TL;DR:

- External banking integration consolidates multiple accounts, payment channels, and data feeds into a unified platform using APIs. It enhances real-time cash visibility, reduces manual errors, and strengthens compliance controls, especially for SMEs managing several banking relationships. Building standardized, reusable connections with proper governance and data normalization is essential for maximizing operational and strategic benefits.

External banking integration is the practice of connecting multiple bank accounts, payment rails, and financial data feeds into a single automated platform through APIs and standardized protocols. For SMEs and cross-border companies managing relationships with two or more banking partners, the reasons for banking integration come down to three things: real-time cash visibility, fewer manual errors, and tighter compliance controls. Technologies like OAuth 2.0, EBICS, and SWIFT messaging make this possible today without rebuilding your core financial infrastructure from scratch.

Why integrate external banking for your business operations

The core case for connecting your banks is operational. When payment data lives in separate portals across Barclays, ING, and a local payment provider, your finance team reconciles manually. That process is slow, error-prone, and gives your CFO a cash position that is always hours or days behind reality. External banking integration solves this by pulling all transaction data into one ledger view automatically.

The benefits of external banking integration extend well beyond convenience:

- Unified cash position. Multi-bank integration eliminates reconciliation delays by consolidating balances across all banking partners into a single view. Companies managing 5 to 15 banking relationships gain the most from this, because the manual overhead of logging into each portal compounds quickly.

- Fewer failed payments. Garanti BBVA’s Request to Pay API demonstrates this directly: by sending payment requests programmatically, businesses remove the manual login friction that causes collections to fail. Fewer failed payments means better cash flow and less time spent chasing receivables.

- Audit trails and compliance. Every API-driven transaction generates a timestamped record. That record supports internal controls, external audits, and regulatory reporting without additional manual documentation.

- Reduced reconciliation labor. Automated data pulls replace the spreadsheet-based matching that finance teams perform at month-end. This frees analysts to focus on forecasting rather than data entry.

Pro Tip: Before selecting an integration approach, map every banking relationship your company holds and categorize each by payment volume and transaction type. This prevents over-engineering a connection for a low-volume account and under-investing in one that processes your highest-value payments.

What technologies power modern external banking integration?

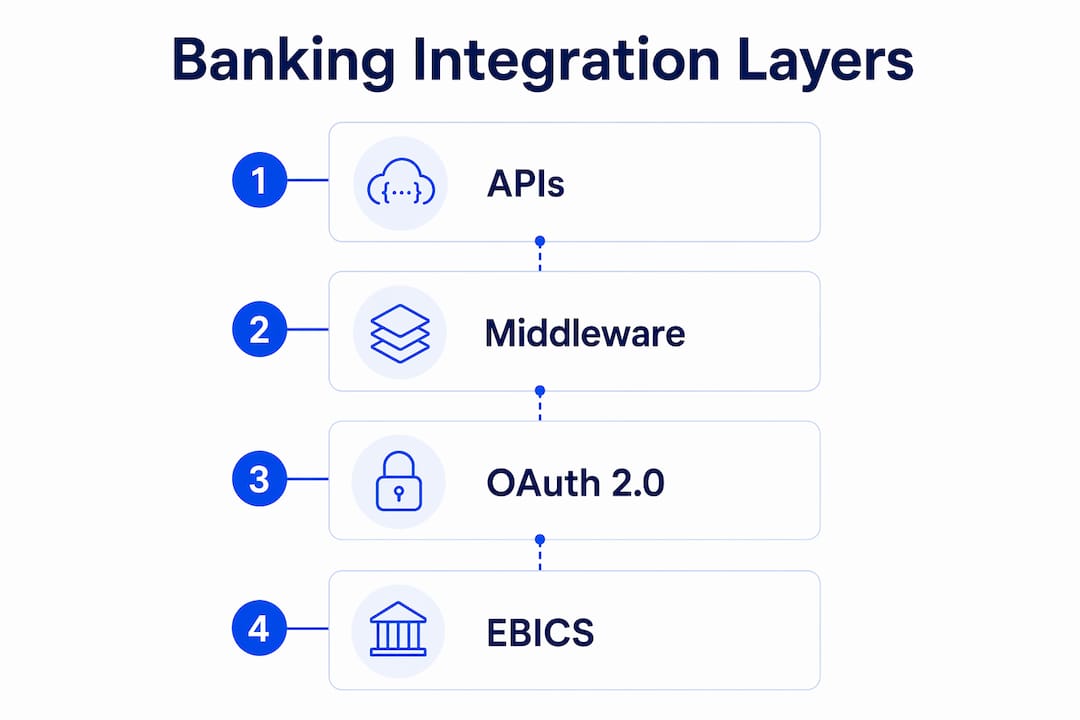

The technical foundation of external banking integration rests on three layers: APIs for real-time data exchange, security protocols for consent and access control, and standardized messaging formats for payment execution.

APIs and middleware are the primary connectors. A banking API exposes account balance, transaction history, and payment initiation endpoints that your ERP, accounting platform, or treasury management system can call directly. Middleware platforms act as translation layers when your internal systems speak a different data format than the bank’s API. This architecture means you do not need to rebuild your accounting software to connect a new banking partner.

OAuth 2.0 governs how your systems request and maintain access to bank data. The OAuth consent flow issues authorization codes, exchanges them for access tokens, and enforces scope constraints that limit what data each integration can read or write. Managing token refresh cycles and consent revocation is an ongoing operational requirement, not a one-time setup task. If a token expires without renewal, your data feed goes dark until someone manually re-authorizes the connection.

EBICS (Electronic Banking Internet Communication Standard) handles bulk corporate payments, particularly across European markets. EBICS onboarding requires contract signing with the bank, subscriber initialization, and a public key certificate exchange before a single payment can be transmitted. This is not a five-minute setup. Plan for two to four weeks of coordination with each banking partner that uses this standard.

Here is a comparison of the three primary integration standards:

| Standard | Best use case | Onboarding complexity | Real-time capability |

|---|---|---|---|

| REST API (Open Banking) | Account data, payment initiation | Low to medium | Yes |

| EBICS | Bulk corporate payments, Europe | High | No (batch) |

| SWIFT | Cross-border wire transfers | High | Near real-time |

Pro Tip: Build your integration layer as a reusable connector, not a point-to-point link. A centralized integration layer standardizes orchestration and policy enforcement across all bank connections, so adding a new banking partner does not require rebuilding governance rules from scratch.

What challenges do businesses face when connecting multiple banks?

The advantages of connecting banks are clear, but the path to achieving them is not always straightforward. Multi-bank integration projects fail most often because of three underestimated problems.

- Data normalization. Every bank delivers transaction data in a slightly different format. One bank uses ISO 20022 XML, another delivers CSV files, and a third returns JSON through its API. Inconsistent data models delay CFO-level reporting even when the raw data arrives in real time. Your integration layer must normalize these formats before they reach your accounting system, or reconciliation becomes a manual task again.

- Security governance at scale. Each new banking connection expands your attack surface. The global average cost of a data breach reached $4.88 million in 2024, with financial services among the highest-cost sectors. This means that adding a fifth or tenth banking connection without updating your access controls, monitoring, and incident response procedures is a measurable financial risk, not just a technical concern. Review your cross-border compliance checklist before expanding your banking network.

- Consent lifecycle management. OAuth 2.0 tokens expire. EBICS certificates require renewal. When your team does not track these expiration dates, integrations break silently. A payment initiation that worked last Tuesday fails this Tuesday because a token was not refreshed. Building a consent and certificate monitoring process is as important as the initial connection setup.

- Onboarding complexity per bank. Each banking partner has its own contract process, technical documentation, and testing environment. For a company adding three new banking relationships in a single year, this overhead is significant. Standardizing your onboarding checklist and using a middleware platform that already holds certified connections to major banks cuts this time substantially.

Pro Tip: Embedded treasury tools work well when you operate with a single primary bank. Once you add a second or third banking partner, embedded solutions fall short and a dedicated integration layer becomes the more cost-effective architecture.

How does banking integration improve financial decision-making?

The operational improvements from external banking integration translate directly into better financial decisions. Here is where the business case becomes concrete.

Liquidity forecasting accuracy improves when your treasury team sees all cash positions in real time rather than pulling yesterday’s statements from three separate portals. A cross-border SME with accounts in Germany, the Netherlands, and Poland can see its total available liquidity within seconds rather than waiting for a morning reconciliation run. That visibility changes how the CFO manages working capital and when the company draws on credit facilities.

Faster product and service launches become possible because reusable integration connectors decouple your financial operations from the constraints of any single banking core. When your payment infrastructure is abstracted into an API layer, adding a new payment method or entering a new market does not require renegotiating your entire banking setup. This is a structural advantage for companies scaling across borders.

Automated cash application reduces the manual matching of incoming payments to open invoices. When your bank API pushes transaction data directly into your ERP, the system matches payments automatically using reference numbers and amounts. Finance teams at SMEs using this approach report significant reductions in manual entry errors and faster invoice closure cycles.

The table below shows how integration affects key financial operations:

| Operation | Without integration | With integration |

|---|---|---|

| Cash position visibility | Daily, manual | Real-time, automated |

| Payment reconciliation | Manual matching | Automated via API data |

| Compliance reporting | Spreadsheet-based | Timestamped audit trail |

| New bank onboarding | Weeks of manual setup | Reusable connector deployment |

For SMEs managing multi-account structures, the shift from manual to automated reconciliation alone can recover several hours of finance team time per week. At scale, that compounds into a material reduction in operational cost.

Key takeaways

External banking integration delivers measurable business value only when governance, data normalization, and token lifecycle management are treated as core operational requirements alongside the technical connection itself.

| Point | Details |

|---|---|

| Unified cash visibility | Connecting multiple banks into one ledger eliminates daily manual reconciliation and gives CFOs real-time data. |

| Security scales with connections | Each new banking link expands risk exposure; governance and monitoring must expand in parallel. |

| Standards vary by use case | REST APIs suit real-time data; EBICS handles bulk payments; SWIFT covers cross-border wires. |

| Data normalization is non-negotiable | Inconsistent bank data formats block accurate reporting even when raw data arrives in real time. |

| Reusable connectors cut long-term cost | A centralized integration layer reduces per-bank setup effort and enforces consistent policy across all connections. |

The part most integration guides skip

Most articles on external banking integration focus on the technical setup and stop there. The harder question is governance: who owns the token renewal calendar, who monitors for silent integration failures, and who updates the security policy when you add banking partner number six?

I have seen well-funded finance teams build technically sound integrations that break within six months because no one owned the operational layer. A token expires on a Friday afternoon. The payment run fails Monday morning. The CFO finds out when a supplier calls. The integration was not the problem. The absence of a process owner was.

The shift toward unified banking and accounting API ecosystems, driven by Open Banking mandates in the EU and the UK, will reduce some of this friction by 2027. Standardized consent frameworks and pre-certified bank connectors will lower onboarding complexity. But the governance requirement does not disappear. It just moves upstream.

My advice for any SME starting an integration project in 2026: treat the consent lifecycle and certificate management schedule as a financial control, not an IT task. Put it on the same calendar as your tax filing deadlines. And before you connect a second or third bank, read the secure cross-border payments checklist to make sure your access controls are ready for the expanded attack surface.

Integration is a business enabler. But it earns that title only when the operational discipline matches the technical ambition.

— dd

How Demivolt supports your banking integration

Demivolt is built for exactly the scenario this article describes: SMEs and cross-border companies that need multiple banking relationships to work together without the manual overhead. The platform provides dedicated IBAN accounts, SEPA and SWIFT payment management, and an API-driven infrastructure that connects cleanly with your existing financial systems. Before you initiate any payment integration, use Demivolt’s IBAN validator tool to confirm account data accuracy and prevent failed transactions at the source. For companies managing multi-bank setups, Demivolt’s SEPA payment tools reduce validation errors and support compliant, efficient payment flows across borders. Explore how Demivolt can serve as your integration-ready banking partner at demivolt.com.

FAQ

What does external banking integration mean for an SME?

External banking integration connects your business bank accounts and payment systems to your financial software through APIs, giving you automated data flows and a unified view of cash across all banking partners.

What is the biggest challenge in multi-bank integration?

Data normalization is the most common bottleneck. Banks deliver transaction data in different formats, and without a normalization layer, your reconciliation process remains partially manual even after the technical connection is live.

How does OAuth 2.0 relate to banking integration security?

OAuth 2.0 manages the authorization tokens that grant your systems access to bank data. Tokens expire and must be renewed on a defined schedule; an unmanaged token expiration breaks your data feed without warning.

Is EBICS or a REST API better for corporate payments?

REST APIs suit real-time account data and payment initiation for most SME use cases. EBICS is the standard for bulk corporate payment files in European markets and requires a more involved onboarding process including certificate exchange with the bank.

How does banking integration support compliance?

Every API-driven transaction generates a timestamped, immutable record that supports audit trail requirements and regulatory reporting. This replaces manual documentation and reduces the risk of gaps in your compliance records.

Recommended

- Demivolt | Blog – Why digital banking empowers SMEs for smarter cross-border finance

- Demivolt | Blog – Modern business banking trends: boost efficiency & compliance

- Demivolt | Blog – Digital banking explained: streamline cross-border success

- Demivolt | Blog – Business banking for SMEs: services, compliance & cross-border