TL;DR:

- Financial compliance involves adhering to laws and standards that govern financial operations, critical for SME protection and trust. Poor compliance management leads to severe penalties, personal liability, and damage to business relationships. Establishing documented controls, ownership, automation, and regular audits ensures ongoing compliance and reduces risks across jurisdictions.

Financial compliance is the process by which businesses meet all legal, regulatory, and standards requirements governing financial operations and reporting. For SME owners and financial managers, getting this wrong is expensive. Civil penalties exceed $1 million per violation for OFAC-related offenses, and regulators increasingly target individuals, not just companies. Financial compliance explained clearly means understanding which rules apply to your business, building repeatable processes to follow them, and generating the evidence that proves you did. This article covers the key components, practical implementation steps, jurisdictional differences, and the risks that catch SMEs off guard.

What is financial compliance and why does it matter for SMEs?

Financial compliance, known formally as regulatory compliance in financial services, is the discipline of adhering to laws, regulations, and internal standards that govern how a business handles money. The densest regulatory environment in any sector is financial services, which requires integrated Anti-Money Laundering (AML), sanctions, Know Your Customer (KYC), and capital adequacy management. SMEs often assume these obligations apply only to banks. They do not.

Any business that sends or receives payments, holds customer funds, or operates across borders carries compliance obligations. The consequences of ignoring them range from tax penalties and license revocation to criminal prosecution. Understanding financial compliance is the first step toward protecting your business and your personal liability as a director or officer.

The importance of financial compliance goes beyond avoiding fines. Regulators, banks, and enterprise clients increasingly require documented compliance programs before they will work with a business. A weak compliance posture can cost you banking relationships, contracts, and investor confidence.

What are the key components of financial compliance?

Anti-Money Laundering and Know Your Customer controls

AML controls require businesses to identify and verify the people they do business with, monitor transactions for suspicious activity, and report concerns to the relevant authority. KYC is the front-end process: collecting identity documents, verifying beneficial ownership, and screening against sanctions lists. These are not optional for SMEs that handle significant payment volumes or serve international clients.

Sanctions compliance and OFAC obligations

The U.S. Office of Foreign Assets Control (OFAC) administers sanctions programs that prohibit transactions with designated individuals, entities, and countries. Violations are strict liability offenses, meaning intent does not matter. Your business is responsible for screening every counterparty, even if you did not know they were sanctioned. Explore how AI in sanctions compliance is changing how finance teams handle this screening at scale.

Tax registration and reporting requirements

Tax compliance covers registration, collection, filing, and payment. These are four distinct obligations, and failing any one of them carries separate penalties. Key financial compliance requirements for SMEs include:

- VAT registration in the EU once turnover thresholds are crossed in relevant member states

- GST registration in Singapore at S$1 million in annual taxable turnover

- VAT registration in the UAE at AED 375,000 in annual revenue

- SST registration in Malaysia at RM 500,000 in annual sales

- Economic nexus registration in U.S. states, typically triggered at $100,000 in sales or 200 transactions annually

Pro Tip: Build a registration threshold tracker in a shared spreadsheet. List every jurisdiction where you sell, the applicable threshold, your current revenue in that market, and the date you expect to cross it. Review it monthly.

| Jurisdiction | Tax Type | Registration Threshold |

|---|---|---|

| Singapore | GST | S$1,000,000 annual turnover |

| UAE | VAT | AED 375,000 annual revenue |

| Malaysia | SST | RM 500,000 annual sales |

| U.S. states | Sales tax | ~$100,000 or 200 transactions |

| EU member states | VAT | Varies by country |

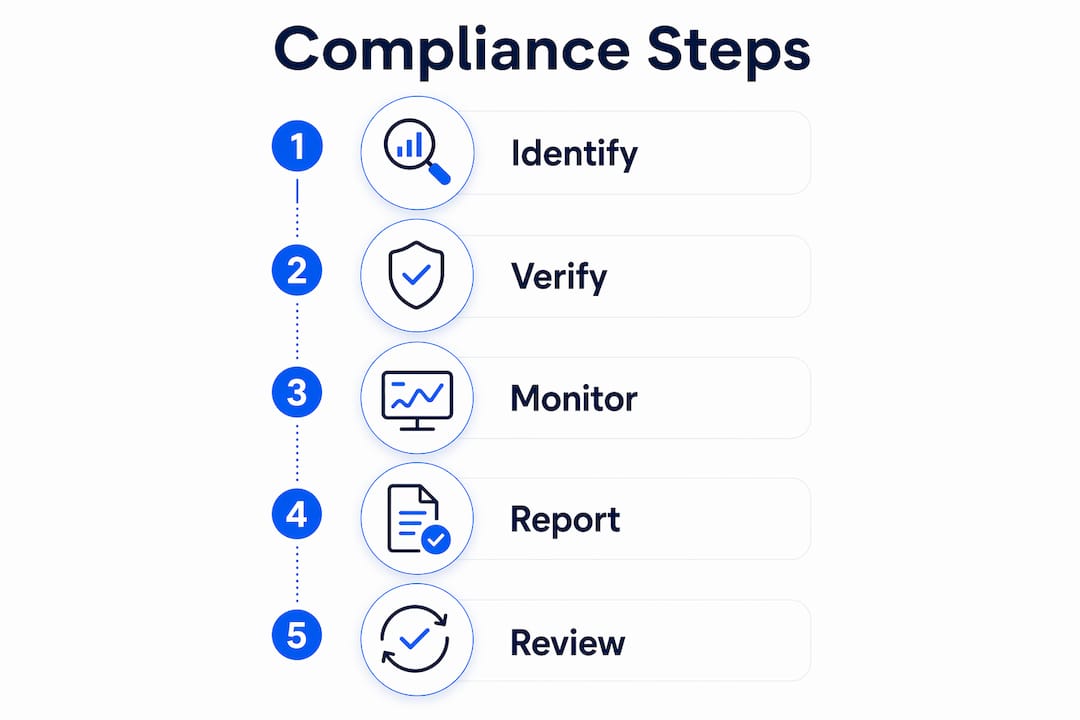

How do SMEs implement effective financial compliance processes?

The most common mistake SMEs make is treating compliance as a checklist to complete once. Compliance is not about knowing the rules. It is about running the rules as a repeatable process through policies, workflows, and evidence capture. That distinction separates businesses that pass audits from those that scramble when regulators call.

Here is a practical sequence for building a compliance program that holds up:

-

Build a compliance map. Document every obligation your business carries, the control that addresses it, and the evidence that proves the control ran. This three-layer structure, obligations, controls, and evidence, is the foundation of audit-ready documentation and reduces the stress of any regulatory review.

-

Assign clear ownership. Separate compliance ownership across finance, IT, and HR. Each function carries distinct obligations. When one person owns everything, gaps appear. When ownership is shared and documented, accountability is clear.

-

Automate evidence capture. Manual approvals feel thorough but create gaps. Automated, repeatable checks embedded into daily workflows reduce dependency on retrospective sign-offs and improve reliability. Tools like transaction monitoring software, automated KYC platforms, and payment compliance systems generate proof without adding manual steps.

-

Run quarterly internal audits. Quarterly internal financial audits combined with an annual mock audit keep your program calibrated. Quarterly reviews catch drift before it becomes a violation. The annual mock audit simulates a regulator’s review so your team knows exactly what to produce and where.

-

Separate personal and business finances from day one. Mixing personal and business finances destroys the credibility of your financial records and makes it nearly impossible to demonstrate good faith in an enforcement inquiry. Open a dedicated business account before you process your first transaction.

-

Integrate tax calculation into your payment workflow. Automated tax calculations at the point of sale prevent hidden liabilities from accumulating. Discovering you owe two years of uncollected VAT after the fact is far more damaging than configuring tax rules correctly from the start.

Pro Tip: Treat your compliance map as a living document. Schedule a 30-minute review every quarter to update obligations when regulations change, controls when your processes evolve, and evidence when your tools change.

Learning how to automate business payments is one of the fastest ways to reduce manual compliance risk in your payment operations.

What are the risks and penalties of financial non-compliance?

The financial penalties for compliance failures are severe and often underestimated by SME leaders. OFAC-related violations carry civil penalties exceeding $1 million per violation. AML failures attract similar enforcement action from financial intelligence units across jurisdictions. These are not theoretical risks reserved for large institutions.

The most common pitfalls that expose SMEs include:

- Mixing personal and business accounts, which undermines every financial record you produce

- Missing registration thresholds in new markets because no one is tracking them

- Filing tax returns late while assuming that is better than not filing, when late payment penalties often equal or exceed late filing penalties

- Relying on manual approvals as the primary compliance control, which creates gaps and no audit trail

- Failing to screen counterparties against sanctions lists before processing payments

“More approvals do not equal more compliance. Segregation of duties and automated evidence capture reduce human error in sensitive operations far more effectively than adding manual sign-off layers.” — Financial Compliance Management Step-by-Step Guide

Personal liability is a real and growing risk. Regulators in the U.S., UK, and EU have shifted enforcement focus toward individual officers and directors, not just corporate entities. If you sign off on financial operations without adequate controls in place, you carry personal exposure. The mitigation is straightforward: document your controls, run them consistently, and keep the evidence.

Review a detailed business payments compliance checklist to identify gaps in your current payment controls before they become enforcement issues.

How does financial compliance vary across jurisdictions?

Jurisdictional variance is where SMEs operating internationally get caught most often. The financial compliance guidelines that apply in your home market do not automatically apply abroad, and the reverse is equally true. A SaaS company selling to customers in Singapore, the UAE, and Malaysia faces three separate registration regimes, each with different thresholds, timelines, and filing formats.

The speed of obligation is the part most businesses miss. Some jurisdictions require registration within days of crossing a threshold, not at the end of the tax year. The registration thresholds vary significantly across markets, and some authorities expect you to register and begin collecting tax almost immediately after you cross the trigger point.

For e-commerce and SaaS SMEs, the online business financial compliance checklist must include a jurisdiction-by-jurisdiction review of:

- Where your customers are located

- What the applicable tax type is (VAT, GST, SST, or sales tax)

- The registration threshold in each market

- The filing frequency once registered

- Whether a local fiscal representative is required

Pro Tip: Subscribe to the official tax authority newsletter or RSS feed for every jurisdiction where you operate. Rates and thresholds change, and the official source is always faster than third-party compliance services.

The EU presents a specific complexity for European SMEs. VAT rules differ by member state, and the One Stop Shop (OSS) scheme simplifies cross-border filing but does not eliminate the need to understand where your obligations sit. Explore the EU banking regulations guide for a structured overview of how European compliance frameworks apply to SMEs in financial services.

For U.S.-based SMEs selling digitally, economic nexus thresholds in individual states create obligations that trigger immediately once crossed, regardless of whether you were aware of the rule. The standard threshold of $100,000 in annual sales or 200 transactions applies in most states, but the details vary enough that a state-by-state review is necessary.

Key Takeaways

Financial compliance is an ongoing operational discipline that requires documented controls, clear ownership, and consistent evidence generation to protect SMEs from penalties, personal liability, and regulatory action.

| Point | Details |

|---|---|

| Define your obligations first | Map every regulatory requirement that applies to your business before building any controls. |

| Automate evidence capture | Repeatable automated checks generate audit-ready proof without adding manual approval layers. |

| Track registration thresholds | Monitor revenue in each jurisdiction monthly to avoid missing tax registration deadlines. |

| Run quarterly audits | Internal audits every quarter, plus one annual mock audit, keep your compliance program calibrated. |

| Separate finances from day one | Dedicated business accounts are the foundation of credible financial records and regulatory good faith. |

Why compliance programs fail before they start

Most SME compliance programs I have reviewed share one structural flaw: they were built to satisfy a single audit or investor request, not to run continuously. The team completes the checklist, files it away, and moves on. Six months later, the thresholds have changed, the controls have drifted, and the evidence trail has gone cold.

The misconception that compliance is a static tick-box leads directly to fragile programs. Real compliance is a rhythm, not an event. It requires someone who owns it, a calendar that enforces it, and tools that generate evidence automatically.

The other failure I see consistently is the belief that adding more approvals makes a process more compliant. It does not. It makes the process slower and creates the illusion of control without the substance. What actually works is segregation of duties combined with automated evidence capture. When the system generates proof that a control ran, you do not need three people to sign off on it.

Start with the compliance map. Get the obligations documented, assign a control to each one, and define what evidence proves the control ran. That structure alone puts you ahead of most SMEs. Then automate wherever you can, review quarterly, and treat the map as a living document rather than a finished product.

— dd

How Demivolt supports SME financial compliance

Managing financial compliance across multiple jurisdictions is significantly easier when your banking infrastructure is built for it. Demivolt provides SMEs with dedicated IBAN accounts, SEPA and SWIFT payment management, and role-based user controls that support segregation of duties directly within your banking setup. Every transaction is traceable, every account is segregated, and the infrastructure meets EU regulatory standards by design.

Start with Demivolt’s free IBAN validator tool to verify international payment details before processing, reducing the risk of misdirected funds and failed compliance checks. You can also access the full suite of free SEPA tools to support payment compliance workflows across European markets. For SMEs building or tightening their compliance programs, Demivolt’s infrastructure removes the friction from the banking layer so your team can focus on the controls that matter.

FAQ

What is financial compliance in simple terms?

Financial compliance is the practice of following all laws, regulations, and standards that govern how a business manages and reports its money. It covers tax obligations, AML controls, sanctions screening, and financial reporting requirements.

What are the biggest financial compliance risks for SMEs?

The most common risks include missing tax registration thresholds in new markets, failing to screen counterparties against sanctions lists, mixing personal and business finances, and relying on manual approvals instead of documented controls with audit trails.

How often should SMEs conduct compliance audits?

Quarterly internal audits combined with one annual mock audit represent the recommended standard. Quarterly reviews catch issues early; the annual mock audit prepares your team for a real regulatory review.

Does financial compliance apply to small online businesses?

Yes. E-commerce and SaaS businesses face tax registration obligations in every jurisdiction where they exceed revenue thresholds, which can be as low as $100,000 in annual sales in U.S. states or S$1 million in Singapore for GST purposes.

What is a compliance map and do SMEs need one?

A compliance map is a document that lists every regulatory obligation a business carries, the control that addresses it, and the evidence that proves the control ran. SMEs that build and maintain one are significantly better prepared for audits and regulatory inquiries.