TL;DR:

- Inbound payments are funds received and validated into a business account that confirm a completed transaction. Managing their lifecycle, methods, and compliance requirements is essential to maintain liquidity and operational efficiency.

An inbound payment is defined as the receipt, validation, and posting of funds from external entities into a business account to settle a financial transaction. The industry term for this process is “incoming payment,” and both phrases describe the same event: money arriving in your account from a customer, partner, or financial institution. Understanding how inbound payments work is not optional for business owners. It directly affects your liquidity, your ability to pay suppliers, and your compliance standing with regulators.

What is an inbound payment and why does it matter?

An inbound payment confirms that a transaction is complete and that funds are now available in your account. Until that posting happens, a sale is just a promise. In B2B contexts especially, inbound payments are the trigger for liquidity realization. You cannot pay staff, reorder inventory, or fund operations on an unpaid invoice.

Payment networks like ACH, SWIFT, and Fedwire are the infrastructure that carries these funds from the sender’s bank to yours. Each network has different rules, speeds, and data requirements. Knowing which network your payment traveled through tells you when to expect the funds and what to do if something goes wrong.

The inbound payment definition also covers digital payment platform receivables, such as funds arriving from Stripe, PayPal, or similar processors before they settle to your bank account. These follow the same basic lifecycle but add an intermediary layer that can affect timing and visibility.

How do inbound payments work?

The lifecycle of an inbound payment follows a clear sequence from initiation to posting.

- Initiation. The sender instructs their bank to transfer funds. They provide your account details, the amount, and a payment reference.

- Routing. The sending bank routes the payment through a network. Domestic wire transfers in the US travel via Fedwire. International transfers use SWIFT for routing and correspondent banking chains. ACH payments batch and route through the ACH network.

- Verification. Your bank receives the payment message and runs validation checks. These include sanctions screening, AML checks, and confirmation that the account number and routing details match.

- Posting. Once verified, the funds post to your account ledger and become available.

Wire transfers settle same-day if the payment arrives before the bank’s cut-off time. ACH payments typically take 1–3 business days. That difference matters when you are managing tight cash flow windows.

Not every inbound payment flows through automatically. Non-STP (manual) workflows handle exceptions such as missing beneficiary data or failed validation checks. Manual intervention adds delays and sometimes fees. Businesses that send incomplete payment instructions create these exceptions on the receiving end.

Pro Tip: Set up real-time payment notifications through your banking platform. Knowing the moment a payment posts lets you act on it immediately rather than reconciling at end of day.

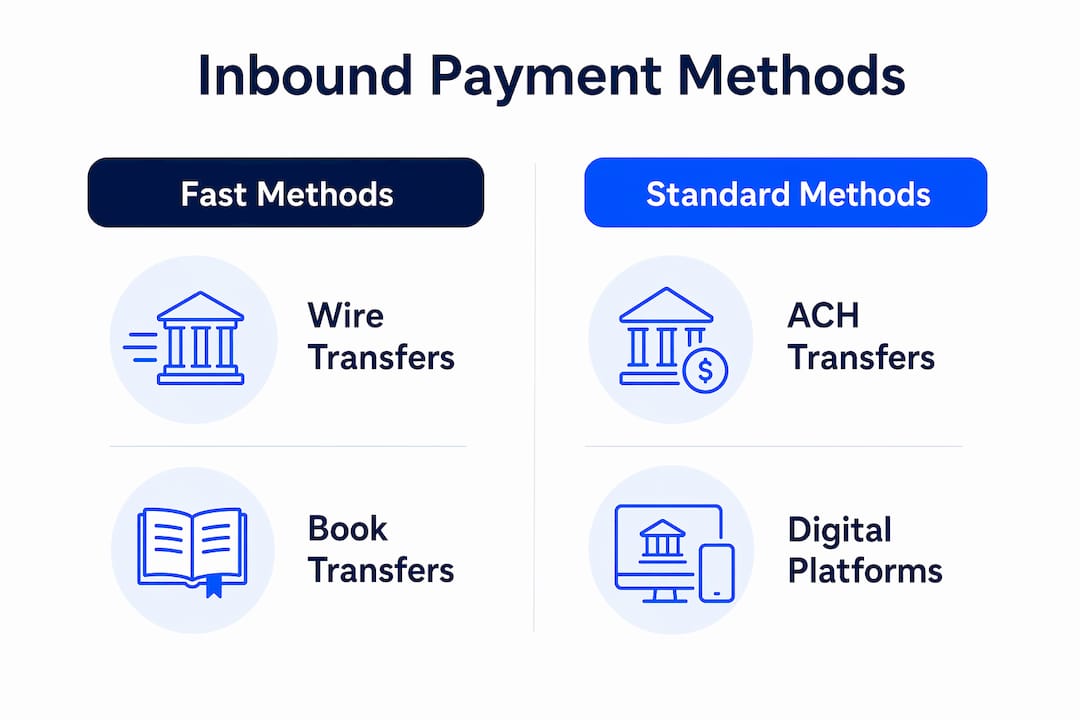

What are the different types of inbound payment methods?

Inbound payment processing varies significantly depending on the method used. Each method carries different trade-offs in speed, cost, finality, and risk.

Wire transfers are fast and irrevocable once sent. That irrevocability is a double-edged quality. It protects you as the recipient because the funds cannot be clawed back without your consent. It also means errors are harder to correct. Wire transfers suit high-value or time-sensitive transactions.

ACH transfers are the workhorse of routine B2B payments in the US. They carry lower fees than wires but come with a reversal window. A sender can initiate an ACH reversal for a limited period after the transfer, which means funds you see in your account are not always final. Businesses that assume ACH finality immediately can run into cash flow problems if a reversal occurs.

Book transfers, or same-bank transfers, settle fastest and at the lowest cost because no interbank routing is needed. If both you and your customer bank at the same institution, the transfer is an internal ledger adjustment. Interbank payments route through intermediaries, which adds both time and cost.

| Method | Speed | Fees | Finality | Best use case |

|---|---|---|---|---|

| Wire transfer | Same day | Higher | Irrevocable | High-value, urgent payments |

| ACH transfer | 1–3 business days | Low | Reversible window | Routine recurring payments |

| Book transfer | Instant | Minimal | Immediate | Same-bank counterparties |

| SWIFT (international) | 1–5 business days | Variable | Generally irrevocable | Cross-border B2B transactions |

| Digital platform (e.g., Stripe) | Hours to days | Percentage-based | Platform-dependent | E-commerce, subscription billing |

Pro Tip: If a customer offers to pay via book transfer, prioritize it. You get the funds faster, with no reversal risk, and at near-zero cost.

What compliance and data requirements affect inbound payments?

Compliance is not a back-office concern. Missing or incorrect data on an inbound payment can freeze your funds before they ever reach your account.

Cross-border inbound payments must include an international flag, complete originating institution details, and accurate account holder information. Regulators require this data to perform AML screening and sanctions checks. When that data is absent or wrong, the receiving bank places the payment on hold pending investigation. That hold can last days.

Domestic payments face fewer data requirements but are not exempt. AML rules apply to all transactions above reporting thresholds, and your bank must be able to identify the source of funds. Businesses operating in regulated industries, such as financial services or real estate, face heightened scrutiny on incoming funds.

The compliance checklist for SMEs receiving international payments covers the core requirements. The practical steps for your business include:

- Collect full sender details before issuing an invoice, including legal entity name, address, and bank details.

- Include a clear payment reference on every invoice so your bank can match the incoming payment to the correct transaction.

- Maintain an audit trail for all inbound payments, including timestamps, network identifiers, and verification outcomes.

- Screen your own customers against sanctions lists before accepting payment, not just after.

- Use a banking platform that flags incomplete inbound payment data before it causes a hold.

Digital tools reduce compliance risk significantly. Platforms that validate IBAN numbers at the point of entry catch errors before a payment is even initiated. That one step alone prevents a large share of inbound payment rejections.

Why are inbound payments critical for cash flow and operations?

Inbound payments are the confirmation signal that your business is functioning. Every payment received is proof that a customer completed their obligation and that your account balance reflects real, usable funds.

Active management of inbound payments strengthens liquidity and builds financial credibility with suppliers and lenders. A business that knows exactly when payments will arrive can plan purchases, payroll, and investments with confidence. A business that does not track inbound payments operates on guesswork and reacts to shortfalls rather than preventing them.

Clear payment terms directly influence when and how reliably inbound payments arrive. Terms that specify due dates, accepted payment methods, and penalties for late payment reduce ambiguity for your customers. Early payment discounts are a proven tool for accelerating inbound payment timing without damaging client relationships.

Poor inbound payment management has concrete consequences. Cash shortages force businesses to draw on credit lines at cost. Delayed payments to suppliers strain relationships and can result in lost preferential pricing or supply disruptions. Inaccurate cash flow forecasts, caused by untracked or misposted inbound payments, lead to bad financial decisions.

Pro Tip: Negotiate net-15 or net-30 terms as your standard, and offer a 1–2% early payment discount for payment within 7 days. Many customers will take it, and the cost of the discount is far lower than the cost of a cash shortfall.

Key Takeaways

Inbound payments are the operational foundation of business liquidity, and managing them well requires understanding their lifecycle, method differences, and compliance requirements.

| Point | Details |

|---|---|

| Core definition | An inbound payment is funds received, validated, and posted to your account from an external source. |

| Method matters | Wire transfers are fast and irrevocable; ACH carries a reversal window that affects true finality. |

| Compliance is non-negotiable | Missing sender data on cross-border payments triggers holds and delays that freeze your funds. |

| Payment terms drive timing | Clear due dates and early payment incentives directly improve when inbound payments arrive. |

| Active monitoring pays off | Tracking inbound payments in real time supports accurate forecasting and prevents cash shortfalls. |

The part most businesses get wrong about inbound payments

Most business owners treat inbound payments as a passive event. Money arrives, the bookkeeper records it, and everyone moves on. That approach works until it doesn’t.

The businesses I’ve seen struggle most with cash flow are not the ones with bad customers. They are the ones with no system. They don’t know which payments are in transit, which are held for compliance review, and which are simply late. When a wire doesn’t arrive by end of day, they don’t know whether to call the customer or call the bank.

The shift that changes everything is treating inbound payment management as a proactive discipline. That means knowing your cut-off times for same-day wire settlement. It means understanding that an ACH credit in your account is not final for several business days. It means building your invoices and contracts around payment terms that actually reflect how you want to receive money, not just what feels polite to ask for.

Regulatory pressure on inbound payments is increasing, not decreasing. The UK banking regulations affecting transfers in 2026 illustrate a broader trend: more data, more screening, more documentation required at every step. Businesses that build compliance into their payment processes now will face fewer disruptions as requirements tighten.

The practical advice is simple. Use a banking platform that gives you visibility into payment status before funds post. Validate IBANs before you send invoices. Write payment terms into every contract, not just the invoice. And when a payment is late, follow up within 24 hours. The longer you wait, the harder the conversation gets.

— dd

How Demivolt supports your inbound payment processes

Demivolt’s platform gives business owners direct visibility into inbound and outbound payment activity through dedicated IBAN accounts that meet EU regulatory standards.

For businesses receiving international payments, Demivolt’s free IBAN validator tool checks account numbers against ISO 13616 standards before a payment is initiated, catching errors that would otherwise cause holds or rejections. The free SEPA tools suite supports compliance checks and payment formatting for businesses operating within European payment networks. Demivolt’s segregated account structure also means your incoming funds are protected and clearly attributed from the moment they post.

FAQ

What is the inbound payment definition in simple terms?

An inbound payment is money received into your business account from an external source, such as a customer or partner, to settle a transaction. The funds go through validation and posting before they are available to use.

How long does inbound payment processing take?

Wire transfers settle same-day if received before the bank’s cut-off time. ACH transfers typically take 1–3 business days, and international SWIFT payments can take 1–5 business days depending on the correspondent banking chain.

What is the difference between inbound vs outbound payments?

An inbound payment is funds arriving in your account. An outbound payment is funds leaving your account to pay a supplier, employee, or other party. Both require accurate data and compliance checks, but inbound payments also require your bank to validate the sender’s information.

Why do inbound payments get held or rejected?

Payments are held or rejected when required data fields are missing or incorrect, such as incomplete originating institution details or a failed sanctions check. Cross-border payments are especially vulnerable to holds when international flags or sender information are absent.

How can I improve the reliability of inbound payments?

Set clear payment terms on every invoice, validate customer IBAN numbers before invoicing, and use a banking platform that provides real-time payment status notifications. Early payment discounts also accelerate inbound payment timing without requiring legal enforcement.