TL;DR:

- Outbound payments are transfers initiated by businesses to external parties, reducing cash reserves. Managing them effectively relies on selecting the right payment rail, validating recipient data, and automating workflows for accuracy.

An outbound payment is any transfer of funds initiated by a business to an external party, reducing cash reserves and directly affecting operational liquidity. The term covers every payment a company sends out: supplier invoices, employee payroll, tax remittances, and loan repayments. Outbound payments appear alongside inbound flows on cash flow statements, making them a core measure of financial health. Understanding how they work, which payment rails to use, and how to automate them gives business owners and financial professionals a real edge in managing cash flow.

What is an outbound payment, and why does it matter?

An outbound payment is defined as any business-initiated fund transfer to an external recipient that reduces the company’s cash position. The industry also uses the term “outgoing payment,” though the two carry a subtle but important distinction. “Outbound payment” describes the full orchestration process, including rail selection, API routing, and compliance checks. “Outgoing payment” refers more narrowly to the specific accounting entry that records the debit in a general ledger.

This distinction matters in practice. A finance team that treats both terms as identical risks misaligning its payment operations with its accounting records, creating reconciliation gaps. Cash flow statements capture outbound payments as operating, investing, or financing outflows, and each category carries different implications for financial analysis. A business with strong revenue but poorly managed outbound payment timing can still face a liquidity crisis.

Common examples of outbound payment transactions include paying a supplier in Germany via SEPA, wiring funds to a manufacturer in Asia through SWIFT, running a domestic payroll via ACH, or reimbursing employee expenses through virtual card settlements. Each example involves a different payment rail, a different cost structure, and a different settlement timeline.

What are the main types of outbound payment options?

The payment rail you choose determines speed, cost, and the amount of remittance data that travels with the funds. The four primary rails for outbound transactions in 2026 are:

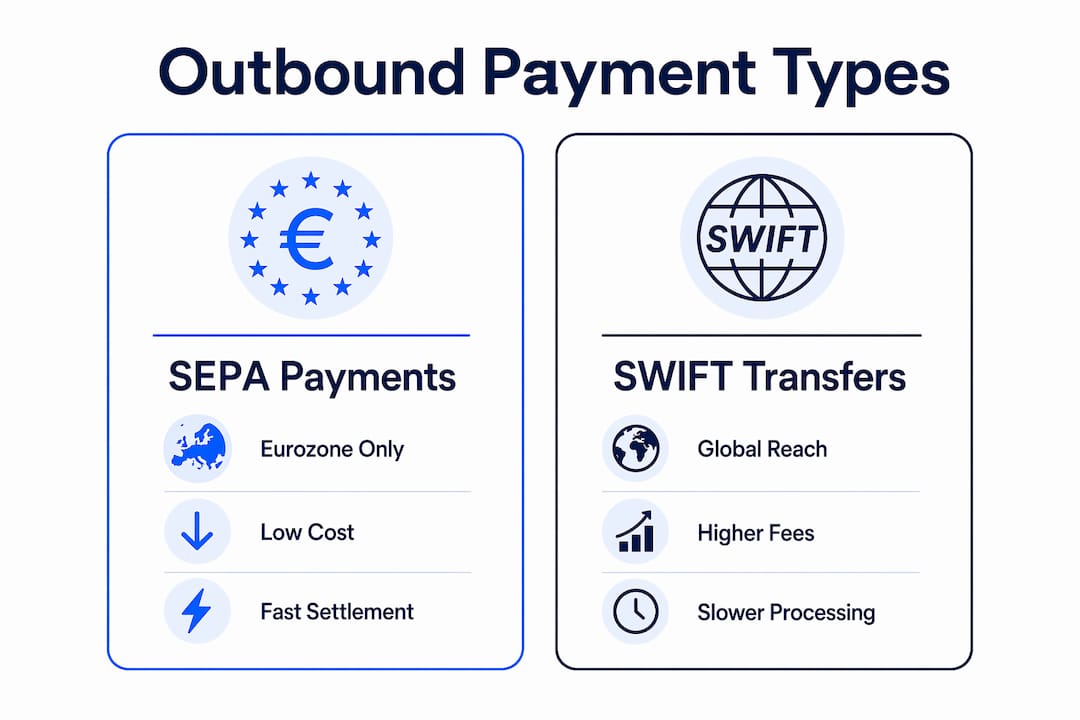

- SWIFT: The global standard for cross-border wire transfers. Settlement takes 2–5 business days and involves correspondent banks, which add intermediary fees. SWIFT carries rich remittance data fields, making it the preferred rail for high-value or complex transactions that require detailed reconciliation.

- SEPA: The Single Euro Payments Area network covers 36 European countries. Standard SEPA credit transfers settle the next business day. SEPA instant payments settle in under 10 seconds, giving EU businesses a fast, low-cost option for euro-denominated outbound transfers.

- FedNow and RTP: These domestic instant rails in the United States settle in seconds to minutes. They are cost-effective for domestic payroll, vendor payments, and disbursements, though their remittance data capacity is more limited than SWIFT.

- ACH: The Automated Clearing House network processes batched domestic payments overnight or within one business day. ACH is the workhorse of U.S. payroll and recurring vendor payments due to its low per-transaction cost.

Cross-border outbound payments add layers of complexity beyond rail selection. Currency conversion, regulatory compliance in the recipient’s country, and intermediary bank fees all affect the final cost and arrival time. A payment from a U.S. company to a supplier in Japan involves FX conversion, potential correspondent bank fees, and compliance checks in both jurisdictions. Choosing the right rail depends on the payment corridor, the currency pair, and whether speed or data richness takes priority.

Pro Tip: For euro-denominated payments within the EU, SEPA instant is almost always the better choice over SWIFT. It is faster, cheaper, and sufficient for most B2B transactions under standard value thresholds.

How does outbound payment processing work?

Every outbound payment moves through four distinct stages before funds reach the recipient. Understanding each stage helps financial professionals identify where errors occur and where automation delivers the most value.

- Initiation. A payment instruction is created, either manually by a finance team member or automatically by an ERP system, accounts payable platform, or API trigger. The instruction includes the recipient’s account details, the amount, the currency, and the payment reference.

- Validation. The system checks the payment data before execution. This includes verifying the recipient’s IBAN or account number against real-time banking databases, confirming available funds, and screening against sanctions lists. Validating payment data before execution reduces failed transactions and costly repair fees by up to 20%. That figure represents real money: repair fees from correspondent banks and the administrative cost of reprocessing failed payments add up quickly at scale.

- Routing. The validated instruction is sent to the appropriate payment rail. The routing decision depends on the destination country, currency, required speed, and cost parameters set by the business. API-based payment systems make this routing decision automatically based on predefined rules.

- Accounting. Once the payment clears, the system posts the debit to the general ledger and updates the accounts payable record. Enterprise accounting systems integrate payment orchestration with ledger posting to prevent discrepancies between bank movements and accounting records, avoiding what practitioners call “ghost accounting” errors.

Pro Tip: Always validate recipient banking details at the initiation stage, not after a failed payment. Real-time IBAN validation tools catch errors before they become expensive problems.

What should you consider when choosing a payment rail?

Selecting a payment rail is not just a technical decision. It directly affects your reconciliation workload, your cash flow timing, and your transaction costs. The right choice depends on four factors: speed, cost, data richness, and geographic coverage.

Speed and data richness often pull in opposite directions. Instant rails like FedNow and SEPA instant settle in seconds, but they carry less remittance data than SWIFT. For a simple vendor payment with a single invoice reference, that limitation is irrelevant. For a complex payment covering multiple invoices, partial credits, and deduction codes, the limited data fields of instant rails create reconciliation headaches on the receiving end.

Cost is the second variable. SWIFT transfers carry correspondent bank fees that can range from a flat charge to a percentage of the transaction value, depending on the corridor. SEPA and domestic instant rails are significantly cheaper per transaction. For high-volume, low-value payments, the cost difference between rails compounds quickly across thousands of transactions per month.

Geographic coverage sets the outer boundary of your rail options. SEPA covers 36 countries but only processes euro-denominated payments. SWIFT reaches virtually every country but at higher cost and slower speed. For businesses operating across multiple regions, a payment compliance checklist that maps rail availability by corridor prevents costly routing mistakes.

Pro Tip: Build a simple rail-selection matrix for your most common payment corridors. Map each corridor to its preferred rail based on value, currency, and required settlement speed. This removes guesswork from daily payment decisions and reduces errors.

How does automation improve outbound payment reliability?

Automation changes the economics and reliability of outbound payment operations. Manual payment processing introduces errors at every stage: wrong account numbers, duplicate payments, missed approval steps, and delayed reconciliation. Automating approval flows and reconciliation controls reduce these risks while cutting the administrative overhead that finance teams spend on payment management.

The specific benefits of API-driven payment automation include:

- Real-time status tracking. Legacy systems often provide payment status only after clearing, which can take hours or days. API-based systems deliver status updates at each stage of the payment lifecycle, from initiation through settlement. This visibility lets treasury teams manage cash positions with current data rather than estimates.

- Reduced manual errors. Automated data validation at the initiation stage catches formatting errors, invalid IBANs, and missing fields before they cause failed payments. The cost of a failed cross-border payment, including repair fees and reprocessing time, far exceeds the cost of preventing it.

- Improved cash flow forecasting. When payment status is available in real time, finance teams can build accurate short-term cash flow models. Knowing exactly when funds will leave the account, and confirming when they have, removes the uncertainty that makes cash flow forecasting unreliable.

- Audit trail integrity. Automated systems log every action taken on a payment instruction, from creation through approval and execution. This creates a complete audit trail that supports both internal controls and external regulatory requirements.

Modern fintech platforms connect to cross-border payment infrastructure through cloud-native APIs, giving businesses the same payment orchestration capabilities that were previously available only to large banks. For SMEs managing outbound payments across multiple currencies and corridors, this access is a practical advantage.

Key Takeaways

Outbound payments are business-initiated fund transfers that reduce cash reserves, and managing them well requires choosing the right rail, validating recipient data, and automating workflows to maintain accuracy and cash flow visibility.

| Point | Details |

|---|---|

| Outbound payment definition | Any business-initiated transfer to an external party that reduces the company’s cash position. |

| Rail selection trade-offs | Faster rails like SEPA instant offer speed; SWIFT offers richer remittance data for complex reconciliation. |

| Validation reduces failures | Validating recipient IBANs before execution cuts failed payments by up to 20% and avoids repair fees. |

| Automation improves visibility | API-driven systems provide real-time payment status, reducing forecasting uncertainty and manual errors. |

| Terminology distinction | “Outbound payment” covers full orchestration; “outgoing payment” refers to the specific accounting entry. |

The detail most businesses overlook in payment management

Most finance teams focus on payment speed and cost when evaluating outbound payment options. Those factors matter, but the detail that causes the most operational pain is data completeness. I have seen businesses switch to instant payment rails to cut costs, then spend more time on manual reconciliation because the rails could not carry enough remittance information to match payments to invoices automatically.

The fix is not to avoid instant rails. It is to design your payment instructions so that the reference data you need travels with the payment, even within the constraints of the rail. For SEPA payments, that means using the structured remittance field correctly. For domestic ACH, it means standardizing your payment reference format so your ERP can match it automatically on the other side.

The second thing I would flag is the accounting distinction between outbound payment orchestration and outgoing payment entries. If your payment system and your accounting system are not tightly integrated, you will eventually encounter ghost accounting: payments that left the bank but never posted correctly to the ledger, or ledger entries with no corresponding bank movement. Maintaining a single source of truth in your ERP for both payment status and accounting entries is not optional at any meaningful transaction volume. It is the foundation of accurate financial reporting.

The businesses that manage outbound payments well treat payment operations as a financial control function, not just a back-office task. That shift in perspective changes how they invest in tools, how they structure approval workflows, and how they measure payment performance.

— dd

Demivolt tools for cleaner outbound payment operations

Accurate recipient data is the single most preventable source of failed outbound payments. Demivolt’s free IBAN validator tool checks account numbers against the ISO 13616 standard in real time, catching formatting errors before they reach the payment rail. For businesses processing SEPA transfers regularly, the full suite of free SEPA tools on the Demivolt platform supports payment initiation and validation without additional software costs.

Demivolt’s business banking platform gives companies dedicated IBAN accounts, SEPA and SWIFT payment management, and role-based user controls built for teams that need both speed and compliance. For businesses managing outbound payments across multiple currencies and European corridors, Demivolt provides the infrastructure to do it accurately and efficiently.

FAQ

What is the outbound payment definition in accounting?

An outbound payment is any business-initiated transfer of funds to an external party that reduces the company’s cash balance. In accounting, it is recorded as a debit to accounts payable or an expense account and a credit to cash or a bank account.

How are outbound payments different from inbound payments?

Outbound payments flow from the business to external recipients, reducing cash reserves. Inbound payments flow into the business from customers or other sources, increasing cash reserves.

Which payment rail is best for international outbound transfers?

The best rail depends on the corridor, currency, and required speed. SWIFT suits high-value transfers needing rich remittance data. SEPA instant is the fastest and cheapest option for euro payments within the 36-country SEPA zone.

How does SEPA compare to SWIFT for outbound payments?

SEPA vs SWIFT differs primarily in geography, speed, and cost. SEPA covers euro payments across 36 countries and settles in under 10 seconds for instant transfers. SWIFT reaches nearly every country globally but takes 2–5 business days and carries higher fees.

Why do outbound payments fail, and how can businesses prevent failures?

Most outbound payment failures result from invalid recipient account details or insufficient funds. Validating IBANs and account numbers against real-time banking databases before execution reduces failed payments by up to 20% and eliminates costly repair fees from correspondent banks.