotiation, not just an application.

Common pitfalls in the onboarding process

Knowing what happens during onboarding is one thing. Knowing where it goes wrong is where most business owners gain real ground. Here are the most common failure points, in the order they typically hit:

- Document overload and inconsistency. Providers request a significant volume of documents. When information on your incorporation certificate, bank account, and identity documents does not match exactly, verification fails. Even minor name discrepancies (“Ltd” vs “Limited”) can trigger a rejection or a manual review that adds days to your timeline.

- Manual data entry errors. When bank account details are entered manually, typos cause payout routing failures. Name mismatches and delayed verification on payout accounts are a leading cause of early payout failures and escalating support tickets.

- Slow verification timelines. Identity checks, business registry lookups, and AML screening do not always happen in real time. When manual review is triggered, activation can be delayed by days or weeks, directly impacting your revenue start date.

- Risk assessment mismatches. If your business description does not align cleanly with your stated industry or revenue model, the risk team flags the account for further review. Ambiguity in how you describe your business almost always works against you.

- Silent payout failures. This is the most dangerous scenario. Silent failures occur when a merchant is approved to accept payments but payouts are withheld because a verification step was not completed or a webhook notification was not handled. You can be processing transactions for weeks while the money accumulates in a hold. Most businesses do not discover this until they notice the absence of incoming funds.

Pro Tip: Request a written confirmation of your verification status and expected payout timeline at every stage of onboarding. Do not assume approval to transact means approval to receive payouts. These are two separate gates.

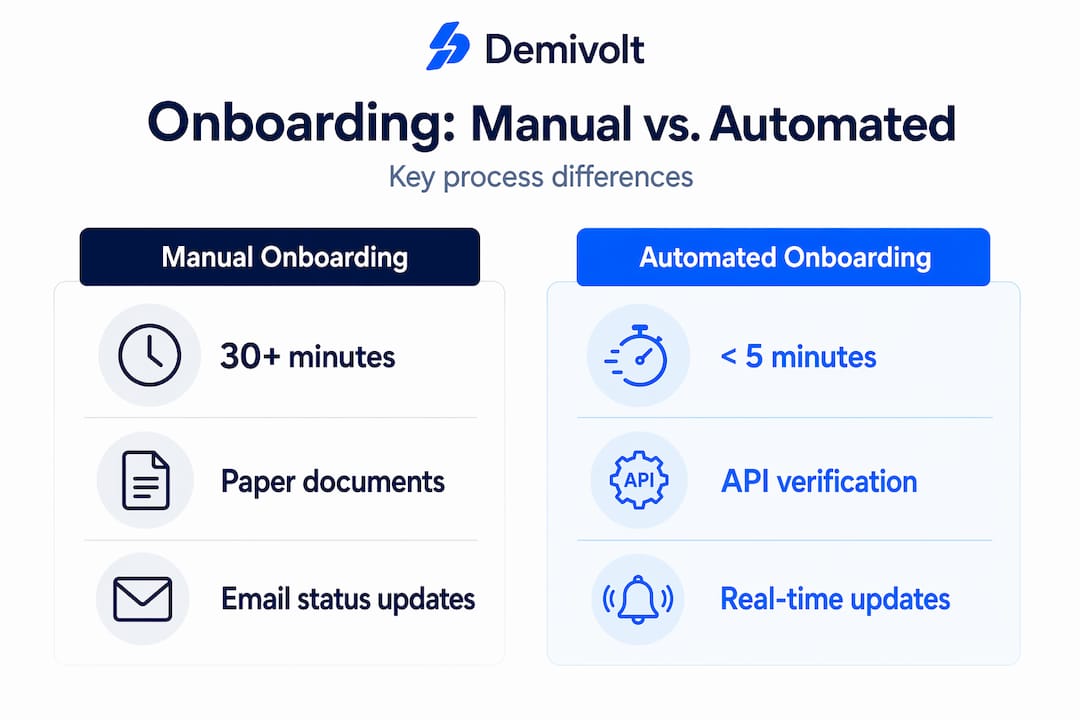

How automation improves onboarding outcomes

The difference between a smooth onboarding experience and a frustrating one often comes down to whether the provider is running a manual or automated workflow. The contrast is significant.

| Factor | Manual onboarding | Automated onboarding |

|---|---|---|

| Time to complete | 30 minutes or more | Under 5 minutes |

| Data entry errors | High risk from manual input | Reduced through direct API connections |

| Status visibility | Limited, reactive | Real-time dashboards and alerts |

| First payout success | Lower, more variables | Higher, verified account linking |

| Escalation handling | Manual review queues | Automated flagging with direct routing |

Automated onboarding platforms use API-based identity verification tools to match documents against live databases in seconds. Bank account linking through APIs removes the manual entry step entirely, which eliminates the most common source of payout failures. Rather than submitting your bank details as typed text, the system verifies ownership electronically before any funds are ever sent.

Two-way communication and real-time status updates are another measurable benefit of automated systems. Instead of waiting on email responses about verification progress, you get dashboard visibility into exactly which step is pending and what action is needed from you. This alone reduces the back-and-forth that causes most activation delays.

Effective onboarding platforms combine electronic identity verification and bank account linking through APIs and reserve manual review only for genuinely high-risk cases. This speeds activation for compliant businesses without lowering the bar on due diligence.

Pro Tip: When evaluating payment providers, ask specifically whether their verification is API-driven or manual. A provider using direct processor connections will get you to first payout faster and with fewer errors.

Best practices for managing your onboarding

Preparing properly before you start onboarding is the single most effective thing you can do to avoid delays. Here is what that looks like in practice:

- Standardize your business information. Your legal name, registered address, and company number must appear identically on every document you submit. Cross-check your bank account name against your official business registration before you start.

- Prepare your document package in advance. Typical requirements include a certificate of incorporation, proof of address for the business, government-issued ID for all beneficial owners (usually anyone holding more than 25%), and recent bank statements. Having these ready in digital format prevents the most common bottleneck.

- Verify your payout account before submission. Verification requires consistent matching across identity, business existence, ownership, and payout account details. Any mismatch across these four categories is a rejection trigger. Check that your bank account is registered under the exact same legal entity name you are onboarding.

- Communicate proactively with your provider. Do not wait for rejection notices. Contact your provider during the process to confirm which checks are pending and what the expected timeline looks like. Building a direct relationship with an account manager shortens resolution times dramatically.

- Plan for ongoing compliance. Onboarding is not a one-time event. Payment providers conduct periodic re-verification, especially when your transaction volumes change or you expand into new markets. Many onboarding failures result from neglected post-onboarding monitoring and unresolved verification flags. Build a compliance review into your annual financial calendar.

For a deeper look at building secure payment workflows after onboarding, the Demivolt guide on payment workflow security covers risk team considerations and document requirements in practical detail.

The real-world impact on your business

Payment onboarding is not just a legal hurdle. The decisions made during onboarding shape your operational reality well beyond the setup phase. Onboarding decisions drive your merchant profile, risk levels, pricing, and payout schedules within the acquiring ecosystem. That risk profile follows you and is difficult to change once set.

Your MCC assignment affects chargeback ratios, fraud controls, and how card networks categorize your transactions. A misclassification can raise your processing fees or trigger unnecessary fraud flags on legitimate transactions. Correcting it requires re-review and creates downtime.

Customer trust is also at stake. When a customer places an order and receives a failed transaction message, or when your business cannot fulfill orders because payouts are frozen, that experience damages your reputation. These outcomes trace directly back to onboarding gaps.

The first successful payout is a trust milestone. It confirms that your business is fully operational within the payment ecosystem. Until that moment, you are technically onboarded but not yet financially active.

The reputational and financial cost of poor onboarding scales with business size. For an SME, a two-week payout delay during peak trading can be genuinely damaging. For a growing operation handling cross-border payments, the stakes are higher still. Viewing onboarding as a strategic foundation, not a formality, changes how you prepare for it.

My take on why onboarding deserves serious attention

I’ve worked with enough SMEs navigating payment setup to see a consistent pattern: businesses invest heavily in their product, their marketing, and their operations, then treat payment onboarding as a box to check on the way to launch.

The result is predictable. Founders submit documents in a rush, overlook the bank account name mismatch, and spend their first week live wondering why payouts are not arriving. In my experience, the businesses that sail through onboarding are not necessarily more sophisticated. They are simply more prepared. They read the requirements in full, gather documents before starting, and ask questions upfront.

What I’ve learned from observing automated versus manual onboarding workflows is that technology closes most of the gap caused by human error. But technology only helps businesses that show up with accurate, consistent information. Garbage in still means garbage out.

My strong recommendation: treat your first onboarding as a rehearsal for every payment relationship you will have afterward. The habits you build around documentation, verification, and compliance communication will serve you every time you add a new payment method or expand into a new market.

— dd

How Demivolt simplifies payment onboarding for SMEs

For business owners who want a payment and banking setup that does not become a months-long compliance project, Demivolt offers a regulated European business banking platform built specifically for modern SMEs.

Demivolt’s onboarding is designed to be fast, transparent, and compliant with EU regulatory standards. The platform provides dedicated IBAN accounts, SEPA and SWIFT payment support, and automated verification workflows that reduce the manual friction that causes most onboarding delays. For businesses managing cross-border operations or multiple payment streams, Demivolt supports multi-account structures and role-based user access, meaning your team has the right level of control without unnecessary complexity. If you are looking to get your payment infrastructure right from the start, it is worth exploring what Demivolt’s fintech onboarding approach looks like in practice.

FAQ

What is payment onboarding?

Payment onboarding is the process a business completes with a payment provider to get verified, set up for payment processing, and activated to receive payouts. It includes identity checks, KYB screening, AML review, and bank account verification.

How long does the payment onboarding process take?

Timelines vary by provider and complexity. Automated onboarding can be completed in under 5 minutes, while manual processes can take several days or longer if additional documentation or risk review is required.

Why would payouts be blocked after onboarding is complete?

Silent failures occur when a merchant is approved to accept transactions but payout verification was never fully completed. Funds are held until the verification flag is resolved, which can go unnoticed without proactive status tracking.

What documents are typically required for payment onboarding?

Most providers require a certificate of incorporation, proof of business address, government-issued ID for beneficial owners, and bank account verification documents. Requirements vary by jurisdiction and business type.

How does my merchant category code affect my payment account?

Your MCC classifies your business type and directly influences your processing fees, chargeback thresholds, and how card networks assess your transactions. A misclassified MCC can raise costs and trigger unnecessary fraud controls.

Recommended

- Demivolt | Blog – Digital banking client onboarding: a compliance-first guide

- Demivolt | Blog – Onboarding in fintech: Efficient, compliant solutions for SMEs

- Demivolt | Blog – How to automate business payments and stay compliant

- Demivolt | Blog – Why automate business payments? Reduce costs, risks and delays