TL;DR:

- Bank integration creates a secure link between business systems and banks for real-time data synchronization. It can be implemented via direct or aggregator models, each with different control, speed, and scalability benefits. Proper consent flow design and ongoing maintenance are crucial to avoid project failures and ensure reliable operations.

Bank integration is defined as the automated, secure connection between a company’s internal financial systems, such as an ERP or accounting platform, and external banking institutions to enable real-time transaction synchronization. The industry term for this practice is “banking integration,” and it covers everything from automatic bank statement imports to payment initiation directly from your accounting software. Tools like Plaid, OAuth 2.0 authorization frameworks, and ERP add-ons from providers like NetSuite have made this connectivity standard practice for finance teams in 2026. Understanding bank integration meaning is the first step toward eliminating manual data entry, reducing reconciliation errors, and building a financial operation that scales.

What is bank integration and how does it work?

Bank integration works by creating a secure, authenticated channel between your business systems and your bank’s data infrastructure. The process starts with authorization. Using OAuth 2.0, a third-party application requests access to bank data without ever handling your login credentials. The bank issues a scoped, time-limited access token instead. That token governs exactly what data the application can read or write, and for how long.

Once authorized, the integration runs encrypted API calls on a scheduled or event-driven basis. Your ERP pulls transaction records, account balances, and payment statuses directly from the bank. The data flows in both directions. Outbound payment instructions travel from your ERP to the bank, while inbound transaction data returns for automatic reconciliation.

Common use cases include:

- Automatic bank statement imports into accounting software like QuickBooks or SAP

- Payment execution triggered directly from an ERP without logging into a bank portal

- Real-time balance monitoring across multiple accounts

- Transaction categorization applied automatically as data enters the system

Integration automates transaction categorization and reconciliation, which directly reduces the hours finance teams spend on manual data handling. That time savings compounds across every month-end close.

Pro Tip: Always verify that your integration uses API key authentication combined with certificate-based identity verification. Token-only setups without certificate validation are more vulnerable to man-in-the-middle attacks.

What are the main types of bank integration?

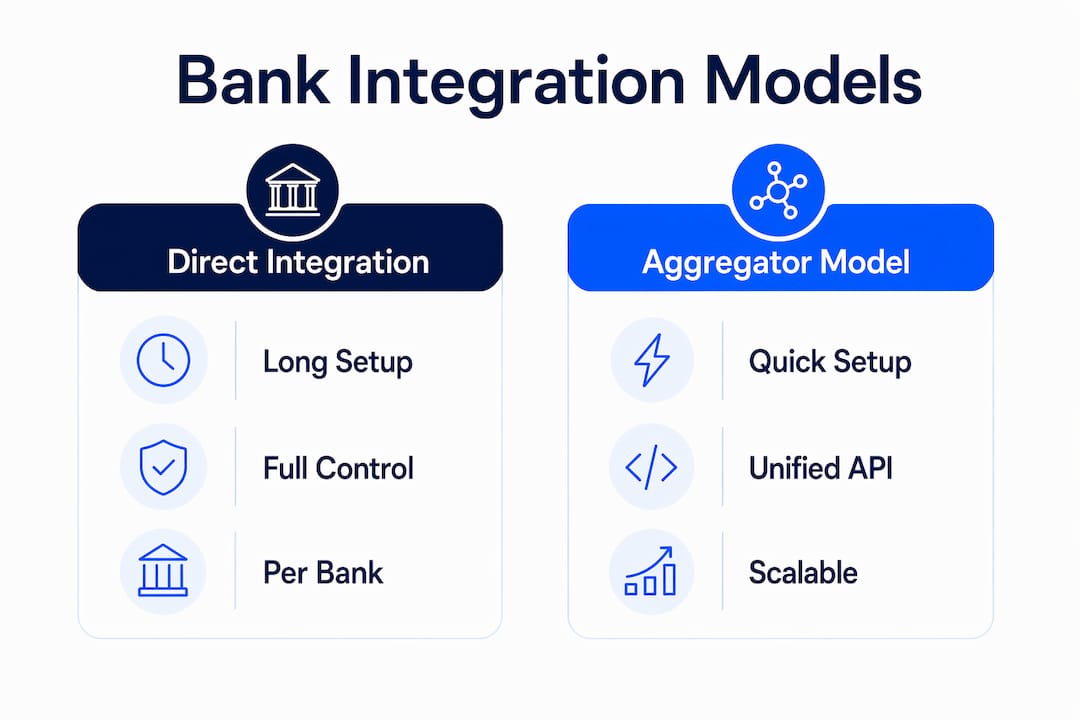

Two primary models define how businesses connect to banks: direct integration and the aggregator model. Each carries different tradeoffs in cost, speed, and control.

Direct bank integration means your business builds a one-to-one connection with each bank using that bank’s proprietary API. Direct integration moves payment approvals from the bank portal into the ERP system, which gives your finance team full control over the approval workflow. The tradeoff is onboarding time. Each direct integration requires separate credentials, certification, and testing, and onboarding typically takes 4–8 weeks per bank. For businesses banking with three or four institutions, that timeline multiplies quickly.

The aggregator model solves the scalability problem. An aggregator like Plaid acts as a single API layer sitting between your systems and thousands of banks. Access over 12,000 financial institutions globally through a normalized data schema, meaning you write integration code once and it works across the entire network. Maintenance overhead drops significantly because the aggregator manages bank-specific API changes on your behalf.

| Criteria | Direct integration | Aggregator model |

|---|---|---|

| Setup time | 4–8 weeks per bank | Days to weeks for full network |

| Cost | Higher per-bank cost | Subscription or per-call pricing |

| Control | Full control over data flow | Dependent on aggregator’s schema |

| Scalability | Low, grows linearly with banks | High, one connection covers thousands |

| Maintenance | Internal team responsibility | Aggregator manages bank-side changes |

One distinction that causes project scoping errors: read-only data feeds are fundamentally different from payment initiation integrations. Treating them as the same leads to underestimating security requirements and compliance obligations.

Pro Tip: Start with an aggregator for data feeds and reporting. Reserve direct integration for payment initiation workflows where you need full control over approval logic and audit trails.

Why is bank integration important for business financial operations?

Bank integration is important because it replaces slow, error-prone manual processes with automated, auditable data flows. The operational benefits are concrete and measurable across four areas.

Efficiency. Automated reconciliation eliminates the manual matching of bank statements against ledger entries. Finance teams that previously spent days on month-end reconciliation can close books in hours. The time saved goes directly into analysis and decision-making.

Visibility. Real-time transaction monitoring means your cash position is always current. You are not waiting for a nightly batch file or a manual export from your bank’s portal. For businesses managing multiple accounts or operating across borders, that visibility is the difference between proactive cash management and reactive firefighting.

Security. Tokenized access through OAuth 2.0 means no one on your team needs to share bank login credentials with a third-party tool. Payment approvals shift inside your ERP, where role-based controls and audit logs already exist. This consolidation reduces the attack surface and makes access reviews straightforward.

Compliance and audit readiness. Every transaction that flows through an integrated system carries a timestamp, a source record, and a reconciliation status. Auditors get a clean, traceable data trail. For businesses operating under EU regulations or cross-border payment rules, that traceability is not optional. Demivolt’s approach to compliance-first onboarding reflects exactly this principle.

What challenges should businesses expect when implementing bank integration?

Bank integration projects fail most often because teams underestimate the technical and organizational complexity involved. Five challenges appear consistently across implementations.

-

Legacy bank system limitations. Many banking cores were built for batch processing and were not designed for real-time API calls. Legacy systems designed in the 1980s require middleware translators to bridge the gap between batch-oriented bank infrastructure and modern cloud ERPs. Without middleware, data arrives in formats your system cannot parse.

-

Middleware architecture. Event-driven architecture and service virtualization prevent the “spaghetti” of undocumented bilateral connections that accumulates when teams build point-to-point integrations without a standard layer. Service virtualization tools simulate legacy core banking behaviors during testing, catching errors before they reach a live environment.

-

User consent flow complexity. Poor consent messaging leads directly to user drop-off during authorization. If users do not clearly understand what data they are authorizing, for what purpose, and for how long, they abandon the process. This is not a technical problem. It is a communication design problem that requires deliberate attention.

-

Onboarding time for direct connections. Direct integrations require separate credentials and testing cycles for each bank. Teams that plan a three-month integration project for five banks often discover the timeline is closer to nine months.

-

Ongoing maintenance. Banks update their APIs, change authentication requirements, and deprecate endpoints. An integration that works today requires active monitoring and periodic updates. Treating integration as a one-time project rather than a continuous operational responsibility is the single most common cause of production failures six months after go-live.

How can businesses get started with bank integration in 2026?

The most effective starting point is a needs assessment focused on three variables: transaction volume, payment channels, and compliance obligations. Those three factors determine which integration model fits your business and how much internal resource you need to commit.

- Assess transaction volume first. Low-volume businesses with one or two banking relationships can often use native integrations built into accounting software like Xero or QuickBooks. High-volume operations with multiple banks need a purpose-built API layer.

- Choose aggregators for initial deployments. Aggregator APIs reduce setup time from weeks to days for read-only data feeds. They are the right starting point for most SMEs.

- Evaluate your ERP’s native capabilities. NetSuite, SAP, and Microsoft Dynamics all offer built-in bank connectivity modules. Using a native module avoids a separate integration project entirely.

- Plan your consent and security workflows before writing code. Define who authorizes data access, what scope they grant, and how tokens are rotated. Document this before implementation begins.

- Use fintech partners for cross-border payment flows. For businesses handling SEPA or SWIFT transactions, a regulated fintech platform provides the compliance infrastructure that a generic aggregator does not. Demivolt’s guidance on secure cross-border payments covers the specific compliance checkpoints that matter for international payment flows.

Pro Tip: Run a pilot integration with one bank account and one data feed before expanding. A controlled pilot surfaces undocumented legacy behaviors and consent flow gaps without disrupting your live financial operations.

Key Takeaways

Bank integration is the foundational layer that connects business financial systems to banking data, and choosing the right model, direct or aggregator, determines how fast and how reliably that connection performs.

| Point | Details |

|---|---|

| Core definition | Bank integration automates the secure connection between ERPs and banks for real-time data sync. |

| Two primary models | Direct integration offers control; aggregator APIs offer speed and scale across thousands of banks. |

| Security framework | OAuth 2.0 grants scoped, time-limited access without exposing bank login credentials. |

| Biggest implementation risk | Legacy bank systems and poor consent flows cause most integration project failures. |

| Starting point | Begin with an aggregator for data feeds, then add direct integration for payment initiation. |

The part most integration guides skip entirely

Finance teams spend months debating direct versus aggregator models and almost no time on consent flow design. That is backwards. I have watched well-funded integration projects stall not because the API was wrong, but because the authorization screen confused users into abandoning the process. The technical architecture was sound. The communication design was not.

The second pattern I see repeatedly: businesses treat bank integration as a project with a finish line. They go live, declare success, and move on. Six months later, a bank updates its API and the integration breaks silently. No one notices until reconciliation fails at month-end. Integration is an operational function, not a deployment event. It needs an owner, a monitoring process, and a maintenance budget.

The businesses that get the most value from bank integration are the ones that start narrow and expand deliberately. One bank, one data feed, one use case. Prove the value, fix the gaps, then scale. That approach sounds slow. It is actually faster than a broad rollout that collapses under its own complexity.

The modern banking infrastructure that supports these integrations has matured significantly, but the organizational discipline required to maintain them has not kept pace. That gap is where most projects fail.

— dd

Demivolt’s tools for accurate bank integration work

Accurate banking data is the foundation of any integration project. A single malformed IBAN can cause a payment to fail, a reconciliation to break, or a compliance check to flag an account.

Demivolt offers a free IBAN Validator built to ISO 13616 standards, which lets finance teams verify account numbers before they enter any integration pipeline. For businesses running SEPA payment flows, Demivolt’s free SEPA tools cover the compliance and formatting checks that cross-border payments require. Both tools are built for the practical realities of business banking, not consumer use cases. If you are building or auditing a bank integration, clean data at the input stage prevents the majority of downstream errors.

FAQ

What is bank integration in simple terms?

Bank integration is the automated connection between a business’s accounting or ERP system and its bank accounts, enabling real-time transaction data to flow without manual exports or data entry.

What are banking APIs and how do they relate to bank integration?

Banking APIs are the technical interfaces that banks expose so external systems can request account data or initiate payments. Bank integration uses these APIs, secured by protocols like OAuth 2.0, to build the connection between business software and financial institutions.

What is the difference between direct integration and an aggregator?

Direct integration connects your system to one bank at a time, with full control but high setup time per bank. An aggregator like Plaid connects once to access thousands of banks through a single normalized API.

How long does bank integration take to implement?

Direct bank integrations typically take 4–8 weeks per bank due to certification and credential requirements. Aggregator-based integrations for read-only data feeds can go live in days to a few weeks.

What is the biggest risk in a bank integration project?

The two most common failure points are legacy bank systems that require middleware to function with modern ERPs, and poorly designed user consent flows that cause drop-off during the authorization process.