TL;DR:

- KYC is a continuous process that verifies customer identity, assesses risk, and prevents financial crimes. It involves onboarding, ongoing monitoring, and intensified review for high-risk clients, supported by risk-driven triggers. Banks with effective KYC programs improve compliance, reduce fraud, and build customer trust while avoiding costly penalties.

KYC, or Know Your Customer, is defined as the mandatory process banks use to verify client identities, assess risk profiles, and prevent financial crime. The role of KYC in banking extends far beyond a one-time onboarding check. It forms the backbone of anti-money laundering (AML) compliance, fraud prevention, and ongoing customer risk management. Regulatory bodies including FATF and FinCEN require KYC as a condition of operating in global financial markets. The stakes are real: AML and KYC fines surged to over $4.6 billion in 2024, with penalties rising 417% in the first half of 2025. That trajectory tells compliance officers one thing clearly. Weak KYC programs are no longer a manageable risk.

What does the KYC process actually involve?

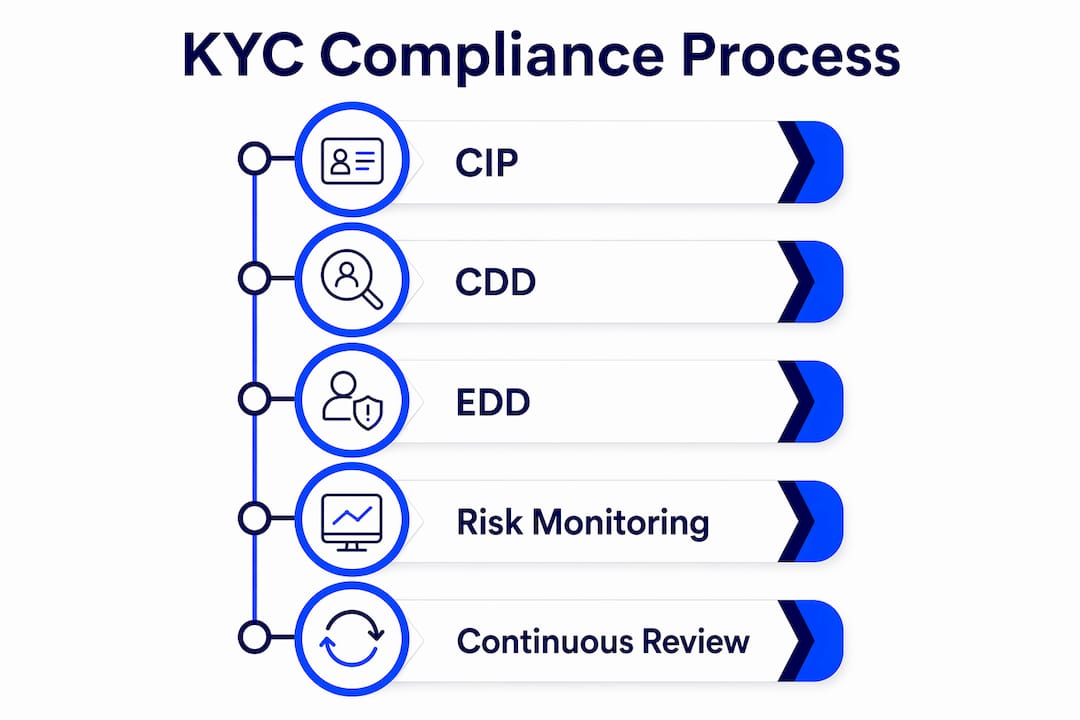

KYC compliance in finance operates through three interconnected components: the Customer Identification Program (CIP), Customer Due Diligence (CDD), and Enhanced Due Diligence (EDD). Each layer serves a distinct function, and together they form a continuous risk management cycle rather than a static checklist.

Customer Identification Program (CIP)

CIP is the foundation. At onboarding, banks collect and verify basic identity information: full legal name, date of birth, address, and government-issued identification. For business clients, this extends to beneficial ownership verification, confirming who ultimately controls the entity. CIP sets the baseline from which all subsequent risk decisions flow.

Customer Due Diligence (CDD)

CDD goes deeper. It profiles the customer’s expected transaction behavior, business purpose, and source of funds. KYC includes CIP and CDD as ongoing elements, not one-time events, meaning banks must continuously monitor whether actual account activity matches the risk profile established at onboarding. A retail client suddenly routing large international wire transfers triggers a CDD review.

Enhanced Due Diligence (EDD)

EDD applies to high-risk customers: politically exposed persons (PEPs), clients in high-risk jurisdictions, and entities with complex ownership structures. EDD requires more intensive documentation, more frequent reviews, and direct senior management sign-off in many regulatory frameworks. The threshold for triggering EDD varies by jurisdiction, but the principle is consistent. Greater risk demands greater scrutiny.

Continuous monitoring ties all three layers together. Transaction monitoring systems flag anomalies against the established customer risk profile, feeding alerts back into the CDD and EDD review cycle.

- CIP: Identity verification at account opening using government documents and beneficial ownership data

- CDD: Ongoing profiling of expected behavior, source of funds, and business purpose

- EDD: Intensified review for PEPs, high-risk jurisdictions, and complex corporate structures

- Continuous monitoring: Transaction analysis measured against the customer’s established risk baseline

Pro Tip: Build your CDD questionnaire around expected transaction patterns, not just static identity data. A customer’s anticipated monthly volume and counterparty geography are the variables most likely to surface risk early.

Why does KYC matter beyond regulatory compliance?

KYC serves three fundamental purposes: regulatory compliance, fraud prevention, and building customer trust. Banks that treat KYC as purely a compliance exercise miss the operational and commercial value embedded in a well-run program.

Fraud prevention is the most direct benefit. Verified identity data makes it significantly harder for bad actors to open accounts under false pretenses, launder proceeds, or finance illegal activity. Banks with weak identity controls become conduits for financial crime, often without knowing it until regulators arrive.

The reputational risk is equally serious. Banks with weak KYC risk correspondent banking relationship terminations, cutting off access to global payment rails. Losing a correspondent banking relationship can effectively shut a bank out of international dollar clearing. That is an existential operational threat, not a compliance footnote.

Customer trust is the less-discussed benefit. Clients, particularly corporate clients, want to bank with institutions that take identity verification seriously. A bank known for lax controls attracts the wrong customers and repels the right ones. Firms that balance thoroughness with efficiency treat KYC as a competitive advantage in compliance.

The cost of poor onboarding design compounds the problem. 70% of financial institutions lost customers in the prior year due to slow or cumbersome onboarding, up from 48% two years earlier. That 22-percentage-point increase signals a market where friction kills conversion. KYC processes in banking that are thorough but slow create a direct revenue leak.

How are risk-based KYC models changing compliance practice?

Traditional KYC refresh cycles operate on fixed schedules: high-risk customers reviewed annually, medium-risk every two years, low-risk every three to five years. The problem is that risk does not move on a calendar.

Check-the-box KYC approaches generate many immaterial outputs and inefficiencies, undermining risk mitigation effectiveness. A scheduled review of a dormant low-risk account consumes analyst time that should go toward a newly active high-risk relationship. The result is a compliance program that looks thorough on paper but misses actual risk signals.

Risk-based KYC models improve compliance effectiveness and reduce costs by focusing on material risk changes and adopting event-driven refresh cycles. The shift is from “when did we last review this customer” to “has anything changed that warrants a review now.”

Event-driven triggers that prompt an immediate KYC refresh include:

- A significant change in transaction volume or counterparty geography

- Negative news screening hits on the customer or associated parties

- A change in beneficial ownership or corporate structure

- Sanctions list additions affecting the customer’s jurisdiction

- Suspicious activity reports filed on the account

Integrating KYC data directly with transaction monitoring enables customer-level compliance reviews rather than isolated alerts, increasing investigative efficiency. When a transaction alert and the customer’s risk profile are visible in the same workflow, analysts resolve cases faster and with better accuracy.

| Approach | Trigger | Output |

|---|---|---|

| Periodic refresh | Fixed calendar schedule | High volume, many immaterial reviews |

| Risk-based refresh | Material risk change or event | Targeted reviews, higher signal quality |

| Event-driven refresh | Specific trigger (news, ownership change) | Immediate, proportionate response |

Pro Tip: Assign a continuous risk score to each customer account that updates automatically when transaction patterns shift. Use that score as the primary trigger for CDD reviews, not the calendar.

What challenges do banks face in KYC compliance?

Over 40% of new customer onboarding time in banks is consumed by KYC due diligence and account opening. That concentration of effort creates a bottleneck that slows revenue generation and frustrates clients before the relationship even begins.

Data fragmentation makes the problem worse. KYC data often sits across multiple systems: onboarding platforms, transaction monitoring tools, sanctions screening databases, and relationship management software. Analysts manually reconcile information across these systems, which introduces errors and delays. The digital banking onboarding process works best when identity data flows automatically between systems rather than being re-entered at each stage.

Effective customer screening depends on internal data standardization before screening begins, reducing false positives and improving risk scoring integrity. Banks that skip this “preflight” step generate high volumes of false positive alerts that consume analyst capacity without producing genuine risk findings.

The key operational challenges compliance teams face:

- Data silos: KYC records stored in disconnected systems prevent a unified customer risk view

- Manual processes: Document collection and verification done by hand creates delays and inconsistency

- False positive overload: Poor data standardization generates screening alerts that waste analyst time

- Regulatory divergence: Different KYC requirements across jurisdictions complicate cross-border onboarding

- Continuous monitoring gaps: Many banks review risk profiles only at scheduled intervals, missing real-time changes

Addressing these challenges requires both process redesign and technology investment. Automated data standardization, integrated compliance workflows, and modern banking compliance trends all point toward the same conclusion. KYC programs that rely on manual effort at scale will always underperform.

Key Takeaways

KYC is the single most consequential compliance process in banking, and banks that treat it as a continuous risk management function rather than a periodic administrative task consistently outperform on both regulatory outcomes and customer retention.

| Point | Details |

|---|---|

| KYC is a continuous process | CIP, CDD, and EDD must operate as an ongoing cycle, not a one-time onboarding check. |

| Non-compliance carries severe costs | AML and KYC fines exceeded $4.6 billion in 2024, with penalties rising 417% in H1 2025. |

| Onboarding friction drives customer loss | 70% of financial institutions lost customers due to slow KYC processes in the prior year. |

| Risk-based models outperform fixed schedules | Event-driven KYC refresh cycles reduce immaterial reviews and improve risk signal quality. |

| Data quality determines screening accuracy | Internal data standardization before screening reduces false positives and improves risk scoring. |

KYC as a risk culture, not a compliance checkbox

The compliance officers I respect most do not talk about KYC as a regulatory obligation. They talk about it as a risk intelligence function. That framing matters more than it sounds.

When KYC is treated as a checkbox, the program optimizes for completion rates and review cycle adherence. When it is treated as risk intelligence, it optimizes for the quality of information and the speed of detection. Those are fundamentally different programs, and they produce fundamentally different outcomes.

The 417% rise in penalties in the first half of 2025 is not a coincidence. Regulators have gotten better at identifying programs that look compliant on paper but fail to detect actual risk. The tell is usually the same: high review volumes, low suspicious activity referrals, and no clear link between KYC data and transaction monitoring outcomes.

The role of AI in fraud prevention is becoming central to this conversation. AI does not replace the judgment of a skilled compliance analyst. It removes the noise so that analyst can focus on the signals that matter. That is the direction KYC programs need to move. Advanced fintechs already treat KYC as a commercial asset that signals institutional maturity to investors and correspondent banking partners. Banks that internalize that view will build programs worth having.

— dd

How Demivolt supports compliant banking operations

Compliance-first banking infrastructure is not optional for businesses operating across borders. Demivolt is built around that reality.

Demivolt’s platform meets EU regulatory standards from the ground up, with segregated client accounts, transparent onboarding workflows, and SEPA and SWIFT payment infrastructure designed for cross-border operations. For businesses that need dedicated IBAN account validation and compliant payment rails without the operational overhead of building compliance programs from scratch, Demivolt provides the infrastructure. The platform’s role-based user management and multi-account structures also support the kind of internal controls that regulators expect to see in a mature compliance program. Explore Demivolt’s full suite of compliance and payment tools to see how they fit your operational needs.

FAQ

What does KYC stand for in banking?

KYC stands for Know Your Customer. It is the mandatory process banks use to verify client identities and assess their risk profiles before and during a banking relationship.

What are the three main components of KYC?

The three core components are the Customer Identification Program (CIP), Customer Due Diligence (CDD), and Enhanced Due Diligence (EDD). CIP verifies identity at onboarding, CDD monitors ongoing risk, and EDD applies intensified scrutiny to high-risk customers.

What happens if a bank fails to meet KYC requirements?

Regulatory fines, reputational damage, and loss of correspondent banking relationships are the primary consequences. AML and KYC penalties exceeded $4.6 billion in 2024 and rose 417% in the first half of 2025.

How does KYC support anti-money laundering efforts?

KYC is the customer-facing component of AML compliance. By verifying identities and monitoring transaction behavior against established risk profiles, banks detect and report suspicious activity before funds move through the financial system.

What is the difference between CDD and EDD?

CDD applies to all customers and involves ongoing risk profiling and transaction monitoring. EDD applies to high-risk customers such as politically exposed persons or clients in high-risk jurisdictions, requiring more intensive documentation and more frequent senior-level review.