TL;DR:

- Payment infrastructure is a layered system of technology and institutions that enables secure money transfer between buyers and sellers.

- Different provider types offer varying control, costs, and regulatory responsibilities, making license verification essential.

Payment infrastructure is the integrated ecosystem of technology, financial institutions, regulatory rules, and networks that enables secure money movement between buyers and sellers. Every time a business collects a payment, this system handles authorization, routing, fraud screening, and settlement. The core components include payment gateways, processors, acquirers, card networks like Visa and Mastercard, and orchestration layers. Understanding how this system works is not optional for decision-makers. It directly shapes your transaction costs, cash flow timing, compliance exposure, and your ability to operate across borders.

What is payment infrastructure and how is it structured?

Payment infrastructure is built across three distinct layers, each handling a different stage of the transaction. The presentation layer covers customer-facing interfaces: checkout pages, payment forms, and card entry screens. The orchestration layer sits in the middle, handling routing logic, fraud prevention, and provider selection. The processing layer is where the actual financial movement happens, across card networks, acquiring banks, and settlement systems.

Each layer contains specialized components with defined roles. Understanding those roles prevents costly mistakes when selecting or switching providers.

| Component | Primary function |

|---|---|

| Payment gateway | Captures and tokenizes card data at the point of checkout |

| Payment processor | Builds authorization messages and routes them to card networks |

| Acquirer | Holds the merchant account and settles funds after authorization |

| Card network | Facilitates fund transfer between issuing and acquiring banks |

| Orchestrator | Routes transactions across multiple providers to maximize approval rates |

Gateways encrypt sensitive card data the moment a customer submits payment. Processors then carry that authorization request to the relevant card network. Acquirers receive the approved transaction and deposit funds into the merchant’s account. Orchestrators sit above all of these, directing traffic based on cost, geography, or success rate.

Pro Tip: Providers like Stripe unify gateway, processor, and acquirer functions behind a single API. That simplifies onboarding but reduces your ability to negotiate pricing or switch components independently.

How does payment infrastructure work from capture to settlement?

The payment lifecycle follows a defined sequence. Each step involves a different component, and a failure at any point can result in a declined transaction or delayed funds.

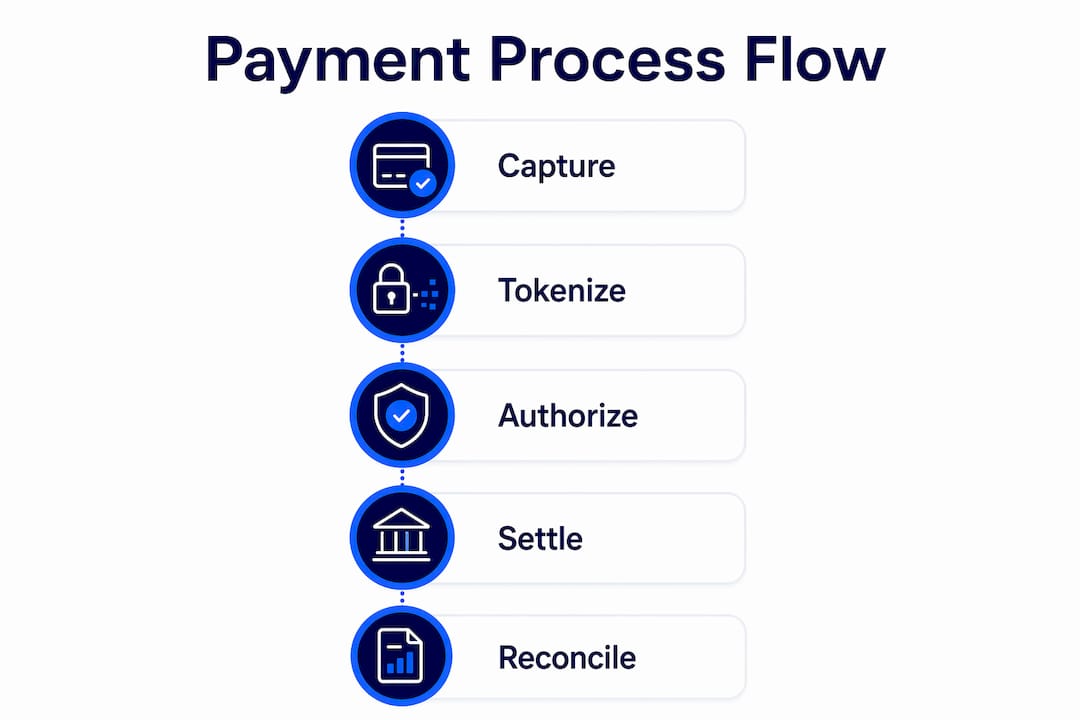

- Payment capture. The customer enters card details at checkout. The gateway encrypts and tokenizes this data before it leaves the browser.

- Authorization request. The processor formats an authorization message and sends it to the card network, which routes it to the card-issuing bank.

- Issuer decision. The issuing bank approves or declines based on available funds, fraud signals, and account status.

- Response routing. The approval or decline travels back through the network to the processor, then to the gateway, and finally to the checkout interface.

- Capture and batching. Approved transactions are captured and grouped into a settlement batch, typically at end of day.

- Settlement. The acquirer transfers funds to the merchant account. Settlement timing typically ranges from T+1 to T+3 days depending on the acquiring relationship.

- Reconciliation. The business matches settled amounts against transaction records to confirm accuracy.

Settlement timing matters more than most businesses realize. A T+3 cycle on high-volume days can create a meaningful cash flow gap, especially for SMEs managing payroll or supplier payments on tight schedules.

Security measures operate throughout this sequence. Tokenization replaces raw card numbers with non-sensitive tokens that are useless if intercepted. 3D Secure adds an authentication step between the issuer and the cardholder, shifting fraud liability away from the merchant. Both are now standard requirements under EU regulations.

Pro Tip: Relying on a single provider across every step creates a single point of failure. If that provider experiences downtime, every transaction fails. Multi-provider routing eliminates that risk by distributing traffic across backup processors.

What types of payment infrastructure providers exist?

The provider market divides into four categories, each offering a different level of control, cost, and regulatory responsibility.

- Payment Service Providers (PSPs). PSPs offer bundled access to gateway, processing, and sometimes acquiring services. They are functional categories, not banking institutions. Verifying their license type, specifically whether they hold an Electronic Money Institution (EMI) license or a standard payment institution license, is critical to evaluating partner regulatory risk.

- Acquirers and banks. Acquirers hold the merchant account and manage the settlement relationship directly. A direct acquiring relationship gives you more control over settlement timing, chargeback management, and pricing. It also requires more compliance work to establish.

- Payment Facilitators (PayFacs). PayFacs onboard merchants under a master account, which accelerates setup. The tradeoff is reduced autonomy. PayFacs control settlement timing and chargeback handling on your behalf, which limits your visibility and negotiating power.

- Orchestrators. Orchestrators sit above PSPs and acquirers, routing transactions dynamically across multiple providers. They do not process payments themselves. Their value is in maximizing approval rates and reducing dependency on any single provider.

The distinction between PSPs and banks trips up many businesses. A PSP may look and feel like a bank account, but it operates under different rules. Fund safeguarding practices vary significantly between license types, and that difference matters when a provider fails or freezes accounts.

Full-stack providers simplify onboarding but restrict pricing flexibility. Businesses at scale benefit from modular stacks with multiple providers, because that separation gives you the ability to negotiate each component independently and route around failures.

Why does compliance and regulatory licensing matter in payment infrastructure?

Compliance is not a background concern. It defines which providers you can legally use, which markets you can operate in, and how your customers’ funds are protected if something goes wrong.

The World Bank supports payment reforms in over 120 countries, with an explicit focus on international standards that ensure safe cross-border operations. That scale reflects how central payment infrastructure is to economic stability, not just business efficiency.

“Compliance is no longer a check-the-box exercise. Choosing partners with transparent regulatory licensing and deep market knowledge is key to operational reliability.” — Corefy on regulatory influence

The CPMI-IOSCO Principles for Financial Market Infrastructures set the global benchmark for safe payment system design. Adoption of these principles supports cross-border operations and financial system stability. Businesses that choose partners aligned with these standards reduce their exposure to regulatory action and operational disruption.

Regulatory complexity increases with geography. A provider licensed in one EU member state may not be authorized to operate in every market you serve. The international compliance checklist for cross-border operations is longer than most SMEs expect. E-money authorization, fund safeguarding requirements, and data localization rules all vary by jurisdiction. Selecting a partner without verifying their specific licenses in your target markets is a material business risk.

Transparency from your provider is non-negotiable. You need to know exactly which entity holds your funds, under which license, and what happens to those funds if the provider enters insolvency. Segregated accounts are the standard protection mechanism. Providers that cannot answer these questions clearly are not suitable partners for serious business operations.

Key Takeaways

Payment infrastructure is the layered system of gateways, processors, acquirers, card networks, and orchestrators that moves funds securely from customer to merchant, governed by licensing rules that vary by jurisdiction.

| Point | Details |

|---|---|

| Three-layer structure | Payment infrastructure spans presentation, orchestration, and processing layers with distinct components at each level. |

| Settlement timing affects cash flow | Settlement cycles range from T+1 to T+3 days, creating cash flow gaps that SMEs must plan for. |

| Provider type determines control | PSPs, PayFacs, acquirers, and orchestrators offer different levels of autonomy, cost, and compliance responsibility. |

| License verification is non-negotiable | Confirm whether a PSP holds an EMI license or standard payment institution license before committing to a partnership. |

| Compliance scales with geography | Operating across borders requires verifying provider authorization in each target market, not just your home jurisdiction. |

The case for building a modular payment stack from day one

Most businesses choose their first payment provider based on ease of onboarding. That is a reasonable starting point. The problem comes when that initial choice calcifies into permanent dependency.

Full-stack providers like Stripe are genuinely good at what they do. They reduce time to first transaction and handle a lot of compliance complexity behind the scenes. But the pricing model is fixed, the routing logic is opaque, and switching costs grow every year you stay. By the time a business is processing meaningful volume, the cost of that convenience becomes measurable.

The businesses I have seen manage payment infrastructure well share one trait: they treat their payment stack the way they treat their technology stack. They separate concerns. Gateway, processor, acquirer, and orchestrator are distinct functions that can be sourced from distinct providers. That separation gives you negotiating leverage, routing flexibility, and the ability to replace one component without rebuilding everything.

Regulatory knowledge is the other factor that separates good infrastructure decisions from expensive ones. A provider that cannot clearly explain their fund safeguarding model, their license scope, or their chargeback process is a liability. The benefits of digital payment platforms are real, but only when the underlying compliance architecture is sound.

My honest advice: audit your current stack against the three-layer model. Identify where you have single-provider dependency. Then ask your providers the hard licensing questions before you need the answers in a crisis.

— dd

Demivolt’s tools for payment validation and compliance

Building sound payment infrastructure starts with getting the basics right. Accurate IBAN validation and SEPA compliance are foundational for any business managing European payments.

Demivolt provides free, ISO 13616-compliant IBAN validation that checks account numbers before transactions are submitted, reducing failed payments and reconciliation errors. The platform also offers a full suite of SEPA payment tools designed for businesses that need reliable, compliant transfer workflows across EU markets. Demivolt’s business banking platform supports dedicated IBAN accounts, SEPA and SWIFT payments, and segregated fund safeguarding under EU regulatory standards. For decision-makers building or auditing their payment operations, these tools provide a practical starting point.

FAQ

What is payment infrastructure in simple terms?

Payment infrastructure is the network of technology, institutions, and rules that moves money from a customer’s account to a merchant’s account. It includes gateways, processors, acquirers, card networks, and the compliance frameworks that govern them.

What are the main types of payment infrastructure providers?

The four main types are PSPs, acquirers, Payment Facilitators, and orchestrators. Each offers a different level of control, pricing flexibility, and regulatory responsibility.

How long does payment settlement take?

Settlement typically takes T+1 to T+3 business days depending on the acquiring relationship and the card network involved. Faster settlement is available through some acquirers at higher cost.

Why does provider licensing matter for businesses?

A provider’s license type, whether an EMI license or a standard payment institution license, determines how your funds are safeguarded and what regulatory protections apply. Choosing an unlicensed or incorrectly licensed provider creates direct financial and legal risk.

What is the difference between a payment gateway and a payment processor?

A payment gateway captures and encrypts card data at checkout. A payment processor takes that encrypted data and routes the authorization request to the card network and issuing bank. They are separate functions, though some providers combine both.