TL;DR:

- Managing finances across disconnected tools damages SMEs by increasing manual work and errors.

- Integrated banking connects accounts directly via APIs, enabling real-time reconciliation, faster payments, and lower costs.

Managing finances across disconnected tools is one of the most quietly damaging habits an SME can have. If your team is manually exporting bank statements into spreadsheets, logging into three separate portals to move money, and reconciling transactions at month-end with crossed fingers, you already know the cost. The real question is why use integrated banking instead of patching the gaps with workarounds. This guide breaks down what integrated banking actually is, what it does for your operations, and how to make it work for your business without a painful overhaul.

Table of Contents

- Key takeaways

- Why use integrated banking: the core concept

- Key benefits of integrated banking for SMEs

- Integrated banking vs. traditional banking: a direct comparison

- How to implement integrated banking without disruption

- My take: why this decision is more urgent than most SMEs realize

- How Demivolt makes integrated banking work for your SME

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Integration eliminates manual work | Connecting banking to your finance tools removes duplicate data entry and reduces reconciliation errors. |

| Faster payments improve cash flow | API-based payments settle in under 10 seconds, compared to days with traditional card processing. |

| Lower costs than traditional banking | Fixed transaction fees and reduced chargeback exposure make integrated banking financially smart for SMEs. |

| Implementation does not require full replacement | Modern integration layers let you modernize progressively without replacing your existing systems entirely. |

| Reliability is a competitive advantage | Stable, well-governed banking infrastructure builds customer trust and protects operational continuity. |

Why use integrated banking: the core concept

Before getting into the benefits, it helps to understand what integrated banking actually means in practice. At its core, integrated banking connects your business bank accounts directly to the other systems you use to run your company, such as accounting software, ERP platforms, or payment processors. The connection happens through APIs, which are programming interfaces that let two software systems talk to each other in real time.

Traditional banking keeps everything in a silo. You log into your bank, download a statement, upload it somewhere else, and hope the formatting matches. Integrated banking removes that entire chain of manual steps.

Here is what that looks like for a real SME:

- Balance visibility without logging in: Your accounting software shows live account balances pulled directly from your bank, so your bookkeeper never has to switch tabs to check available funds.

- Transfers initiated inside your ERP: A supplier invoice gets approved in your finance tool and the payment is triggered immediately, no separate bank portal required.

- Automatic transaction sync: Every inbound and outbound payment hits your books the moment it clears, cutting reconciliation time from hours to minutes.

- Faster onboarding for new accounts: Embedded banking products like those pioneered by Yayoi and GMO Aozora Net Bank allow balance checks and transfers inside accounting tools, with transaction data syncing automatically.

The distinction from traditional disconnected banking is not just cosmetic. It changes how your finance team spends its time, how quickly you can close your books, and how much control you have over cash flow at any given moment.

Key benefits of integrated banking for SMEs

The advantages of integrated banking compound quickly once you see them in practice. This is not about adopting technology for its own sake. Every benefit here translates to real money, saved time, or reduced risk.

Fewer errors, less manual labor. Every time a human manually transfers data between systems, there is a chance of a typo, a skipped row, or a mismatched currency figure. Integrated systems eliminate manual logins and duplicate data transfers, removing entire categories of error from your back office. For SMEs running lean finance teams, that is not a small thing.

Dramatically faster payment settlements. This is where the numbers get compelling. API-based payments settle in under 10 seconds, compared to the one to three days typical of card gateway processing. For businesses managing B2B invoices or cross-border payments, that difference is the gap between a cash flow crisis and a smooth operation.

Lower transaction costs. Open banking payments governed by PSD2 regulation come with fixed fees of 20 to 50 cents, no fraud disputes from card issuers, and immediate liquidity benefits. Compare that to percentage-based card processing fees and the cost advantage is obvious.

Operational efficiency from consolidation. Fragmented systems are expensive to maintain. Connecting account opening, lending, and card functions into one unified ecosystem reduces the number of vendor relationships you manage and the complexity of daily financial operations.

Built-in security and reliability. As banking becomes embedded in broader business workflows, operational reliability becomes a strategic asset. A system that is down at the wrong moment costs far more than the subscription fee you pay to avoid it. Integrated platforms with proper governance and monitoring reduce that risk significantly.

Pro Tip: When evaluating integrated banking solutions, ask vendors specifically about uptime SLAs and incident response times. A provider offering 99.5% uptime sounds reassuring until you calculate that it allows 43 hours of downtime per year.

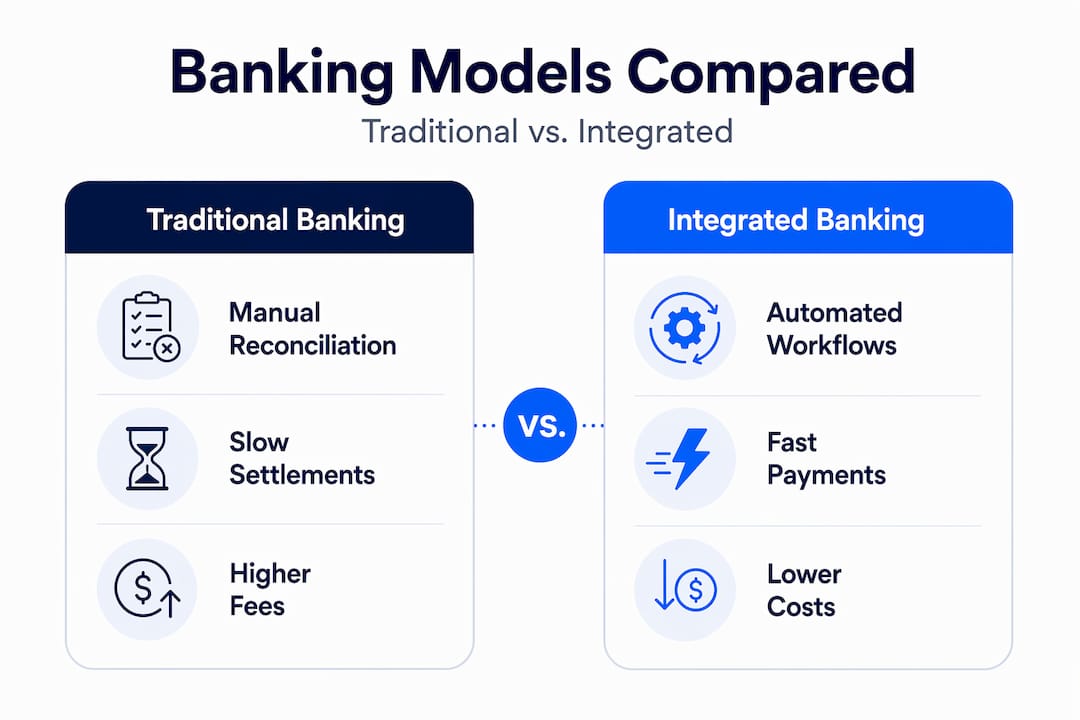

Integrated banking vs. traditional banking: a direct comparison

Most SMEs do not switch banking models because they fear disruption. That fear is understandable, but it is based on a misreading of how modern integration actually works. You do not have to replace everything to get the benefits.

Modern integration layers let you wrap existing banking infrastructure with API connectivity, launching new capabilities without disturbing the core systems underneath. That means you can adopt integrated banking progressively, one function at a time.

Here is how the two approaches stack up across the dimensions that matter most to SMEs:

| Feature | Traditional banking | Integrated banking |

|---|---|---|

| Transaction reconciliation | Manual, end-of-day or monthly | Automatic, real-time |

| Payment settlement speed | 1 to 3 business days | Under 10 seconds via API |

| Transaction fees | Percentage-based, variable | Fixed rate, 20 to 50 cents |

| System logins required | Multiple portals | Single connected workflow |

| Error risk | High (manual data transfers) | Low (automated sync) |

| Scalability | Limited by manual capacity | Scales with transaction volume |

| Compliance management | Fragmented across systems | Centralized policy enforcement |

The centralized auditing and policy enforcement that integrated platforms provide is particularly valuable for SMEs that are growing. When your transaction volume doubles, integrated banking scales with you. Traditional banking workflows collapse under that pressure.

The modernization argument here is practical, not ideological. You are not tearing out what works. You are connecting it so it works better.

How to implement integrated banking without disruption

Choosing to adopt integrated banking is the easy part. Doing it without creating chaos in your existing operations takes more thought. These steps will save you significant pain.

-

Audit your current financial stack. Before you select a platform, map every tool your finance team uses: accounting software, payment processors, expense management, payroll. You need to know what needs to connect before you can evaluate whether a given integration solution covers it.

-

Prioritize your highest-friction pain points. Not every integration delivers equal value. If manual reconciliation is eating 10 hours a week, start there. If delayed supplier payments are hurting vendor relationships, focus on payment speed first. Fix the biggest problem before adding complexity.

-

Verify API compatibility with your existing tools. Most modern accounting platforms support open banking APIs, but confirm this before committing. Integrated banking solutions that connect natively to your accounting software deliver far more value than those requiring middleware or custom builds.

-

Manage onboarding and compliance upfront. EU-regulated platforms, in particular, require identity verification and compliance checks during account setup. Governance across interoperable services is non-negotiable. Budget time for this step rather than treating it as a blocker.

-

Select a platform with room to grow. Your needs in year one are not your needs in year three. Look for platforms that support multi-account structures, role-based access, and cross-border payments. Changing banking platforms is expensive and disruptive, so choose for where you are going, not just where you are.

-

Run a parallel period before going live. For one to two weeks, run your new integrated system alongside your existing process. This catches sync errors, confirms data accuracy, and gives your team confidence before you depend on it entirely.

Pro Tip: Choose a provider that supports modern banking trends like role-based user permissions and multi-account structures from day one. These features feel optional until your team grows and suddenly they are not.

Fintech-driven banking for SMEs has lowered the barrier to entry considerably. Platforms that once required enterprise budgets are now accessible to businesses with five employees. The implementation question has shifted from “can we afford to do this?” to “can we afford not to?”

My take: why this decision is more urgent than most SMEs realize

I’ve worked alongside enough SME finance teams to know that the biggest barrier to adopting integrated banking is not cost or technical complexity. It’s the belief that the current system, however inefficient, is “good enough.”

What I’ve seen repeatedly is that “good enough” tends to break at the worst possible moment. A finance director is on leave. A large customer pays early and the cash doesn’t show in your accounting tool for three days. A payment to a critical supplier gets delayed because someone forgot to log into the bank portal. These are not edge cases. They are the predictable outcomes of disconnected systems operating under pressure.

What I’ve learned is that operational resilience is not a feature you add when you can afford it. It is the baseline from which everything else in your business operates. If your financial infrastructure is fragile, your whole operation is fragile.

The SMEs I’ve seen thrive financially share one common trait: they treat their banking infrastructure as seriously as they treat their sales pipeline. They want real-time visibility, minimal manual intervention, and systems that hold up under volume. Integrated banking is how you build that. Not as a one-time fix, but as a strategic choice that pays compounding dividends as your business scales.

My honest recommendation: stop treating banking as a back-office nuisance and start treating it as operational infrastructure. The upside is not theoretical. It is measurable, month by month.

— dd

How Demivolt makes integrated banking work for your SME

Demivolt is built specifically for businesses that need their banking to work inside their operations, not alongside them. The platform gives SMEs dedicated IBAN accounts, SEPA and SWIFT payment management, and virtual and physical business cards, all within a compliant, EU-regulated environment. Multi-account structures and role-based user permissions mean your team always has the right level of access, nothing more and nothing less.

If cross-border transactions are part of your business, Demivolt handles currency complexity without requiring you to manage multiple banking relationships. Onboarding is fast, transparent, and built to meet EU regulatory standards with segregated client funds for added protection.

For SMEs ready to move beyond disconnected banking, Demivolt’s business banking platform is a practical starting point. You can also explore how digital banking empowers SMEs in cross-border finance for a deeper look at what integrated financial infrastructure actually unlocks.

FAQ

What is integrated banking for SMEs?

Integrated banking connects your business bank accounts directly to your accounting, payment, and finance tools via APIs. It eliminates manual data transfers and gives your team real-time visibility into cash flow inside the tools they already use.

What are the main benefits of integrated banking?

The core benefits include automatic transaction reconciliation, payment settlement in under 10 seconds, lower fixed transaction fees, and reduced operational complexity from consolidating fragmented financial systems.

Is integrated banking safe for small businesses?

Yes, when implemented through regulated platforms. The importance of integrated banking done properly means choosing providers with strong governance, operational monitoring, and compliance frameworks, particularly those meeting EU regulatory standards.

Do I need to replace my existing banking to use integrated banking solutions?

No. Modern integration layers allow you to add API connectivity to existing infrastructure progressively, without replacing core systems. You modernize function by function, not all at once.

How do integrated banking services reduce transaction costs?

Open banking payments under PSD2 regulation carry fixed fees of 20 to 50 cents per transaction and eliminate chargeback disputes from card issuers, making them significantly cheaper than traditional percentage-based card processing for high-volume SMEs.

Recommended

- Demivolt | Blog – Modern business banking trends: boost efficiency & compliance

- Demivolt | Blog – Why digital banking empowers SMEs for smarter cross-border finance

- Demivolt | Blog – How Fintech Is Transforming Banking for SMEs: Efficiency

- Demivolt | Blog – How to streamline your digital business banking workflow