Managing international payments, expense controls, and regulatory requirements across multiple accounts creates operational headaches for finance teams and founders. Many platforms limit account structures, lack partner reseller models, or do not publish clear fee schedules, leaving unpredictable costs and missing features. This comparison covers pricing, account setup, automation, and partner programs across five business banking providers so you can match one to your company’s needs without trial and error.

Table of Contents

Demivolt

At a Glance

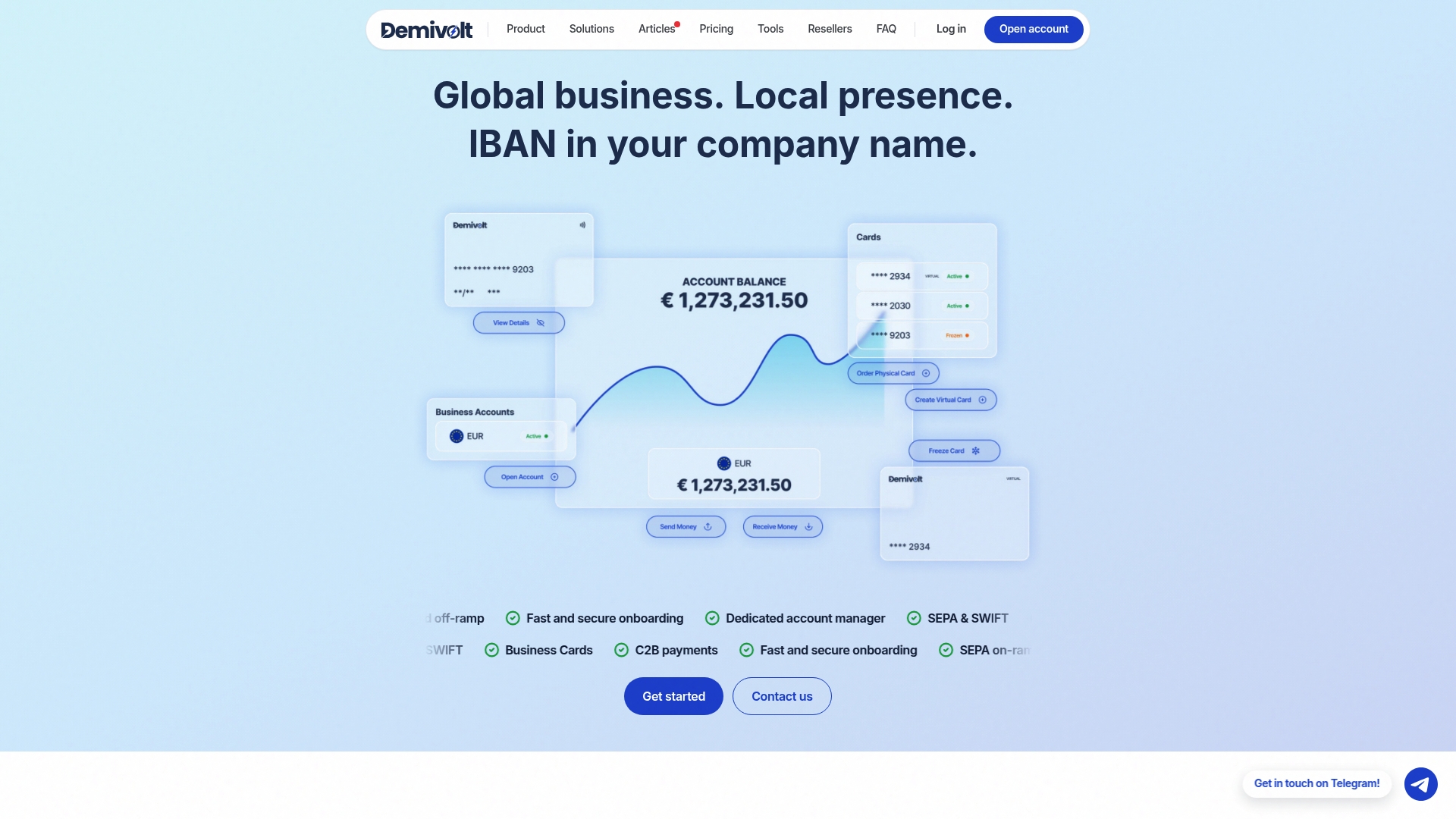

€0.40 per outgoing SEPA transfer and free account setup appear in Demivolt’s published fees. According to the company, Demivolt is a regulated electronic money institution operating under EU financial rules. It combines dedicated IBANs, multiple account structures, and a reseller program for partners to earn recurring commissions.

Core Features

Demivolt issues dedicated business IBANs and supports multiple account structures so companies segregate funds across legal entities or projects. It routes inbound and outbound payments over SEPA and SWIFT and offers role based permission controls for teams. The platform lists virtual cards now with physical cards planned for a later release.

Key Differentiator

That regulatory status sits alongside explicit per transfer fees and a structured reseller program. The vendor emphasizes partner economics rather than only merchant pricing. Partners can onboard client accounts and collect recurring commissions through the reseller workflow.

Pros

That status signals oversight while the vendor publishes clear fees and free account setup to reduce surprises during onboarding. SEPA and SWIFT rails cover common EU and international payment flows. Role based permission controls let you assign duties and reduce operational risk for finance and operations teams.

Cons

- Physical business cards are not yet available, and they are listed by the vendor as upcoming.

Who It’s For

SMEs and fintech enabled companies that need dedicated IBANs and multiple account structures will find the product fits core needs. Digital first regulated businesses seeking transparent fees and predictable cross border costs benefit from the published pricing. Resellers and advisors who want referral commissions can use the reseller program to add recurring revenue.

Unique Value Proposition

Free account setup plus €0.40 per outgoing SEPA transfer gives predictable unit economics for low margin transactions. Charging €25 for SWIFT inbound and €30 for outbound creates clear cross border cost assumptions. That fee clarity helps finance teams model cash flow and vendor payments without hidden fee surprises.

Real World Use Case

A Lithuanian SME uses Demivolt to manage daily EU transactions and separate project accounts. Accountants use roles to control payments, and virtual cards pay for SaaS and marketing costs. Transparent per transfer fees keep monthly bank expenses predictable for the finance lead.

Pricing

Pricing lists free account setup, €0.40 per outgoing SEPA transfer, €25 SWIFT inbound, and €30 SWIFT outbound. The vendor advertises detailed fee calculators on its site to help with volume planning.

Website: https://demivolt.com

Seapoint

At a Glance

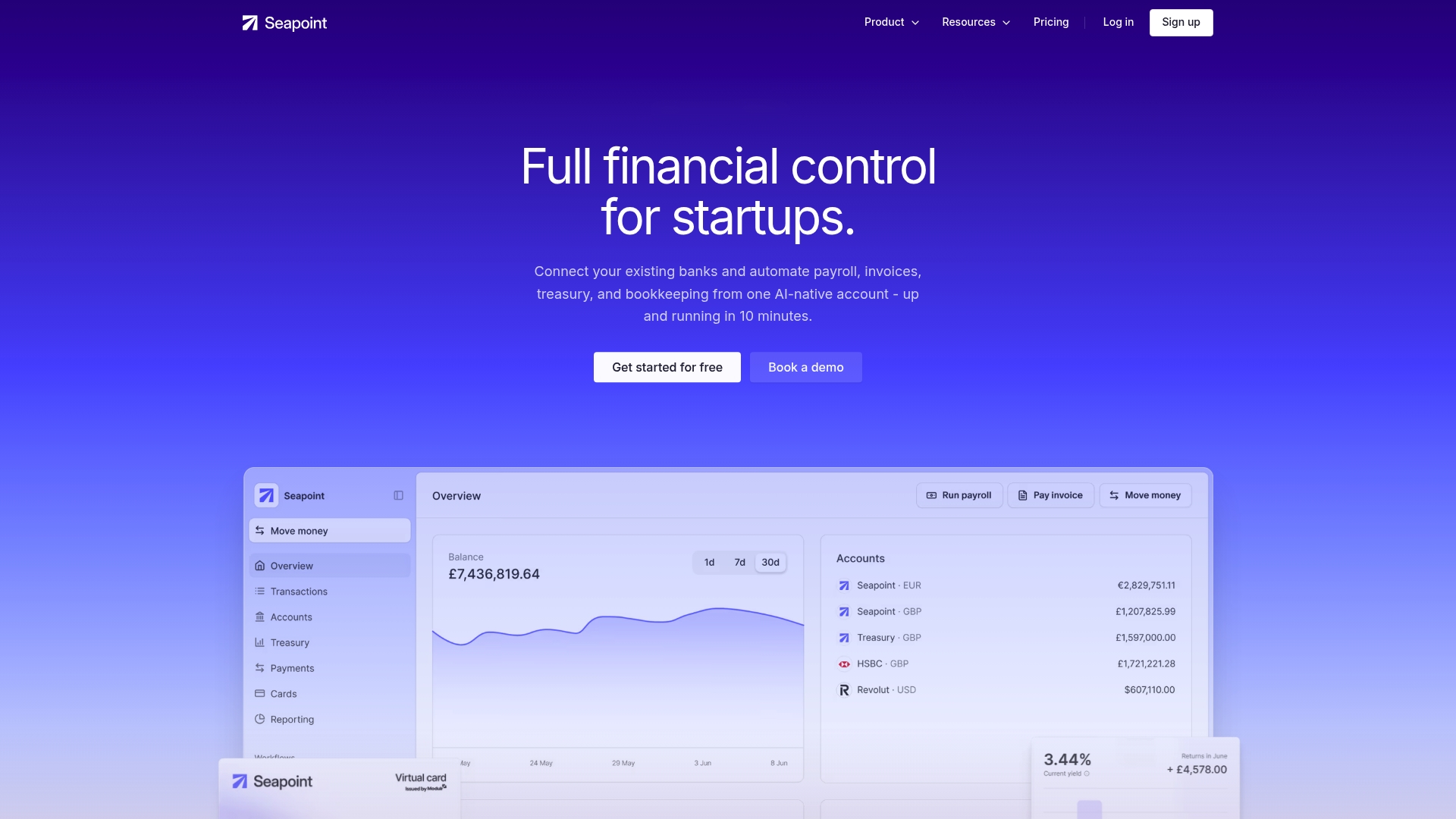

Seapoint reports open banking links to 2,000+ banks. That network powers consolidated cash flow views across multiple accounts in real time. The platform pairs that connectivity with AI workflows that capture invoices from Gmail and automate payroll and bookkeeping. Pricing starts with a free tier and scales to paid growth plans.

Core Features

Seapoint combines AI-powered transaction categorisation with real-time cash flow dashboards so you can spot shortfalls quickly. It connects existing banking rails, bookkeeping, and payment tools and supports invoice capture from Gmail inboxes and automated payroll processing. The product also advertises open banking links that feed live balances and transactions into one unified account.

Key Differentiator

The single strongest angle is the platform’s AI-native automation that pulls banking and financial tools into one dashboard for startups. That focus makes repetitive finance tasks like invoice approvals and bookkeeping low touch for small finance teams. The approach aims specifically at early-stage companies rather than large corporate treasury setups.

Pros

Seapoint offers a free plan that helps very small teams get started without upfront cost, and the paid tiers add reporting and unlimited teams. Connections to common tools cut manual work during onboarding, and the vendor reports fast setup times for bank and Gmail links. The platform highlights real-time financial insights, which helps founders decide when to hire or delay spend.

Cons

- Limited third-party reviews and public validation for the platform.

- No full disclosure of broader integration coverage beyond core financial tools.

- Several items such as Slack integration and full Xero sync are listed as coming soon.

- No dedicated mobile app is mentioned in the feature set.

When It May Not Fit

If your finance team needs a heavily vetted vendor with many independent reviews, this will feel risky. If you require immediate Slack notifications or a complete two-way Xero sync today, the roadmap items mean missing features. If mobile-only access matters, the lack of a stated mobile app is a constraint.

Notable Integrations

- Xero for accounting sync when available.

- Gmail for invoice capture and approval.

- Stripe for payment reconciliation.

- Open banking links to that network of banks for live balances.

Who It’s For

Early-stage founders, finance managers, and small teams that need an integrated finance stack with low setup overhead. Companies that already use Xero, Gmail, or Stripe and want to reduce bookkeeping time will see value. Teams that require enterprise-grade audit trails or a mature app ecosystem may want a different fit.

Real World Use Case

A seed-stage startup connects its bank accounts, Gmail, and Xero. Incoming invoices land in the inbox and the platform captures them for approval. Payroll processes run automatically and cash flow dashboards show live balances, saving hours of manual reconciliation each month.

Pricing

Free tier available. Data & Reporting at £29/month after a three-month trial. Growth at £199/month after a three-month trial. The vendor advertises discounts for early-stage startups on paid plans.

Website: https://seapoint.co

Juni

At a Glance

Juni reports account openings in as little as 24 hours. The vendor advertises cashback rewards of up to 1% on card spend. That combination targets global SMEs that need fast onboarding and cost conscious cross border payments.

Core Features

Juni bundles multi currency accounts with low FX fees and unlimited virtual cards in multiple currencies. Transparent cross border payments show clear exchange rates and the platform supports mobile management for real time control. AI powered automation handles invoicing, expense tracking, and syncs with Fortnox to reduce manual accounting work.

Key Differentiator

Juni integrates multi currency accounts, unlimited virtual cards, and AI powered automation in one product geared toward global SMEs. That integration reduces tool fragmentation for businesses that manage cross border suppliers and online ad spend.

Pros

The platform is easy to use and suits ecommerce and growing businesses, offering unlimited virtual cards for campaign and supplier spend. Cashback and transparent rates help control costs, while a mobile app gives real time visibility. Juni operates under Swedish regulation as an electronic money institution and provides community resources plus dedicated support channels.

Cons

- Account freezes can occur abruptly with little warning, which can halt operations until the issue is resolved.

- Customer support responsiveness varies and some users report unhelpful responses during urgent issues.

- Lack of automated recurring payment features complicates routine expense management.

- Account recovery and recall processes are reported as slow and cumbersome.

When It May Not Fit

If your business cannot tolerate unexpected freezes, Juni may not be a fit. Companies that need built in recurring payment workflows will find feature gaps. Operations that require rapid account recovery for high volume payments should look elsewhere for faster remediation.

Notable Integrations

- Fortnox

- Google Pay

- Apple Pay

Who It’s For

Small and medium sized businesses, especially ecommerce brands, benefit from multi currency accounts and virtual cards. Companies that run international ad campaigns or manage foreign suppliers will find the exchange controls useful. Teams needing accounting automation with Fortnox integration will value the AI driven workflows.

Real World Use Case

A growing online retailer uses Juni’s multi currency accounts and unlimited virtual cards to pay international suppliers. They automate invoicing and expense tracking with AI powered tools and sync records to Fortnox. Invoice credit and transparent FX help them stretch cash and scale across borders.

Pricing

Pricing includes account setup, transaction fees, and optional premium services. See the website for detailed plans and any merchant or FX charges.

Website: https://juni.co

Swan

At a Glance

Swan’s marketing materials state it offers embedded business accounts with full verification and no limits. It issues virtual and local IBANs across Europe and supports physical, virtual, and wallet-compatible cards. The partner-driven model targets platform companies that want banking features inside their apps.

Core Features

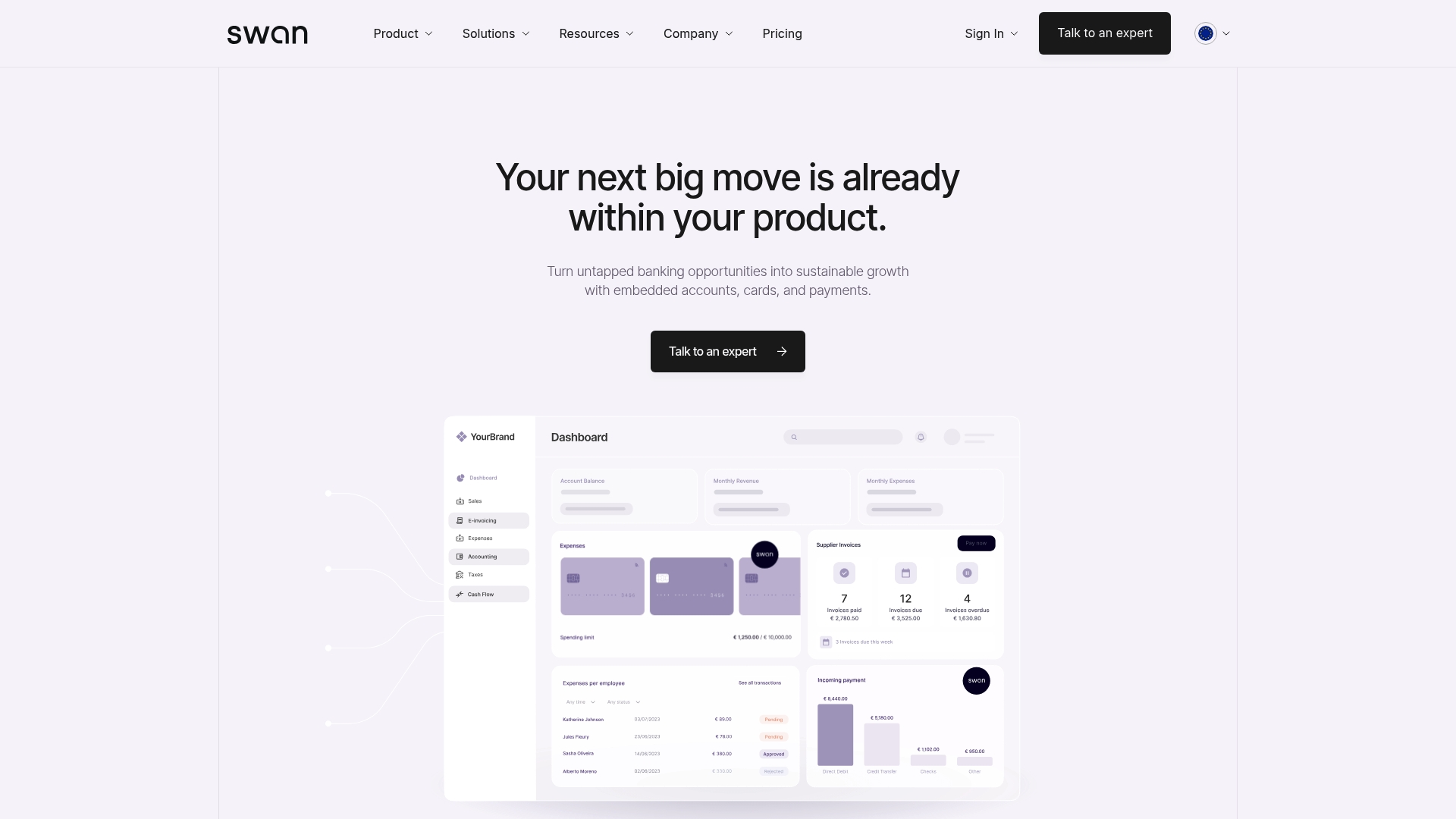

The platform issues embedded business accounts and creates virtual and local IBANs for multiple European countries. Partners can design and issue physical, virtual, and wallet-compatible cards and process SEPA, instant, and international transfers. It accepts card payments, checks, and direct debits where supported and includes onboarding and verification workflows for business customers. APIs let partners control account lifecycle, transfers, and card settings programmatically.

Key Differentiator

Swan bundles embedded accounts, card programs, and cross-border payment rails with local compliance management across several European jurisdictions. This lets platform teams add banking features without handling regulatory licensing themselves. That approach favors software businesses that need regulated banking primitives inside their product.

Pros

Email support is responsive and partner integrations reduce engineering friction during deployment. Onboarding tools make account and card issuance straightforward, which shortens time to live for embedded features. The vendor lists industry leaders among its customers. Swan’s marketing materials state it is backed by a licensed electronic money institution.

Cons

- Some customers report account freezes without clear explanations, which can halt operations.

- There is no phone support, so urgent issues may wait for email responses.

- Resolution processes for technical issues and disputes can feel slow and opaque.

- Certain automated document actions and some transfer types carry relatively high fees.

When It May Not Fit

If you need immediate phone support for incidents, Swan may not meet your responsiveness needs. If your business cannot tolerate unexplained account freezes, the operational risk may be unacceptable. If low transaction fees for automated documents are critical, this platform may prove costly.

Who It’s For

Businesses embedding banking features into SaaS products that serve European customers will find Swan relevant. Examples include accounting, prop-tech, HR tech, health insurance, and travel platforms that need IBANs and card programs. You should have product teams ready to integrate partner APIs and accept a partner-first support model. It suits teams that prefer to offload licensing and compliance to a partner rather than build banking infrastructure.

Real World Use Case

A prop-tech company can use Swan to issue local IBANs and accept rent payments inside its app. That integration automates collections, routes funds to landlords, and issues employee or company cards for property managers. The integration reduces manual reconciliation and brings payments and compliance into the product interface.

Pricing

Not applicable, informational only.

Website: https://swan.io

Revolut Business

At a Glance

Revolut Business reports tiered plans starting from £10/month for basic essentials. The platform centers on multi currency accounts, corporate and virtual cards, and automated expense matching with AI. That mix targets teams that move money across borders and need tight card controls and spending visibility.

Core Features

Revolut Business provides multi currency accounts and global payments alongside card issuance for teams. It combines expense automation with AI receipt matching and built in bills and purchase order controls. Administrators get per user spend controls, approvals, real time notifications, and automated reconciliation.

Key Differentiator

The defining feature is a unified control plane that merges global payments, multi currency balances, and card management. That consolidation lets finance teams view currency exposures and card activity from one dashboard. It emphasizes operational control with spend policies and approvals applied at the card or user level.

Pros

The interface makes routine banking and expense tasks fast and approachable for finance teams. International transfers use interbank rates, which helps lower FX costs for cross border payments. Card management is flexible with virtual and physical cards plus per card limits and instant controls. The platform supports high daily and per transaction limits that suit growing companies. Multi currency support reduces manual conversion steps when paying suppliers or receiving foreign revenue.

Cons

- Clunky expense reporting module can frustrate high volume workflows and complex reconciliation.

- Accounts have been frozen unexpectedly during compliance reviews, which can interrupt operations.

- Onboarding can be lengthy and slow initial cash access for new clients.

- Lacks some traditional lending tools such as detailed loan or overdraft services that large firms often use.

When It May Not Fit

Companies with very high volume expense operations or complex travel and reimbursement policies may find the expense module limiting. Businesses that need guaranteed uninterrupted access during aggressive compliance checks may prefer providers with different compliance flows. Enterprises requiring on site relationship banking or full lending lines will find product gaps.

Notable Integrations

- Xero

- Sage

- QuickBooks

- Accounting and HR software APIs

Who It’s For

Revolut Business fits small to large firms that prioritize international payments and card level spend control. It suits teams that want multi currency accounts and automated reconciliation inside one app. It is less suitable for firms that require full suite lending or highly customized expense workflows.

Real World Use Case

A multinational startup issues virtual cards to remote teams to control vendor spend. The finance lead uses AI receipt matching to speed month end reconciliation. The company pays suppliers in local currencies and reduces conversion steps by holding funds across multiple currency balances.

Pricing

Pricing starts at £10/month for entry level essentials and scales to custom enterprise plans. Each tier changes features and allowances for cards, limits, and automation tools. Enterprises can request bespoke pricing and terms for higher limits or tailored services.

Website: https://revolut.com/business

Comparison of Alternatives

Demivolt stands out among its peers, offering transparent pricing and partner revenue options through its reseller program. Nonetheless, alternative platforms provide unique advantages in automation, cross-border operations, and scalability, ensuring diverse solutions for businesses with distinct needs.

Automation and Integration Prowess

Seapoint excels in its ability to unify multiple financial processes into a singular dashboard, integrating open banking links and AI-driven functionalities. This feature simplifies workflows for startups seeking efficiency gains. Unlike Demivolt, which emphasizes IBAN setup and predictable pricing, Seapoint delivers a streamlined experience for managing invoices, payroll processing, and cash flow analysis dynamically. This capability positions Seapoint as an instrumental tool for nascent ventures prioritizing automation.

Cross-Border and Ecommerce Specialization

Juni caters to ecommerce businesses through its multi-currency accounts and transparent foreign exchange rates, facilitating international transactions and supplier payments. The inclusion of unlimited virtual cards for ad spend makes Juni a preferred platform for scaling online ventures. While Demivolt’s emphasis on structured IBANs aids SMEs with diverse project needs, Juni addresses transaction fluidity and campaign management at a global level.

Best Fit

- SMEs requiring transparent fees should choose Demivolt for its predictable transaction costs and dedicated IBANs.

- Businesses focused on automated finance tasks may favor Seapoint’s integrated dashboard and AI-powered workflows.

- Ecommerce brands handling cross-border costs will benefit from Juni’s multi-currency accounts and virtual card provisions.

- SaaS platforms embedding transaction functions should consider Swan for its localized compliance and API ecosystem.

- Teams prioritizing multicurrency payments might select Revolut Business for its expense matching and user-based card controls.

Our Pick

Demivolt offers superior clarity in fee structures and facilitates partner-driven revenue growth through its reseller program, making it the best choice for SMEs prioritizing straightforward banking solutions. However, platforms like Seapoint and Juni cater to businesses with specific automation or international transaction needs, broadening the selection depending on operational priorities.

Choosing the best platform depends on key features such as pricing structure, target audience, and offered functionalities.

| Product | Key Features | Pricing | Best For | Limitation |

|---|---|---|---|---|

| Demivolt | Dedicated IBANs, SEPA and SWIFT | Free setup, €0.40/transfer | SMEs needing structured accounts and clear cost predictability | Physical cards not yet available |

| Seapoint | AI-powered financial workflows, open banking links | Free plan; paid £29+/month | Startups wanting integrated financial tools with minimal onboarding effort | Limited third-party reviews and missing mobile app |

| Juni | Multi-currency accounts, cashback rewards | Price not published | SMEs managing cross-border payments and international ad spend | Potential abrupt account freezes |

| Swan | Embedded accounts, local IBANs | Price not published | SaaS platforms requiring banking features through API integrations | No phone support, high fees for certain actions |

| Revolut Business | Multi-currency accounts, card management | £10/month and up | Firms needing tight card and spend control across multiple currencies | Complex reconciliation and event-triggered account freezes |

What Challenges Do Businesses Face When Looking for vialet.eu Alternatives?

Companies searching for vialet.eu alternatives often need transparent fees and clear cross-border cost structures. Managing multiple IBAN accounts, overseeing outgoing payments, and enforcing role-based permissions are common challenges. Businesses want a provider that combines regulatory compliance with easy onboarding and reliable payment processing.

Demivolt solves these issues by offering regulated business accounts with dedicated IBANs and published transfer fees, including €0.40 per outgoing SEPA transfer. Its platform supports multi-account structures and role-based user management to give finance teams better operational control. International SMEs and fintech companies benefit from predictable costs and compliant financial infrastructure.

Looking for a reliable alternative to vialet.eu? Explore how Demivolt can help your company manage inbound and outbound payments with confidence. Visit Demivolt to open an account with free setup and start handling your SEPA and SWIFT transfers transparently today.

Learn more about Demivolt

FAQ

What are the fees for outgoing SEPA transfers with Demivolt?

Demivolt charges €0.40 per outgoing SEPA transfer. This clear pricing structure helps businesses anticipate their banking costs without hidden fees.

How does Demivolt compare to Juni for international payments?

Juni offers competitive features such as cashback rewards of up to 1% on card spend. Demivolt, on the other hand, is well-suited for businesses needing transparent pricing and separate account structures, allowing for better management of cash flow across different projects.

Can I manage multiple accounts with Demivolt?

Yes, Demivolt supports multiple account structures. This feature allows businesses to segregate funds across legal entities or projects, facilitating better financial management.

Does Demivolt provide physical business cards?

Currently, Demivolt does not offer physical business cards, but they are planned for a future release. Businesses should consider this while evaluating their immediate banking needs.

What kind of companies will benefit from using Demivolt?

SMEs and fintech-enabled companies that require dedicated IBANs and clear, predictable fees will find Demivolt particularly valuable. Its features support businesses that prioritize transparent pricing and operational control.