TL;DR:

- Banking integration automates data synchronization between banks and business systems, reducing manual reconciliation and enhancing cash visibility. Implementing it requires mapping workflows, assessing compatibility, and establishing governance to ensure security and operational resilience. Effective integration boosts operational efficiency, customer retention, and supports future embedded finance models for SMEs.

Banking integration is defined as the automated synchronization of financial data between a bank and a business’s accounting, ERP, or treasury system, eliminating manual data entry and creating real-time visibility into cash positions. Platforms like FISPAN, Apideck, and NetSuite have made this connectivity accessible to companies far beyond the enterprise tier. The role of banking integration has expanded from a back-office convenience to a core operational requirement, particularly for SMEs and digital-first businesses managing cross-border payments, multi-entity structures, and regulatory compliance simultaneously. Connection methods include RESTful APIs, ISO 20022 messaging standards, and middleware layers that normalize data across heterogeneous bank systems. For any business leader evaluating why integrated banking matters in 2026, the answer starts with what manual reconciliation actually costs you.

What are the key benefits of banking integration for SMEs?

The importance of banking integration becomes concrete when you measure what it replaces. Manual bank reconciliation, duplicate payment entry, and fragmented cash reporting consume finance team hours that produce zero revenue. Financial organizations using API-led automation report 20% to 30% operational cost reductions and process cycle time improvements of 30% to 50%. That means a reconciliation process that took two days can realistically complete in hours, with fewer errors.

The benefits of banking integration extend across four distinct areas:

- Operational efficiency: Payment initiation, reconciliation, and cash reporting run automatically within your ERP or accounting platform. Finance staff shift from data entry to exception handling.

- Cash flow visibility: Real-time bank feeds replace end-of-day batch files, giving treasury teams an accurate intraday liquidity picture. This directly improves working capital decisions.

- Compliance and audit readiness: Integrated systems generate structured audit trails automatically. Access controls using OAuth 2.0 and OpenID Connect enforce role-based permissions, aligning digital authority with legal signatory matrices.

- Customer and vendor experience: Suppliers receive faster payments. Customers interacting with your finance team encounter fewer delays caused by manual processing bottlenecks.

Pro Tip: Before selecting an integration platform, map every manual touchpoint in your current payment and reconciliation workflow. The touchpoints that repeat daily are your highest-value automation targets.

Modern business banking trends confirm that SMEs adopting integrated banking consistently outperform peers on working capital efficiency. The advantage is not theoretical. It shows up in days-sales-outstanding figures, supplier discount capture rates, and audit preparation time.

How does banking integration work?

Banking systems integration operates through a layered technical architecture. Understanding each layer helps you evaluate vendor claims and avoid buying complexity you do not need.

-

API connectivity layer: RESTful APIs are the standard connection method between a bank and a business system. ISO 20022 messaging provides a structured data format for payment instructions and account statements, replacing older formats like MT940 and SWIFT MT messages. Most modern banks and fintechs expose open banking APIs that conform to regional standards such as PSD2 in Europe.

-

Authentication and security layer: OAuth 2.0 handles delegated authorization, meaning your ERP requests data from the bank on your behalf without storing your banking credentials. OpenID Connect adds identity verification on top of OAuth 2.0. These protocols are non-negotiable for any production integration handling real funds.

-

Middleware and unified API layer: A unified API platform, such as Apideck or FISPAN, sits between your business system and multiple banks. Instead of building a separate connector for each bank, your engineering team builds once to the unified API. Unified API layers minimize bespoke connector development and reduce duplicated effort across data normalization, authentication, change management, and partner rollout.

-

Data normalization layer: Different banks return account data in different formats. Normalization converts all incoming data to a consistent schema before it enters your ERP, preventing reconciliation mismatches caused by formatting inconsistencies.

-

Event-driven synchronization: Rather than polling the bank every few minutes, event-driven architectures push updates to your system the moment a transaction occurs. This is what enables genuine real-time cash visibility rather than near-real-time approximations.

| Integration method | Best suited for | Key limitation |

|---|---|---|

| Direct bank API | Single-bank, high-volume operations | Requires separate build per bank |

| Unified API platform | Multi-bank, multi-currency SMEs | Platform dependency and licensing cost |

| Middleware connector | Legacy ERP environments | Can become permanent technical debt |

| File-based (SFTP/MT940) | Low-frequency reconciliation needs | No real-time capability |

Pro Tip: If your business operates accounts at more than two banks, a unified API platform almost always delivers a lower total cost of ownership than building direct integrations, even after platform fees.

TD Bank’s embedded banking products and FISPAN’s ERP connector demonstrate how this architecture works in production. Both route payment instructions from within the ERP interface directly to the bank’s core system, with confirmation returned to the ERP in seconds.

What challenges should businesses anticipate in banking integration?

The challenges of banking integration are real, and underestimating them is the most common reason projects stall. Legacy platform complexity is the primary barrier for 70% of banks in integration efforts. For SMEs, the equivalent challenge is an accounting platform or ERP that predates open banking standards and lacks native API support.

Security governance is not optional. Financial organizations face an average data breach cost of $5.9 million, the highest of any industry. A poorly governed integration, one with stale API tokens, unrevoked access for departed employees, or unencrypted data in transit, creates a direct path to that exposure.

Integration governance, security, and operational resilience matter more than technical connectivity alone. A working API connection that lacks lifecycle management is a liability, not an asset.

Additional challenges worth planning for include:

- Integration sprawl: Temporary middleware solutions become permanent fixtures. Each connector added without documentation increases the risk of silent failures during bank API version updates.

- Approval workflow remapping: Transitioning approval workflows from bank portals to ERP-integrated systems requires remapping internal authority to maintain compliance and security. A payment limit that existed in the bank portal must be recreated as a rule in the ERP.

- Reconciliation gaps during migration: Legacy and modern systems often coexist for months. Automated parallel reporting catches discrepancies before full cutover, but this requires deliberate planning, not an afterthought.

- API lifecycle neglect: Token refresh schedules, consent expiry dates, and interface version deprecations require ongoing attention. Neglecting API lifecycle management produces unexpected outages that appear to users as product bugs.

For guidance on building security into your payment workflows from the start, the digital banking security checklist covers the governance controls most relevant to cross-border operations.

How does banking integration impact customer experience and growth?

The impact of banking integration on customer experience is measurable and significant. Banks on the FISPAN platform see 30% to 50% deposit growth from connected clients, alongside 8% net-new customer acquisition. The mechanism is straightforward: businesses that can initiate payments, view balances, and reconcile transactions without leaving their ERP have no operational reason to switch banks.

The retention dynamic runs in both directions. According to Datos Insights and Nine Wave survey data, 85% of CFOs would switch banks for direct ERP connectivity. That figure defines the competitive stakes. If your bank does not offer ERP integration, your most financially sophisticated clients are actively evaluating alternatives.

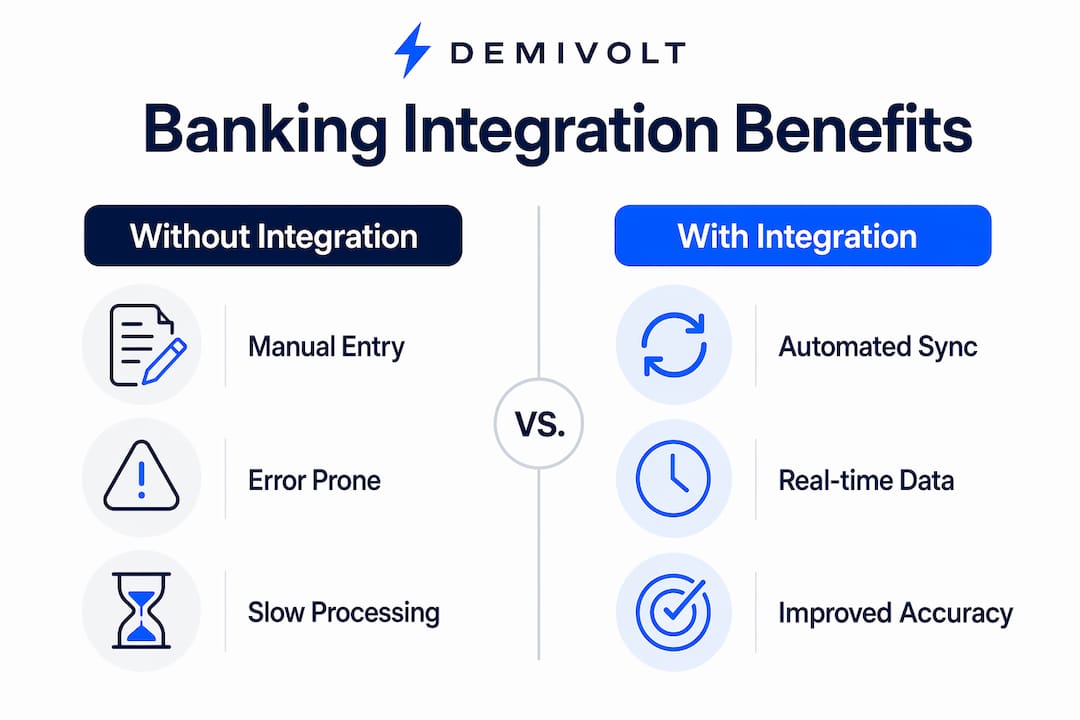

| Without banking integration | With banking integration |

|---|---|

| Manual CSV exports and imports | Automated real-time data sync |

| Multiple portal logins per bank | Single ERP interface for all accounts |

| Delayed cash position reporting | Intraday liquidity visibility |

| High exception and error rates | Structured reconciliation with audit trail |

| Slow payment approval cycles | ERP-embedded payment initiation and approval |

For digital-first businesses, the advantages of integrated banking go beyond convenience. Embedded finance capabilities, where banking functions live inside the product your customers already use, create switching costs that no pricing strategy can replicate. A company that processes payroll, manages supplier payments, and monitors cash flow entirely within its ERP platform has built its banking relationship into its operational infrastructure.

What practical steps should SMEs take to implement banking integration?

Effective implementation of banking systems integration follows a sequence that most failed projects skip.

-

Map your payment and reconciliation journeys end to end. Identify every point where a human manually moves data between a bank and a business system. These are your integration targets. Prioritize by frequency and error rate.

-

Assess technical compatibility. Confirm whether your ERP or accounting platform supports native API connections or requires middleware. Platforms like NetSuite, SAP, and Microsoft Dynamics 365 have established banking connector ecosystems. Smaller platforms may require a unified API intermediary.

-

Choose a phased rollout. Start with the highest-impact, lowest-risk integration point, typically automated bank statement import and reconciliation. Add payment initiation in a second phase once reconciliation is stable.

-

Select your integration architecture deliberately. If you bank with multiple institutions, evaluate unified API platforms before committing to direct integrations. The 2026 SME integration guide covers the decision criteria in detail.

-

Establish governance before go-live. Document every API connection, its owner, its token refresh schedule, and its version dependency. Define the process for revoking access when employees leave or roles change.

-

Validate with parallel operation. Run your new integration alongside your existing process for at least two reconciliation cycles. Phased integration with reconciliation validations catches discrepancies before they affect financial reporting.

-

Monitor operational metrics post-launch. Track onboarding cycle time, payment exception rates, reconciliation completion time, and audit trail completeness. These four metrics tell you whether the integration is delivering its intended value.

Pro Tip: Engage a partner with both banking compliance expertise and technical integration experience. Most integration failures trace back to teams that understood the technology but not the financial authority and approval structures the technology was replacing.

Key takeaways

Banking integration delivers measurable operational, compliance, and growth advantages only when it is treated as a continuous program, not a one-time technical project.

| Point | Details |

|---|---|

| Core definition | Banking integration automates data sync between banks and ERP or accounting systems, eliminating manual reconciliation. |

| Efficiency gains | API-led integration reduces operational costs by 20% to 30% and cuts process cycle times by 30% to 50%. |

| Governance is non-negotiable | API lifecycle management, access controls, and approval workflow remapping are required for security and compliance. |

| Customer retention driver | 85% of CFOs would switch banks for direct ERP connectivity, making integration a competitive differentiator. |

| Implementation sequence | Map journeys, assess compatibility, phase the rollout, establish governance, and validate with parallel operation before full cutover. |

Why integration strategy separates resilient businesses from reactive ones

Most business leaders I speak with treat banking integration as an IT project. That framing is the first mistake. Integration is a product decision. When your payment initiation fails because an API token expired, your finance team does not experience a technical outage. They experience a broken product. That distinction changes how you resource, govern, and maintain the work.

The second pattern I see consistently is underestimating approval workflow complexity. Moving payment authorization from a bank portal into an ERP sounds straightforward. In practice, it requires mapping every signatory limit, every dual-approval rule, and every currency restriction into the ERP’s permission structure. Companies that skip this step discover the gap during an audit, not before.

Unified API models genuinely change the economics for engineering teams at SMEs. Building one integration to a platform like Apideck or FISPAN, rather than three separate bank connectors, is not just faster. It means your team maintains one authentication flow, one data schema, and one version dependency. That reduction in cognitive load has a compounding effect on delivery speed over time.

The future of banking integration points toward embedded finance becoming the default, not the premium option. Businesses that build integration governance into their operational processes now will adapt to that shift without disruption. Those that treat integration as a checkbox will find themselves rebuilding from scratch when their bank deprecates an API version or their ERP vendor changes its connector architecture.

— dd

How Demivolt supports banking integration for modern SMEs

Demivolt is built for exactly the operational requirements this article describes. The platform provides dedicated IBAN accounts, SEPA and SWIFT payment management, and role-based user controls that align digital permissions with your internal authority structure. For SMEs managing cross-border payments or multi-entity structures, Demivolt’s API-driven infrastructure connects directly with external banking workflows without requiring bespoke connector development.

Start with Demivolt’s free IBAN validation tool to verify payment accuracy before transactions process, or explore the full SEPA tools suite to support compliant payment workflows. For businesses ready to evaluate a regulated, digital-first banking platform, Demivolt’s business banking solutions are designed to reduce onboarding friction and support audit-ready financial operations from day one.

FAQ

What is the role of banking integration in business operations?

Banking integration automates the exchange of financial data between a bank and a business’s ERP or accounting system, eliminating manual reconciliation and providing real-time cash visibility. It also enforces structured audit trails and access controls that support regulatory compliance.

How does banking integration work technically?

Banking integration uses RESTful APIs or ISO 20022 messaging to connect bank systems with business platforms, secured through OAuth 2.0 authentication. Unified API platforms like Apideck or FISPAN normalize data across multiple banks into a single interface, reducing the need for separate connectors.

What are the biggest challenges of banking integration?

Legacy platform incompatibility, API lifecycle neglect, and inadequate approval workflow remapping are the three most common failure points. Financial organizations also face an average data breach cost of $5.9 million, making security governance a critical requirement from the start.

Why does banking integration matter for customer retention?

Survey data shows 85% of CFOs would switch banks to gain direct ERP connectivity, meaning integration is a retention tool as much as an efficiency tool. Banks offering embedded ERP integration see 30% to 50% deposit growth from connected clients.

What is the first step to implementing banking integration for an SME?

Map every manual touchpoint in your current payment and reconciliation workflow before evaluating any technology. This exercise identifies your highest-value automation targets and prevents you from buying integration capability you do not actually need.